Venturing into Satellite Manufacturing: Another BIT Graduate is Eyeing an IPO

05/22 2026

05/22 2026

455

455

The global commercial space industry stands on the brink of a breakthrough.

In the first quarter of this year, SpaceX Starlink surpassed 10,000 satellites in orbit, accounting for nearly 70% of all active satellites in Earth's orbit. The company plans to launch the world's largest IPO with a valuation of $1.75 trillion.

Domestically, since June 2025, when the scope of the Science and Technology Innovation Growth Layer was expanded to include cutting-edge fields such as commercial space, the pathway for companies in the commercial space sector to go public has gradually opened up.

The capital markets have responded accordingly. In the first quarter of 2026, the total disclosed financing in China's commercial space sector reached 8.02 billion yuan, a staggering 4.6-fold increase year-on-year. Major players in the commercial space sector, including LandSpace, Galaxy Space, Galactic Energy, and Chang Guang Satellite, have successively initiated or restarted their IPO processes.

The latest development is that on May 11, Weina Xingkong, a unicorn in the commercial space sector, officially had its IPO application accepted by the Science and Technology Innovation Board. As satellite manufacturing becomes a business, a pressing question arises: amidst the hype, when will profitability be achieved?

I. Satellites Enter the Era of Mass Production

Space is undergoing a transformation: from an exclusive national mission to an integral part of everyday life.

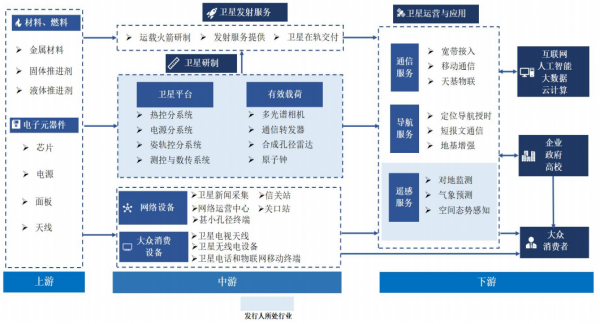

From a industrial chain (industrial chain) perspective, the industry can be roughly divided into three layers. The upstream layer involves satellite and rocket manufacturing, the midstream layer focuses on launch services, and the downstream layer encompasses satellite operations and applications. The relationships between these layers are clear: without upstream production, there would be nothing for the downstream to launch; if rockets cannot keep up, satellites will remain grounded, awaiting their turn.

Within this chain, the generally recognized market space ratio for rockets, satellite manufacturing, and satellite operations is 1:5:20.

Currently, several key application scenarios are pushing the boundaries of the satellite market.

Communication satellites act as signal base stations in space, delivering broadband signals to areas beyond the reach of ground-based stations. In the second half of 2025, the low-orbit satellite internet system commenced public testing, with China Unicom introducing a 10 yuan monthly satellite package, piloted in eight provinces and cities, and supported by mainstream smartphone models from Huawei, Xiaomi, and others. Satellite communication is transitioning from a lifesaving button in extreme environments to a standard feature on smartphones and intelligent vehicles.

Remote sensing satellites function as cameras in space, capturing high-definition images of Earth. They find applications in agricultural insurance for disaster assessment, carbon emission monitoring for urban management, and more. By 2025, China's satellite remote sensing industry had reached a scale of 245 billion yuan, with the commercial remote sensing data services market surpassing 20 billion yuan.

Navigation augmentation satellites enhance positioning accuracy, which is crucial for scenarios like autonomous driving and unmanned aerial vehicle logistics.

While demand is expanding, supply-side support is also emerging.

In the past, the high cost of rocket launches was the biggest bottleneck for satellite constellation networking. In December 2025, LandSpace's Zhuque-3 became the first domestically developed reusable rocket to successfully reach orbit. Once reusable technology is perfected, the significant reduction in single-launch costs will bring satellite commercialization one step closer.

Weina Xingkong has entered the satellite manufacturing sector, which serves as a crucial link in the industrial chain, connecting the upstream and downstream.

In August 2017, Gao Enyu resigned from the China Academy of Space Technology and, along with two partners who also left the system, started his own venture.

Gao Enyu, a doctoral graduate in aerospace jointly trained by Beijing Institute of Technology and Pennsylvania State University, had previously worked at the China Academy of Launch Vehicle Technology and the China Academy of Space Technology. Co-founder Kong Lingbo came from DFH Satellite Co., Ltd., while Huan Yiheng had experience at China Spacesat Co., Ltd. and AVIC Avionics.

In its early days, the company followed a project-based approach, customizing small satellites weighing a few dozen kilograms for research institutes and universities, meticulously crafting each one like an artisan workshop.

Without scale, cost reduction is difficult; without low costs, securing orders becomes challenging, leading to a reliance on customization and piecemeal production. Now, there is a breakthrough to this chicken-and-egg dilemma.

China StarNet's GW constellation plans for approximately 13,000 satellites, while Yuanxin Satellite's Qianfan constellation envisions around 15,000. These Deterministic demand (definitive demands) from downstream mega-constellations are driving upstream supply chain investments and industrial ecosystem construction on a large scale.

