Big Model Marketing War: Can "Spending Money" Alleviate Commercialization Anxiety?

09/03 2024

09/03 2024

630

630

AI applications are used for face-to-face marketing, and advertising platforms are raking in profits.

In the era of big model commercialization, it's not just NVIDIA that is taking off, but also internet advertising.

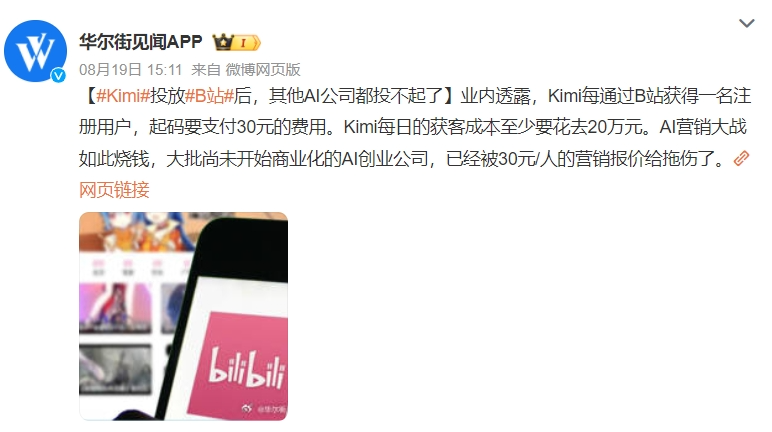

Recent media reports claim that after about five months of advertising investment, Kimi's quoted CPA (Cost Per Action, cost per user conversion) on Bilibili reached as high as around 30 yuan, a "dimensionality reduction blow" to most startups.

Image source: Weibo screenshot

According to data from AppGrowing, a mobile advertising intelligence analysis platform, from April to May this year, ByteDance's AI application "Doubao" invested approximately 15-17.5 million yuan in advertising; by early June, the amount invested in a new round of large-scale advertising surged directly to 124 million yuan.

Can large-scale marketing advertisements bring corresponding commercial returns to AI companies? Besides advertising investments, where is the way out for domestic big model companies?

01. Spend money on advertising, are AI manufacturers "losing money to make a profit"?

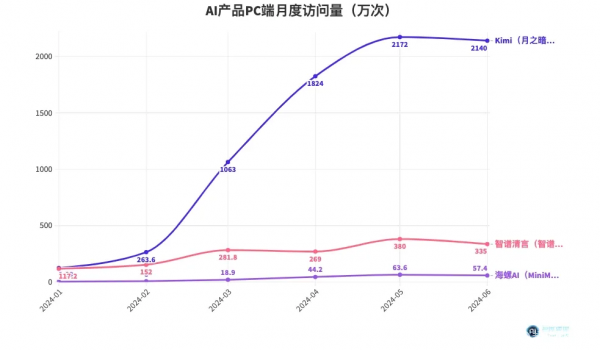

Monitoring data from Similarweb, a website analysis platform, shows that after strengthening its promotion on Bilibili in March this year, Kimi's traffic volume increased by up to 402.9%, pulling far ahead of competitors like Zhipu Qingyan and Hailuo AI.

Image source: AI Emergence

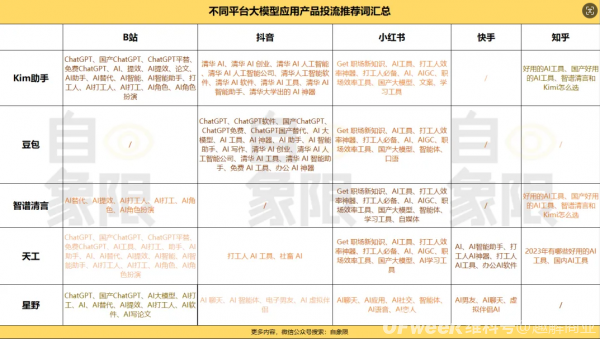

On Bilibili, Kimi is associated with almost every search term a user might use when searching for "AI," such as ChatGPT series, AI series, efficiency-boosting series, assistant series, and worker series, among others; while Tiangong's advertising strategy on Bilibili focuses on capturing search terms like "domestic ChatGPT" to dilute its competitors' branding.

