"UFIDA in the North, Kingdee in the South", is there not much time left for the latter?

09/03 2024

09/03 2024

561

561

The domestic SaaS industry is undergoing a transformation, and fluctuations in the industry have also triggered some abnormal phenomena.

For example, there have been recent voices suggesting that "Kingdee may surpass UFIDA in the next ten years." As we all know, in the domestic SaaS software field, "UFIDA dominates the north, while Kingdee dominates the south," with their headquarters located in two megacities, forming a north-south confrontation.

However, just like "Qiao Feng in the North and Murong in the South," although they stand on opposite sides, their strength is not entirely equal.

The reason behind the suggestion that Kingdee may surpass UFIDA lies primarily in UFIDA's organizational transformation over the past year, coupled with billions of R&D investments that have led to a transitional pain in their business, affecting their 2023 performance and narrowing the gap between UFIDA and the second-tier players in the industry in the first half of this year. Some even directly assert that Kingdee may overtake UFIDA.

Below, let's delve deeper into the intricacies of enterprise services.

1. Revenue difference of nearly double: not in the same tier

Indeed, if Kingdee wants to surpass UFIDA, the first half of this year was the opportunity, almost the only one.

Let's take a look at UFIDA's data for the first half of this year.

According to financial reports, the company achieved a total operating revenue of 3.81 billion yuan in the first half of this year, representing a year-on-year increase of 12.9%, maintaining steady growth. Among this, the cloud service business generated revenue of 2.85 billion yuan, up 21.3% year-on-year, accounting for 74.8% of total operating revenue, with a continuously increasing revenue share.

The suggestion that Kingdee may surpass UFIDA arises because Kingdee's revenue in the first half of this year was 2.87 billion yuan, seemingly very close to UFIDA's. Some voices point out that UFIDA's loss in the first half of the year was 794 million yuan, close to last year's full-year loss, implying a deteriorating performance for UFIDA.

In fact, let's return to the topic at hand and discuss the intricacies within the industry.

Firstly, UFIDA's revenue in 2023 was 9.8 billion yuan, approaching 10 billion, while Kingdee's revenue was 5.68 billion yuan. UFIDA's revenue is almost double that of Kingdee, indicating that these two companies are not in the same tier. If we consider UFIDA as the leader and first-tier player in domestic SaaS, then perhaps UFIDA stands alone in this tier, with Kingdee belonging to the second tier.

Furthermore, to understand why the revenue difference between the two companies in the first half of the year seemed insignificant, let's examine their third and fourth-quarter results.

UFIDA's revenue in the first two quarters of 2023 was 3.37 billion yuan, while the revenue in the third and fourth quarters was 6.43 billion yuan. For UFIDA, the latter half of the year, specifically the third and fourth quarters, accounts for the bulk of its revenue.

In contrast, Kingdee's revenue in the first half of 2023 was 2.57 billion yuan, and 3.11 billion yuan in the third and fourth quarters, resulting in a relatively even distribution throughout the year.

Thus, it becomes clear why the revenue difference between the two companies in the first half of 2024 appears insignificant, as the main event is yet to come.

By now, it should be evident why UFIDA's loss in the first half of the year approached last year's full-year loss. In fact, UFIDA's net profit attributable to shareholders of listed companies in the first half of this year was a loss of 790 million yuan, compared to a loss of 940 million yuan in the same period last year, representing a narrowing of the loss by 150 million yuan.

The narrowing of the loss is a positive trend. Meanwhile, insiders have also noticed some "clues." UFIDA's revenue from central state-owned enterprises accounts for a high proportion, with revenue from large enterprise customers reaching 2.39 billion yuan in the first half of the year, accounting for over 60% of total revenue. This suggests more revenue collections in the latter half of the year, leading to a healthier overall revenue situation.

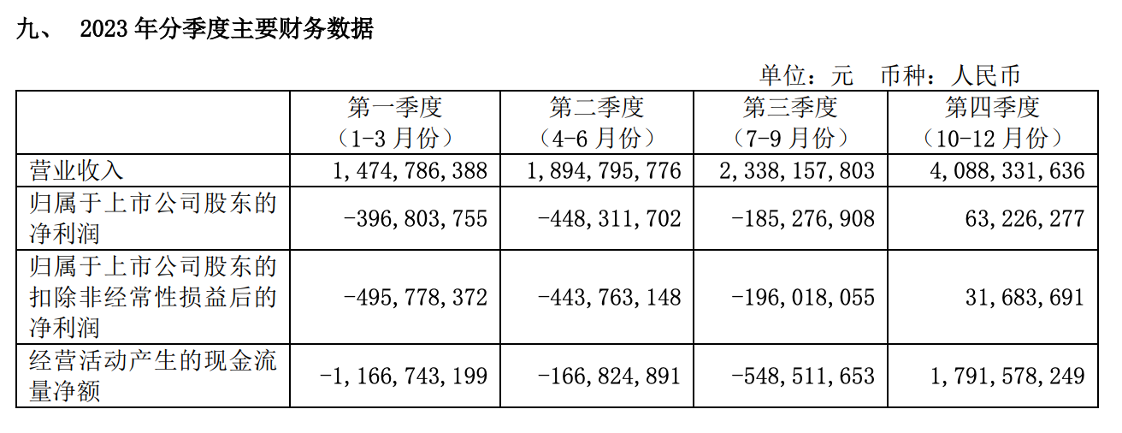

Taking 2023 as an example, the revenue in the first and second quarters was 1.47 billion yuan and 1.89 billion yuan, respectively, while the revenue in the third and fourth quarters was 2.34 billion yuan and 4.09 billion yuan, respectively. For UFIDA, the third and fourth quarters account for the bulk of revenue collections.

