Tencent Divests Kuaishou Stake: A Familiar Tale

07/07 2026

07/07 2026

427

427

Tencent's Divestment of Kuaishou Shares Sparks Immediate Market Response

Following the market's close on July 6, Tencent Mobility, a subsidiary of Tencent, offloaded 272.9 million Class B shares of Kuaishou via off-exchange block trades at HK$43.25 per share. This price represented a roughly 6% discount to the day's closing price, raising approximately US$1.505 billion. Post-transaction, Tencent's ownership in Kuaishou decreased from 15.68% to 9.37%, relinquishing its major shareholder status.

Kuaishou's stock price plummeted by over 9% at today's market opening. The pressure stemmed from two fronts: Firstly, the potential supply pressure from Tencent's remaining 9.37% stake. Secondly, the strategic devaluation following the shift in the Tencent-Kuaishou relationship from equity-based collaboration to market-driven cooperation.

Kuaishou's share buybacks could mitigate the short-term impact. Under its HK$16 billion share repurchase initiative, the company has already bought back shares totaling HK$8.35 billion, equivalent to about 70% of the funds raised from Tencent's current sale. However, buybacks do not equate to a revaluation of the company; they merely offer short-term support. Looking ahead, Kuaishou will need to rely on profits from its core business and Kling's performance to restore market confidence.

01. Strategic Mirage: The "Mature Kuaishou" Loses Its Luster

Tencent began heavily investing in Kuaishou in 2017 as a defensive strategy to safeguard its traffic.

At that time, WeChat Channels were still in their infancy, and Douyin was rapidly gaining user attention. Kuaishou emerged as Tencent's most crucial external ally in the short-video arena. The value of equity binding extended beyond financial returns to strategic equilibrium.

However, this value has significantly diminished today.

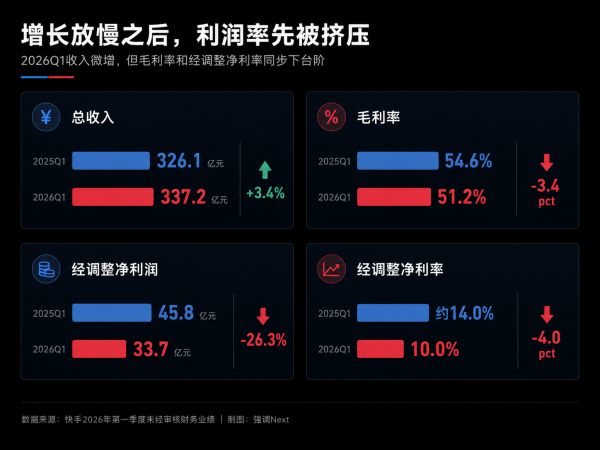

In the first quarter of this year, Kuaishou reported revenue of RMB 33.7 billion, up 3.4% year-on-year. Its daily active users reached 412.7 million, and monthly active users stood at 771.7 million, indicating a stable user base. Nevertheless, live-streaming revenue declined by 13.5% year-on-year, gross margin fell from 54.6% to 51.2%, adjusted net profit was RMB 3.4 billion, down 26.3% year-on-year, and adjusted net profit margin dropped from approximately 14.0% to 10.0%.

While advertising revenue continues to grow, live-streaming revenue declines, and profit margins face pressure from increased investment. The valuation logic for Kuaishou has shifted from a "growth platform" to a "cash flow platform."

Tencent itself has also been consistently divesting from external investments. By the end of 2021, Tencent fully exited its stake in JD.com through a shareholder dividend distribution, reducing its holding from 17% to 2.3% and completely withdrawing from JD.com's board. In 2022, Tencent continued to reduce its stakes in various platform companies, including Meituan, SEA, and New Oriental, lowering its stake in Meituan from 17% to less than 2% and simultaneously relinquishing its board seats.

Kuaishou's announcement emphasized that Tencent's stake reduction does not negate Kuaishou's fundamental strengths, and both parties will continue to maintain a mutually beneficial relationship.

However, the underlying message is clear: Tencent is no longer willing to pay a strategic premium for mature platform stocks.

02. Bypassing Kuaishou, Targeting "Kling" Directly

While divesting its stake in Kuaishou, Tencent has invested in Kling.

The current financing round for Kling AI has an upper limit of RMB 20.447 billion, with a post-investment valuation of approximately US$18 billion. Post-financing, Kuaishou's stake in Kling will decrease to about 68%, while Tencent, Alibaba, Baidu, and others will join the investor roster.