Not just on Bilibili, big model manufacturers are associated with almost every search term related to technology and scenarios on search engines and social platforms, especially those related to work efficiency across various industries, making the competition even more intense.

Image source: Self-quadrant

Besides online advertising, eye-catching big model advertisements are also frequently appearing in offline advertising spaces such as subways and airports. Many urban workers in first-tier cities exclaim: AI applications have become a new form of consumption?

Image source: Canstockphoto

The competition among big models has turned into a "money-burning" marketing war. Fu Sheng, Chairman and CEO of Cheetah Mobile, lamented, "Recently, some big model apps have incredibly high promotion costs, and the ROI just doesn't add up."

A crucial reason why AI applications urgently need marketing promotion is that reasoning costs have been significantly reduced this year, which is a positive signal for the industry to initiate commercial exploration.

Cost reduction refers to the decrease in the price of tokens consumed when big models open APIs for developers and users to input commands, encompassing both reasoning input pricing and reasoning output pricing.

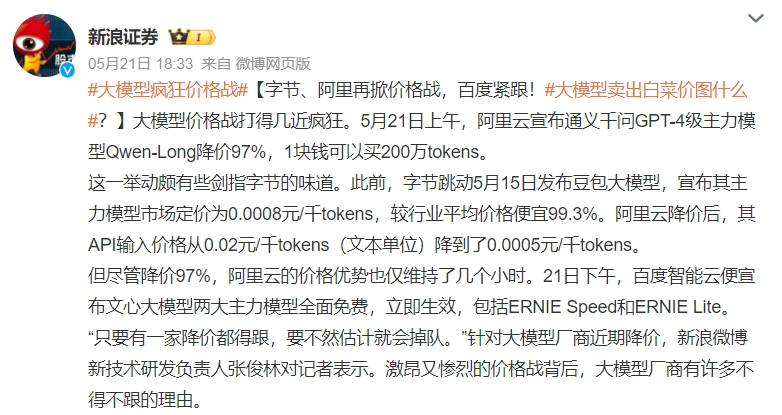

Before commercialization on both the C-end and B-end, the tokens consumed by developers accessing APIs were essentially the "only" source of income for big models. Mainstream big models adjusting prices or even offering services for free is more likely driven by market competition considerations.

Image source: Weibo screenshot

Last year, big model companies were still choosing between ToB and ToC for their commercialization direction. This year, with the "application wave" taking hold, practitioners from different big model companies have all expressed that they are "researching how to achieve user fission."

Entering 2024, the application landing and commercialization path of big models have become the focus. Robin Li, founder of Baidu, bluntly stated at this year's WAIC forum that "without applications, having just a basic model, whether open-source or closed-source, is worthless." Wang Xiaochuan, founder of Baichuan Intelligence, hit the nail on the head with one sentence, "The ToB market is limited."

Gaining users means winning the world, turning into a practical "bidding war"; in this wave of big model application advertising wars, those who directly benefit are the leading big model companies with large user bases or highly targeted traffic advertising platforms.

Image source: Canstockphoto

Additionally, it can be seen from ChatGPT's revenue structure that even without a "killer app," subscription fees for general-purpose big models remain the mainstay. As OpenAI's largest source of revenue, ChatGPT Plus contributes 55% of total revenue, or approximately $1.9 billion, primarily from subscription fees from its 7.7 million global users, each paying $20 per month.

This is even more pronounced in the domestic market, where the Matthew Effect brought about by user scale is becoming increasingly evident. This has also intensified the pressure on big model applications like Zhipu Qingyan, iFLYTEK Spark, and Tongyi, as well as advertising heavyweights like Doubao and Kimi.