With nearly 30,000 satellites in demand from these two super constellations, traditional production methods may not even qualify for bidding.

Thus, satellite manufacturing has entered the era of mass production, akin to automobile manufacturing.

Galaxy Space has established China's first intelligent satellite assembly line in Nantong, capable of producing 150 medium-sized satellites annually, reducing production cycles by 80%. Space Honor's pulsating production line in Zhuzhou also claims an annual capacity of 150 satellites, accommodating multiple varieties.

Weina Xingkong's satellite intelligent manufacturing base in Wuxi has received approval from the National Development and Reform Commission, with an annual capacity of 150 satellites as well. The prospectus also mentions that the company has achieved flexible, mass, and rapid customization of satellites ranging from 10kg to 500kg, adaptable to the production needs of various satellite types, including remote sensing, communication, and navigation.

By the end of 2025, Zhou Xin, the Senior Deputy General Manager of Weina Xingkong, calculated that the company expects to reduce satellite manufacturing costs to one-third to one-half of current levels within the next three years, relying on integration to reduce the number of standalone units, intelligence to enable software-defined capabilities, and mass production to dilute fixed costs.

Cost reduction through mass production is the ticket to entry.

II. Why Raise 5 Billion with Less Than 500 Million in Annual Revenue?

Although satellite manufacturing is transitioning from "artisanal" to "industrial" products, Weina Xingkong currently still exhibits a high degree of customization.

Limited by industry regulatory policies, funding, and terminal application scenarios, downstream customers in the domestic satellite manufacturing industry are primarily satellite constellation operators and research institutes, presenting a relatively concentrated market.

This has led to Weina Xingkong's heavy reliance on major customers.

From 2023 to 2025, revenue from Weina Xingkong's top five customers accounted for 79.75%, 74.95%, and 92.33%, respectively. In 2025, the largest customer contributed 216 million yuan, accounting for 56.15% of the total. Each significant order carries substantial weight; losing a single customer could topple half the business.

The upstream situation is similar. The main services and raw materials procured by Weina Xingkong, including rocket launch services, satellite payload components, satellite platform components, and components (components), are all highly customized.

To ensure reliability, mature suppliers are generally chosen for long-term cooperation, resulting in a crowded supplier list. The top five suppliers accounted for 52.29%, 72.02%, and 67.66% of procurement, respectively. With core suppliers, any delays or price hikes leave little room for maneuver.

Due to the high degree of customization, complex and lengthy development processes, and substantial capital investments, Weina Xingkong typically needs to arrange development in advance. If customers renege on their commitments after adjusting requirements, or if quality issues arise during product development and delivery, the company faces the risk of significant inventory write-downs.

From 2023 to 2025, Weina Xingkong's inventory write-down losses were 8.7486 million yuan, 22.5842 million yuan, and 8.8835 million yuan, respectively. In January 2026, the MN50-8 satellite was destroyed during launch due to rocket failure, and this loss will also be reflected in the annual profit and loss statement.

With few customers and long cycles, the process from securing a satellite order, conducting overall satellite design, implementing satellite manufacturing, to delivery typically takes six months to a year. Consequently, Weina Xingkong's performance is highly volatile.

From 2023 to 2025, the company's operating revenue was 51.084 million yuan, 40.008 million yuan, and 385 million yuan, respectively, totaling less than 500 million yuan over three years.

The profit picture is even less favorable. During the same period, Weina Xingkong's net profit attributable to shareholders was -600 million yuan, -312 million yuan, and -181 million yuan, respectively, with cumulative losses of approximately 1.093 billion yuan over three years.

Cash flow is equally tight, with net cash flow from operating activities being negative for three consecutive years, at -210 million yuan, -376 million yuan, and -189 million yuan, respectively.

The good news is that the comprehensive gross profit margin turned positive in 2025, reaching 11.87%, up from -108.3% in 2023 and -68.6% in 2024, with losses narrowing. However, there is still a way to go before truly crossing the breakeven line.

As for how long this journey will take, it depends on when Weina Xingkong can successfully transition from a project-based model.

This is also a key use of the funds raised in Weina Xingkong's IPO.

Weina Xingkong plans to raise 5 billion yuan in this IPO, with five projects. Apart from the headquarters and R&D center, the largest allocation of 1.2 billion yuan will go towards the first phase of the Taijing Satellite Constellation Construction Project, planning to launch 30 optical/SAR hybrid networking satellites and establish a small-scale constellation.

This can be interpreted as Weina Xingkong's attempt to shift from a "satellite seller" to a "satellite operator," including satellite leasing and data services, while also using "constellations in the sky" to demonstrate the reliability of its entire satellite and system.

The business logic of this transformation is clear.

Smart driving companies, logistics firms, and agricultural insurance companies are unlikely to spend tens of millions yuan upfront to purchase a single satellite. However, they are willing to pay monthly or annual fees for a continuous stream of positioning data or weekly updated remote sensing images. Switching from a project-based to a subscription-based model, once successful, will transform revenue from one-time whole-satellite deliveries into a steady cash flow.