In addition, the revenue structures of UFIDA and Kingdee differ. UFIDA's cloud services account for 75% of its overall revenue, while software accounts for 25%. Based on these figures, UFIDA's cloud service revenue exceeds Kingdee's total revenue in the first half of the year.

2. Fierce competition for large customers, but the outcome is clear

If we consider the most direct impact on domestic SaaS over the past two years, it is undoubtedly the substitution of domestic products for foreign ones. In this context, the high ground that SaaS enterprises must strive for is large customers and enterprises.

The number and quality of services provided to large customers sometimes speak volumes in the enterprise service sector.

When examining the differences between UFIDA and Kingdee, we find that there is still a significant gap in magnitude.

Firstly, there are differences in the revenue proportions from small, medium, and large enterprises.

UFIDA's revenue from large customers and the government accounts for 72% of its total revenue, while Kingdee's share is only 28%. Conversely, UFIDA's share from small, medium, and micro-enterprises is 28%, while Kingdee's is 69%.

In the first half of this year, Kingdee Xinghan did achieve certain results in attracting large customers. Financial reports show that the combined cloud service revenue from Kingdee Cloud Sky and Kingdee Cloud Xinghan was 546 million yuan, up 38.9% year-on-year. However, in reality, we understand that enterprises or products tend to gain an advantage in growth rate during their early stages, but their actual size, at less than 600 million yuan, is still very small.

In the past six months, UFIDA has made new breakthroughs in serving ultra-large enterprises, signing contracts with new large central enterprises and industry leaders, including CITIC Group, China Huadian, China Mobile, Dongfeng Motor Group, ZTO Express, Aimer, Chengde Lulu, and Aiyan Group, among others, totaling 40 contracts. Data shows that UFIDA is the domestic vendor that has upgraded and replaced the most international ERP systems.

Clearly, from the perspective of large customers, UFIDA maintains a leading position.

In fact, data also indicates that the industry positions of the two companies are inherently different.

UFIDA's financial reports mention that, according to IDC data, UFIDA continues to lead the Chinese enterprise cloud service market, ranking first in China's aPaaS market share, first in China's enterprise application SaaS market share, and consistently ranking first in China's super-large and large enterprise application SaaS market share for many years.

Kingdee's financial reports, on the other hand, highlight its advantages in the growth enterprise application software market and small and medium-sized markets.

Large customers represent the commanding heights of competition in the enterprise service market, and the different strategies adopted by the two companies reflect their varying degrees of determination to conquer this commanding height.

3. Barriers established through billions of R&D investments

In its interim report, several key indicators of UFIDA are worthy of attention.

Firstly, UFIDA's gross margin was 52.5% in the first half of the year and 54.0% in the second quarter alone, marking a continuous increase in gross margins. This indicates that UFIDA's basic products have been refined and have entered the stage of later returns.

In simple terms, enterprise service products exhibit certain marginal effects. Heavy investments in the early stages can lead to better products tailored to customer needs. Only after the products are refined will the marginal benefits of product revenue become apparent.

In terms of renewal rates, YonBIP revenue grew by 42.1% year-on-year during the reporting period, with a renewal rate of 101.1%; YonSuite revenue grew by 116.1% year-on-year, with a continuously improving renewal rate of 92.4%.

The most direct manifestation is that UFIDA's product reputation has been transmitted to the industrial end, resulting in an increase of 81,800 new cloud service paying customers in the first half of this year, compared to 59,500 last year. The surge in new customers indicates that UFIDA's industrialization strategy has won market recognition. Additionally, UFIDA signed a new batch of benchmark enterprises such as central state-owned enterprises in the first half of this year, laying a solid foundation for future replication and promotion.

Since its inception, UFIDA has accumulated a 36-year brand reputation, with capabilities in technology and products that enable it to serve ultra-large customers. It better meets the requirements of large enterprises in terms of information security and service guarantees, which are almost unique capabilities and barriers in the industry.

According to rough estimates, UFIDA has invested over 10 billion yuan in the past few years, with R&D investment accounting for 32.8% of revenue in 2023. In August this year, UFIDA BIP and YonGPT, the enterprise service large model, were upgraded again, reaching a leading level among similar vendors.

UFIDA has built a product system that can "accompany enterprises as they grow," meaning that as an enterprise evolves from a growth-stage enterprise to a large or giant enterprise, UFIDA ensures that enterprise applications, experiences, and data remain unchanged, enabling "seamless" switching of enterprise applications and ensuring business continuity and stability. This is a capability that Kingdee's product system lacks.

Most importantly, the ability to serve large customers does not happen overnight. We can observe that UFIDA's confidence stems from accompanying customers in their growth over 36 years, during which time it has accumulated a wealth of industry know-how and leading practices. This is why UFIDA can continuously gain customer trust and create a series of benchmark users.

Currently, UFIDA has established group-level enterprise software cooperation with 74 central enterprises. At the same time, it has created a large number of benchmark industry customers represented by long industrial chains, laying a solid foundation for gaining more market recognition and trust.

Of course, in the era of digital intelligence, for UFIDA to win more market recognition, it must continue to iterate and refine its products.

Summary

With the advent of a new SaaS cycle, the landscape of the SaaS industry over the next decade is taking shape. Enterprises that understand their customers, invest heavily in R&D, refine their products, and delve deeply into their industries will be the most direct beneficiaries of this trend.

Polarization will become even more pronounced, and there is not much time left for latecomers in the market.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?