The essence of marketing is, of course, to acquire and convert customers. Big models' widespread "money-burning" on advertising is not solely to "lose money to make a profit" by acquiring users but rather a path to accelerate commercialization amidst investor and market pressures.

In the previous stage, short-term hit products like "Miaoya Camera" effectively raised user awareness and tentatively explored commercialization with a price of 9.9 yuan. However, considering long-term commercialization, single-point hit products with heavy entertainment attributes will no longer be pursued by big model companies.

Gaining user recognition of a big model itself is the guarantee for these companies' future ROI. Heavy advertising investment and price competition have thus become the successive promotional strategies employed by big model companies.

Advertising investment seeks to reach the ceiling, while price competition aims to seize market share.

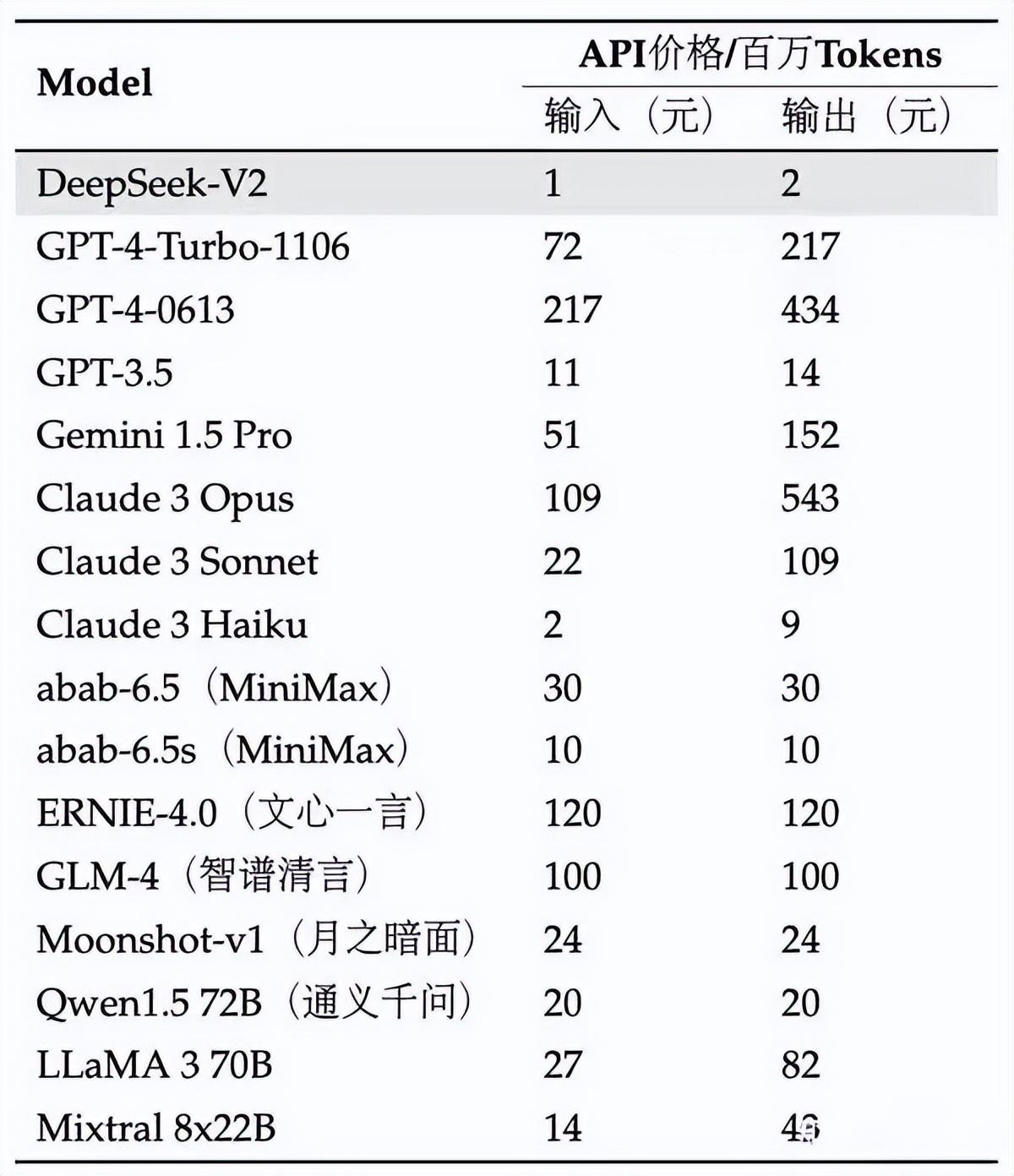

For example, DeepSeek, known as the "price slasher," gained fame overnight in the already established big model landscape by shockingly reducing the input price of one million tokens to just one yuan in May this year.

Image source: The Wall Street Journal

Some big model companies or teams may not excel at creating "super apps," but seizing market share incentivizes developers to rapidly co-create applications; hence, domestic AI big model companies have joined the race to significantly reduce prices.

Image source: Zhidongxi

While emphasizing that "price does not determine the quality of a big model," Baidu honestly made its two flagship big models, ERNIE Speed and ERNIE Lite, free of charge. Similarly, Alibaba's Tongyi simultaneously reduced prices and offered limited free access to both its commercial and open-source models.

