Latest Report on Cellular IoT Modules: Revenue Growth Trails Shipment Growth? AI Memory Pressure Impacts IoT Supply Chain

07/06 2026

07/06 2026

346

346

Recently, Berg Insight, an independent market research and consulting firm with a specialized focus on the global IoT sector, unveiled the latest data concerning the full-year market performance of cellular IoT modules in 2025. According to the report, in 2025, the annual shipments of cellular IoT modules, excluding automotive NAD modules, soared to 612 million units, marking a 33% year-on-year increase. Meanwhile, the full-year revenue from these modules climbed by 19%, reaching $5.6 billion.

These figures not only signify a market recovery but also hint at mounting pressure on module prices and component costs. For manufacturers of cellular IoT devices, 2025 was not just a year of renewed growth; it was also a year when the recovery of sales volume and the recovery of value in the module supply chain were no longer in sync.

This article will delve into recent market developments and future prospects by incorporating data from other institutions.

Destocking and Local Policies Jointly Fuel Recovery

Regarding market growth rates, two other research institutions had already released relevant data before Berg Insight.

Counterpoint Research's report, issued in March 2026, indicated a 15% year-on-year increase in global cellular IoT module shipments in 2025, suggesting steady market growth.

TSR's 2025-2026 Cellular IoT Module Market Outlook report, published in February 2026, revealed a 23% year-on-year rise in global shipments, reaching 544 million units, with market revenue hovering around $3.93 billion.

In contrast, Berg Insight's 33% year-on-year growth figure is the most optimistic. The discrepancies in the assessments of the 2025 cellular IoT module market by the three institutions do not necessarily imply correctness or incorrectness; rather, they are likely attributable to differences in statistical scope and market definitions. Berg Insight adopts a broader "shipment perspective," encompassing a wider array of cellular IoT module types, especially Cat-1 bis, NB-IoT, and low-cost terminals widely utilized in the Chinese market. This approach more readily reflects the amplified effect of "channel shipments and inventory replenishment." Counterpoint Research may lean more towards "end-user demand and revenue quality," emphasizing real deployment rhythms and structural growth, potentially excluding some volatile pan-IoT shipments, resulting in a relatively conservative overall assessment. TSR's model falls somewhere in between, with stricter screening of regional and technical classifications, presenting median results in terms of scale and growth rate.

Nevertheless, all three institutions concur on the trend of market rebound. Berg Insight attributes this rebound primarily to the recovery of demand in major global regions, with high customer inventory levels being a significant factor in the previous market downturn. In reality, a substantial portion of the 2025 shipment growth stemmed from the digestion of excess inventory in the channel, not just the expansion of new demand in the end market.

The report also underscores that local policies in some countries, including China and Spain, provided additional growth momentum. This is particularly crucial because demand for cellular IoT modules is often driven not only by enterprises' digitalization needs but also by regulatory policies and public sector projects. Smart metering, payment systems, utilities, public infrastructure, and compliance-driven device upgrade cycles can all generate concentrated demand for specific module categories, even when overall corporate IoT investments remain cautious.

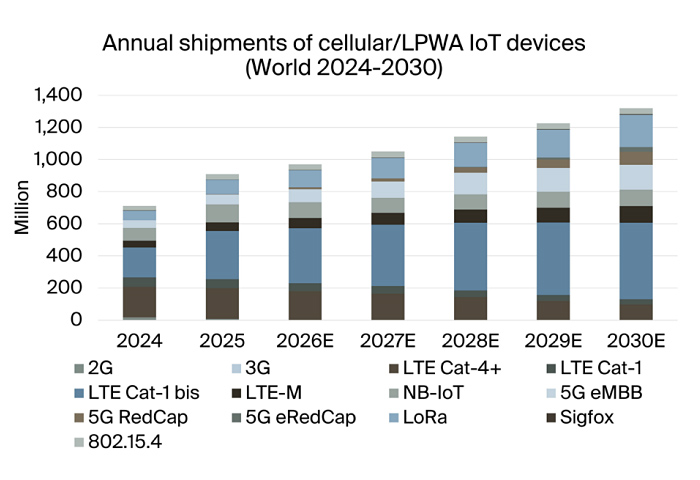

Berg Insight predicts that cellular IoT module shipments will grow at a 7% compound annual growth rate (CAGR) to reach 878 million units by 2030. Compared to the 33% high growth in 2025, this suggests a gradual return to normal market growth rates after inventory adjustments.

The Gap Between Sales Volume Growth and Revenue Growth Warrants Attention

The core contradiction in IoT market growth lies not in acceleration but rather in the gap between shipment growth and revenue growth, which is one of the most noteworthy signals in this report. According to Berg Insight's data, despite the rapid expansion in overall market shipments, the average revenue per module declined year-on-year. For OEM manufacturers and connectivity hardware suppliers, this implies that while demand has indeed recovered, market pricing power remains unevenly distributed.

Berg Insight points out that memory price pressure is emerging as a new structural variable in the cellular IoT market, with its roots not in IoT itself but in the sustained absorption of high-bandwidth memory (HBM) capacity by AI servers and data centers.

This change has created a cross-industry supply chain transmission effect. Although IoT modules and AI servers do not directly compete in end-user applications, they share an upstream semiconductor and memory supply system. Consequently, the IoT industry is passively bearing cost spillovers from AI infrastructure expansion.