The vertically integrated development model of "aerospace manufacturing + operational services" is also a current global trend in commercial space. For example, SpaceX has formed an industrial model integrating rocket manufacturing, satellite manufacturing, and satellite operations, which is more conducive to product standardization and cost reduction.

However, the cost is also substantial. Building a constellation involves significant upfront investment followed by a wait for returns. Additionally, satellites have a limited lifespan, typically 5-8 years, requiring continuous launches, orbital maintenance, and network replenishment, resulting in ongoing capital consumption and potentially long payback periods.

III. The Support and Open Questions Behind the Billion-Dollar Valuation

Over the past few years, Weina Xingkong has undergone a rapid price surge in the primary market.

In 2022, the Series B/B+ round raised nearly 400 million yuan, with a post-investment valuation of 3 billion yuan after the B+ round. In June 2024, the Series C1 round raised 1 billion yuan, pushing the post-investment valuation to 7 billion yuan. By January 2026, in the Pre-IPO round, the institutional share purchase price had risen to 125-134 yuan per share, implying a valuation close to 10 billion yuan.

For this IPO, Weina Xingkong has also chosen the first set of criteria for differential voting rights arrangements on the Science and Technology Innovation Board, with an expected market capitalization of no less than 10 billion yuan.

The first pillar of support is scarcity.

The rocket sector is crowded, and satellite operators are abundant, but few private enterprises in the middle of the industrial chain focus solely on complete satellite manufacturing. With an annual production capacity of 150 satellites, a flight heritage of 32 satellites, and full-stack capabilities covering remote sensing, communication, and navigation satellites, it is challenging to find a perfect match among domestic private satellite enterprises.

The second pillar of support is the transformation option. As mentioned earlier, once the subscription-based data service model is successful, the company can enjoy the valuation premium of the data services sector.

Guojin Securities' research report suggests that when a company reaches the IPO stage, "hard indicators" such as order reserve amounts, customer structure (whether determinism framework agreements have been signed with national constellation operators), and in-orbit delivery success rates are replacing the "TAM (Total Addressable Market) storytelling" approach.

In other words, at the industrialization stage, the market will use more quantitative operational and financial indicators as anchors for valuation, and grandiose prospects described qualitatively may no longer sway investors.

This is even more evident in international markets.

Planet Labs, a pure satellite remote sensing operator, reported revenue of approximately $310 million in the most recent fiscal year, with a price-to-sales ratio of over 40 times. Accompanying the rise in the price-to-sales ratio was the achievement of fiscal year profitability in adjusted EBITDA, although general-purpose profitability has not yet been realized, along with positive cash flow.

When SpaceX plans to go public with a valuation of $1.75 trillion, its price-to-sales ratio approaches 100 times. Supporting this valuation multiple is the fact that Starlink achieved cash flow breakeven in 2023, profitability and positive free cash flow in 2024, and surpassed 9 million active customers by the end of 2025.

Currently, Weina Xingkong is in a state of continuous losses, with cumulative net profit attributable to shareholders exceeding 1 billion yuan over three years and negative operating cash flow for three consecutive years. When it can generate verifiable, low-cost, highly reliable, and sustainable revenue, and how much premium the market is willing to assign to the transformation option during the fundraising stage, remains uncertain, given the significant differences between domestic and international markets.

Domestic precedents also warrant attention. Chang Guang Satellite submitted its Science and Technology Innovation Board application in December 2022, planning to raise 2.683 billion yuan, primarily for self-building and operating a remote sensing constellation. It later withdrew the application voluntarily but has since restarted its IPO. During the review and inquiry process, the operational sustainability under unprofitable conditions was a direction repeatedly questioned by regulators.

As mentioned earlier, suppliers are highly concentrated. Therefore, the autonomy and replaceability of core component suppliers are also key issues. For example, although the localization rate of aerospace-grade chips has been improving, it remains low overall, with high-end models relying on imports for 90% of their needs. Currently, the relevant information in Weina Xingkong's prospectus is insufficient.

For Weina Xingkong, if the IPO is unsuccessful, it not only faces the risk of falling behind in competition but also requires the founding shareholders to fulfill substantial repurchase obligations.

Weina Xingkong stands at the cusp of a commercial space boom and at a crossroads in its own transformation. Whether it can transition from customization to mass production and scalability will determine not only its ability to cross the breakeven line but also whether its 10 billion yuan valuation can materialize.

-

![]()

Why Is Tencent Not Rushing into the AI Race?

-

![]()

Application of Agentic AI in Cancer Research and Oncology

-

![]()

Several Hidden Signals from the Alibaba Cloud Summit

-

![]()

Big Shake-Ups in PR at Leading Firms! Top Executives in Internet and Auto Sectors See Major Turnover, Talent Migration Reaches New Heights

-

![]()

Unchecked Weight Gain in New Energy Vehicles: Taxation as a Stopgap, Not a Long-Term Fix

-

140 Trillion Tokens Later: China is Building a 'High-Speed Rail for Computing Power'

-

![]()

Jeep's Second Attempt: Stellantis' Self-Rescue More Like a Leveraged Position Increase

-

Chinese Cars' North American Experience: Canada Opens a Window While the U.S. Tightens the Door