Although model reasoning costs have been declining, such "aggressive" price wars among mainstream vendors underscore their determination to compete and "force" smaller big models out of the game.

Regarding this trend, industry opinions vary.

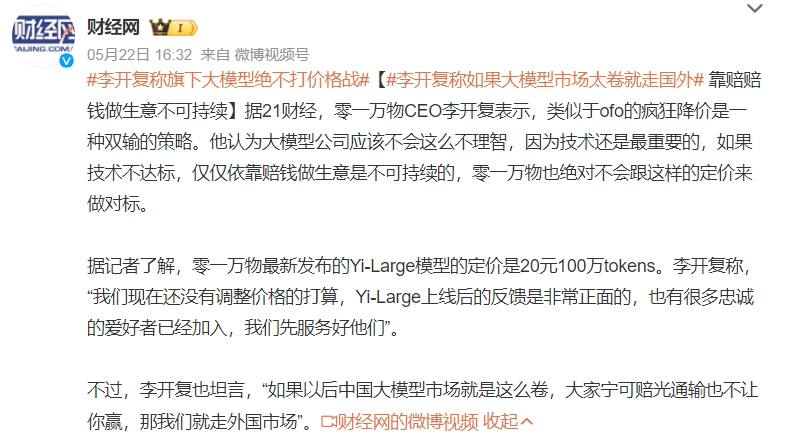

Li Kaifu, CEO of InnoArch, explicitly believes that crazy price cuts akin to those of ofo represent a lose-lose strategy. Wang Xiaochuan, CEO of Baichuan Intelligence, has also stated that big models burning money to acquire customers not only strains corporate cash flows but also risks losing independent development capabilities due to over-reliance on external investments.

Image source: Weibo screenshot

Eric Schmidt, former CEO of Google, recently stated in a speech that the gap between models is widening and that the significant bubble in the market will correct itself.

Luan Jian, head of Xiaomi's big model team, believes that user stickiness is equally important, which could represent an overtaking opportunity for Xiaomi's self-developed products like its big model.

In other words, reducing reasoning costs is about seizing resources from a limited pool of developers and development ecosystems; online and offline advertising investments aim to fish out suitable users from the pan-C-end traffic pool for various application scenarios, essentially paving the way for traffic inlets. However, beyond user acquisition, many big model companies have yet to consider how to enhance user stickiness.

From the perspective of ecological players like Xiaomi, Lenovo, and Microsoft, smart devices and operating systems are already natural traffic inlets, and these capabilities and ecosystems are shortcomings for emerging big model players.

Since the start of summer vacation this year, domestic AI applications, including Doubao, Kimi, Tongyi Qianwen, and Tiangong, have intensified their marketing efforts by "burning money" to increase exposure and compete for users.