Unlike traditional "shortage cycles," this round of impact manifests more as sustained upward price pressure rather than supply shortages. Among them, 5G modules, with their higher memory configurations and stronger reliance on advanced DRAM, are most severely affected. Traditional 4G LTE modules with legacy memory architectures, however, have relatively more buffer space. Nevertheless, Berg Insight also notes that almost no product can fully escape this trend.

A deeper change is that this trend is reshaping the industry's operational logic. The cost structure of cellular IoT modules no longer enjoys high stability, with suppliers increasingly introducing periodic price adjustment mechanisms and contract price linkage clauses to cope with component cost fluctuations. For OEM manufacturers and system integrators, this means the "stable BOM assumption" relied upon for long-term product planning is being shattered. In industrial IoT and utility scenarios characterized by multi-year lifecycles, cost uncertainty will directly impact business model design, project calculations, and investment return cycle assessments, undoubtedly increasing the complexity of long-term product planning.

Overall Market Competition Remains Highly Concentrated

From a competitive standpoint, the cellular module market remains highly concentrated. Berg Insight data shows that in 2025, the top five manufacturers—Quectel, Fibocom, Telit Cinterion, MeiG, and China Mobile—collectively accounted for 73% of market revenue.

However, from a shipment perspective, leading positions are largely determined by the Chinese domestic market. Quectel, China Mobile, Sunsea AIoT, Lierda, and Fibocom are the main shipment leaders, benefiting from strong local demand in China. Meanwhile, ZXInfoTek has rapidly risen, particularly establishing a clear advantage in POS terminal applications. Demand for connectivity modules in this niche market is closely tied to payment device upgrade and deployment cycles.

The chip market landscape reinforces the same regional trend. Berg Insight estimates that cellular IoT chipset shipments (excluding automotive-grade products) reached 706 million units in 2025, with ASR, Qualcomm, Esimcom, Unisoc, Xinyi, and MediaTek as the main suppliers. Among them, Chinese domestic chip manufacturers performed particularly strongly, with ASR, Esimcom, and Xinyi achieving robust growth in LTE Cat-1 bis and NB-IoT chipsets. Qualcomm maintained a strong position in LTE-M, high-end 4G LTE, and 5G eMBB chipsets.

In the report, due to differing supply chain systems, data for automotive-grade modules (NAD modules) is presented separately. Quectel ranks first with a 27% shipment market share, followed by Rolling Wireless at 13%. Other major NAD module manufacturers include TCU suppliers LG Electronics and Aumovio, as well as Kontron, Guangtongyuanchi (Fibocom), MeiG, and Compal. The automotive-grade chipset market is dominated by Qualcomm, with MediaTek ranking second.

The report forecasts that NAD module shipments will grow from 78 million units in 2025 to 98 million units in 2030, representing a 4.6% CAGR during the period.

The IoT Market is Highly Diversified

IoT continues to evolve and expand into new application areas, with the overall market being highly diversified and forming multiple technology ecosystems. Berg Insight's report focuses not only on the 3GPP-based cellular communication technology ecosystem and LPWA (low-power wide-area network) technologies like LoRa and Sigfox but also covers other low-power IoT technologies, such as IEEE 802.15.4-based protocols, Wirepas Mesh, DECT-2020 NR (NR+), and Mioty.

LoRa is gradually becoming an important platform for global IoT device connectivity. By early 2026, cumulative LoRa terminal node shipments had reached 500 million units. Currently, most demand comes from private network deployments, which remain the dominant deployment model for LoRa networks, with primary applications in smart gas and water metering, followed by localized IoT deployments for smart sensors and tracking devices in cities, industrial parks, and commercial buildings. In the coming years, smart homes are expected to become one of LoRa's key application areas, driven primarily by Amazon Sidewalk's expansion beyond the United States. Berg Insight estimates that annual LoRa device shipments reached 90 million units in 2025 and are expected to grow at a 17.5% CAGR to 202 million units by 2030.

Other low-power IoT device ecosystems, such as IEEE 802.15.4, Wirepas Mesh, Sigfox, Mioty, and NR+, also have the potential to grow into important IoT connectivity platforms in the coming years. Among them, IEEE 802.15.4 currently has the broadest application deployment, being the most mature technology in this group and supported by several leading smart metering manufacturers.

By early 2026, Wirepas Mesh had exceeded 20 million installations and had been deployed in multiple large-scale projects. Sigfox reached 15 million installations by the end of 2025. Singapore-based Sigfox operator UnaBiz took over Sigfox in 2022, restructuring its technological roadmap and commercial operating model. Berg Insight believes that Sigfox's future recognition in the asset tracking market will be a key test for its development.

Mioty has gained increasing attention in smart water metering in recent years, with installations now exceeding 1 million units. Meanwhile, DECT-2020 NR (NR+) is still in an earlier development stage, with current deployments mainly concentrated in pilot projects and initial commercial applications.

References:

The Cellular IoT and LPWA Chipset and Module Market——berginsight

2025 IoT Module Industry Report Released: Lierda's Shipments Grow 69% Year-on-Year, Ranking Fourth Globally——Lierda

Cellular IoT Module Market Returns to Double-Digit Growth as Revenues Reach $5.6 Billion——iot business

Cellular IoT reached new heights in 2025——Computer Weekly

Top 5 Chinese Cellular IoT Module Manufacturers Account for Nearly 70% of Global Shipments, Facing a Series of New Challenges——IoT Intelligence

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models