This signifies that Kling is no longer merely an internal AI project at Kuaishou but an asset independently valued by external capital.

According to Kuaishou's financial report, Kling's annual recurring revenue (ARR) was approximately US$500 million in March, with first-quarter revenue of RMB 650 million. While this growth is rapid, it still accounts for less than 2% of Kuaishou's total revenue of RMB 33.7 billion. This underscores Kuaishou's current valuation dilemma: its most promising asset remains small in scale, while its largest core business has limited growth potential.

Tencent's "sell one, invest in another" strategy effectively dismantles Kuaishou.

Kuaishou represents a mature platform asset, while Kling represents an AI video asset. Previously, buying Kuaishou stock meant acquiring both in a package. Now that Kling is being independently financed and valued, Tencent can bypass the parent company's valuation discount and directly acquire a more precise AI stake.

This is more alarming than simply interpreting it as "Tencent is bearish on Kuaishou." It means Tencent no longer wants to buy into Kuaishou's new narrative using the old valuation structure of its parent company.

03. Capital Flows Toward AI and Tencent Itself

In the first quarter of 2026, Tencent reported revenue of RMB 196.5 billion and free cash flow of RMB 56.7 billion, with net cash of RMB 146.9 billion at the period's end. It faces no pressure to replenish cash flow. The real change is that Tencent's capital allocation priorities for external platform stocks have shifted.

Tencent's own funds are being allocated to higher-priority projects. In the first quarter, Tencent's capital expenditures reached RMB 31.9 billion, up 16% year-on-year, primarily directed toward AI computing power, servers, and data centers. While the AI cycle is longer, it directly serves Tencent's own advertising, gaming, cloud, and WeChat ecosystems.

Continuing to heavily invest in Kuaishou would neither provide control nor offer the same strategic leverage as in earlier years.

Share buybacks also represent a clearer calculation. In the first quarter, Tencent repurchased approximately HK$7.6 billion worth of shares. If the funds from selling Kuaishou shares were used to repurchase Tencent's own shares, it would directly enhance earnings per share and shareholder returns. Holding onto Kuaishou would mean enduring slower growth in its core business, uncertainty around Kling's performance, and volatility in Hong Kong-listed internet stocks.

Therefore, the core of this stake reduction is not about "cashing out to fund AI" but about reordering capital priorities. Kuaishou has shifted from being a "strategic insurance" to a "monetizable asset."

Of course, the stake reduction does not represent a complete severance. Tencent still holds a 9.37% stake in Kuaishou, and business collaborations such as WeChat traffic integration, e-commerce cooperation, and advertising partnerships will continue. However, the relationship has evolved from strategic synergy under equity binding to more market-driven commercial cooperation.

04. Kuaishou: Short-Term Buybacks, Long-Term AI Transformation

After Tencent's stake reduction, Kuaishou's valuation has been split into two parts: the revaluation of AI assets brought by Kling and the re-emergence of a maturity discount for the parent company after Tencent's exit as a major shareholder.

This explains the starkly different stock price reactions on July 6 and July 7. On the first day, the stock price surged as the market focused on Kling; on the second day, it plummeted as the market reacted to Tencent's stake reduction.

Going forward, the market will scrutinize whether Kling's revenue can continue to double, whether Kuaishou's AI investments will further suppress profit margins, and whether Kling can truly integrate into Kuaishou's advertising, e-commerce, short-form drama, and creator ecosystems.

If Kling remains merely an independent AI tool and Kuaishou is just its majority shareholder, the parent company will only receive an "investment holding discount." Only if Kling can seamlessly integrate into advertising material generation, product marketing, live-streaming clips, short-form drama production, and creator content creation, becoming a productivity tool within Kuaishou's commercial system, can Kuaishou truly capture valuation upside.

This represents the dividing line for Kuaishou's future stock performance. In the short term, the focus is on buybacks; in the medium term, on Kling's revenue; and in the long term, on whether AI can transform Kuaishou's core business.

Tencent's stake reduction in Kuaishou does not signify a rupture in their relationship, nor is it a simple financial cash-out. It more closely resembles the formal end of the old internet alliance era. In the past, major companies relied on equity alliances, traffic integration, and capital positioning, but that era is now drawing to a close. Today, Tencent has sold some of its Kuaishou shares while retaining Kling, exiting old platform stocks, and preserving its AI options.

For Kuaishou, the truly pressing question is not why Tencent sold but whether the market will continue to buy into the "Kuaishou whole story" when even Tencent chooses to bypass the parent company and directly bet on Kling.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models