Recently, Bilibili stated during its earnings call that "in the first half of the year, the number of advertisers on Bilibili increased by 50% year-on-year, with more advertisers from emerging industries joining, and AI manufacturer coverage exceeding 90%."

It remains uncertain how much commercial return advertising and marketing can bring to AI companies, but it is certain that the beneficiaries of the AI marketing war are traffic platforms; some netizens have even joked, "In the AI era, the most commercially successful is Bilibili."

Image source: Bilibili screenshot

How long will this marketing battle last? Industry insiders expect the money-burning war to potentially continue until the first half of 2025.

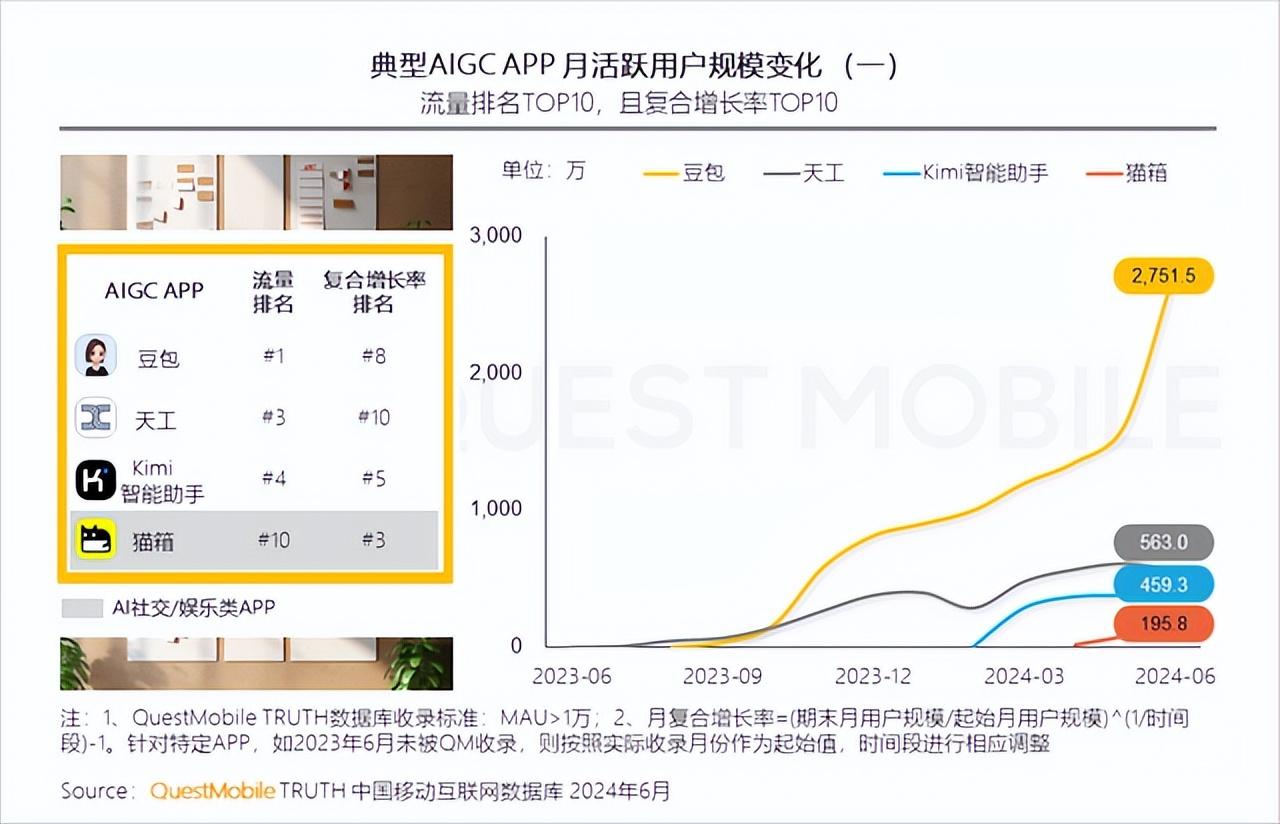

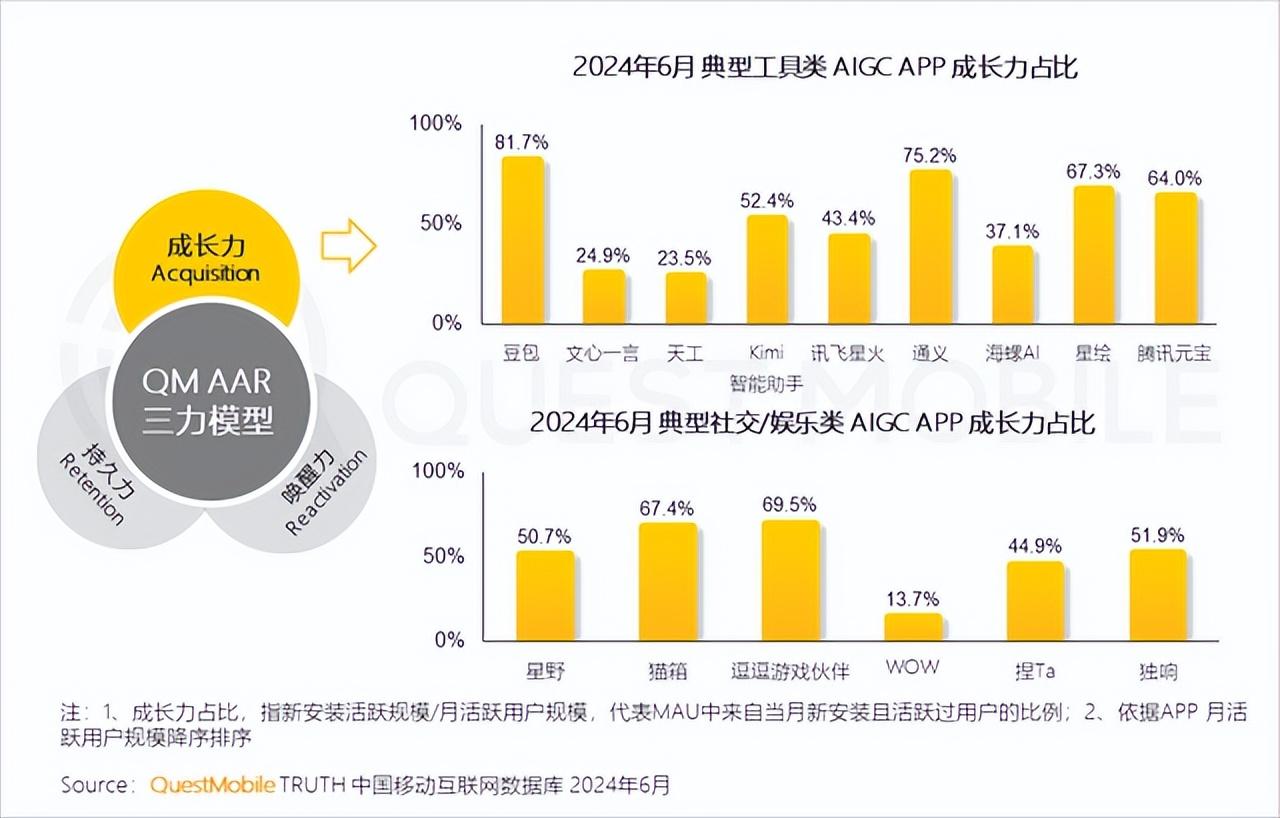

"Spending money" is undoubtedly beneficial to the overall industry's prosperity. In terms of monthly active user data for AI applications in June this year, Maoxiang and Kimi stood out, forming a stark contrast to their relative obscurity six months ago.

Image source: QuestMobile

In terms of traffic composition, Doubao and Kimi, which heavily invested in advertising, both derived over half of their monthly active installations from new user acquisition, demonstrating robust growth momentum.

Image source: QuestMobile

An advertising platform employee who has worked with several big model companies stated that everyone believes in the anchoring effect, and the fear now is that investing heavily in advertising later will be more expensive, with higher user migration costs. Doubao's need to compete in big model advertising with other companies may stem from ByteDance's later start compared to other major players. According to June data from AppGrowing, Doubao invested in 26,521 advertising materials in just one week, while Kimi, ranked second, invested roughly half that amount but still saw a 160% month-on-month increase.

With ByteDance's support, Doubao has delivered impressive results. As of August 30, a search on Xiaomi's App Store revealed that Doubao, iFLYTEK Spark, Wenxin Yiyan, and Kimi had been downloaded 100 million, 73.1 million, 54.27 million, and 28.21 million times, respectively, with Kimi lagging significantly behind the others in downloads.

Image source: Xiaomi App Store screenshot

This raises concerns: now that big model commercialization has become a "resource game," can Dark Moon, Zhipu, MiniMax, and other big model manufacturers outspend the big players in advertising investments? How long can big model companies without commercial profits sustain their high advertising costs?

A former SaaS product founder who has transitioned to GPT applications believes that the CPA war won't last long, perhaps another year at most; "Firstly, the pricing strategy blind box hasn't been opened yet, and no domestic general-purpose big model has truly found its long suit in scenarios. The traffic pool is limited, and everyone is advertising on the same platforms and bloggers, so what's the difference?"

In contrast to the high customer acquisition costs, Kimi and Doubao have both recently chosen the small and simple scenario of "browser plugins" to penetrate the C-end market.

Image source: WeChat official account screenshot

In Tencent's big model industry research report released this year, the compatibility of big model applications with the "smiling curve" is mentioned: the closer to high value-added scenarios like R&D design and marketing services, the faster application landing will be, leading to the conclusion that "big models should avoid the misconception of unilaterally pursuing short-term gains."

A more reasonable approach is to treat big models as R&D or incubation projects, not insisting on absolute short-term financial indicators but instead focusing on relative business improvements and adopting a broad portfolio investment strategy.

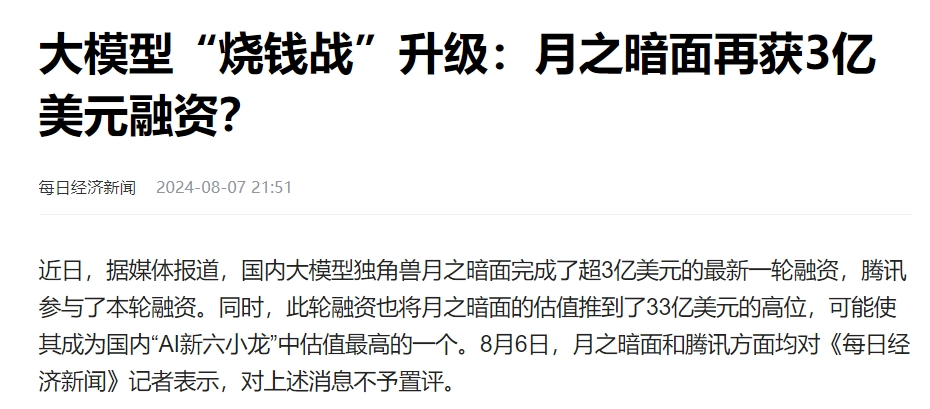

Kimi's commercialization is still in its infancy, and the money burned on marketing can only come from financing. Recently, media reports claimed that Dark Moon completed over $300 million in its latest funding round, with Tencent participating, pushing its latest valuation up to $3.3 billion.

Image source: Baidu screenshot

Investors have high expectations for their "real money" investments, and while large models are still in a high-investment development stage, investors will eventually demand the returns they seek.

In the future, the "Hundred Model War" will inevitably shrink to "Ten Models," and the battlefield will shift from computing power to the market, in line with the value laws of technological change. By this time next year, there may be a "result" regarding the outcome of the bidding game.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?