Multi-short showdown at HSI 18,000, Hong Kong stock valuations expected to recover!

07/04 2024

07/04 2024

781

781

The three major Hong Kong stock indices surged in the morning session and maintained high-level volatility in the afternoon, with market sentiment recovering significantly. As of market close, the Hang Seng Tech Index rose the most, gaining 0.63%. The Hang Seng Index and the China Enterprises Index rose 0.28% and 0.23% respectively, with the Hang Seng Index briefly regaining the 18,000-point mark. However, after opening higher, the gains narrowed, and as of market close, the Hang Seng Index gained 0.28%. New energy vehicle stocks performed strongly, and Apple concept stocks showed improvement.

The 2024 World Artificial Intelligence Conference and High-Level Conference on Global Governance of Artificial Intelligence, themed "Promoting Shared Development through Consultation and Good Governance through Intelligence," opened in Shanghai on July 4. Focusing on core technologies, intelligent terminals, and application empowerment, it highlighted key areas such as large models, computing power, robots, and autonomous driving, showcasing a batch of the latest achievements in "AI+" innovative applications and launching a series of highly anticipated innovative products.

Foreign institutions have successively raised their growth expectations for the Chinese economy and indicated that as the AI boom continues to drive stock market gains, they expect China to eventually develop an AI ecosystem distinct from other regions, bringing significant monetization potential and thus benefiting the Chinese internet industry. UBS emphasized in a report that despite the decline in the MSCI China Index since May, it maintains an overweight rating on Chinese stocks, expecting them to outperform other markets as policy support and corporate earnings stabilize.

Looking back at the first half of 2024, the Hong Kong stock market experienced ups and downs, with winds and clouds. At the beginning of the year, the Hang Seng Index once fell to a near one-year low of 14,794.16 points, but then in late April, Hong Kong stocks embarked on a powerful rebound, firmly entering a technical bull market and becoming the focus of global markets. Although the Hong Kong market has seen a slight correction recently, fluctuating within a support range, it has not hindered institutions and investors' eager anticipation of a rally in the second half of the year.

In terms of the broader market, many institutions believe that the Hang Seng Index will break through the 20,000-point mark, with Guosen Securities even giving an ultra-strong forecast of up to 21,500 points. In terms of sectors, high-dividend assets and the internet sector have become hot targets for major institutions, and some institutions are also bullish on mainland property stocks. CCB International proposed that the current rebound momentum of Hong Kong stocks has surpassed that of a bear market oversold rebound, emphasizing the importance of stabilizing at 18,000 points as an important indicator of Hong Kong stocks truly completing the bear-to-bull transition.

Historically, after a technical bull market and short-term pullback at the bottom of a bear market cycle, there is a greater possibility of continued mid-term gains. Currently, almost all of the index gains come from valuation repairs brought about by risk premium adjustments. In the future, sustained policy benefits, declining risk-free yields, and continuous improvement in fundamentals will be needed to support Hong Kong stocks to continue to rise.

CCB International expects Hong Kong stocks to continue to rise in the third quarter, with increased volatility and fluctuations in the fourth quarter. The Hang Seng Index is expected to fluctuate between 17,500-22,500 points, the China Enterprises Index between 6,000-7,500 points, and the Hang Seng Tech Index between 3,500-5,000 points. It is recommended to maintain a range trading and barbell configuration strategy in the second half of the year.

In the first half of this year, according to statistics, at least 180 Hong Kong stock companies implemented share repurchases, totaling HK$121 billion, setting a new high for the same period in history. Especially among internet companies, almost every shareholder return plan has been significantly improved, signaling the beginning of a new era of internet shareholder returns.

Among these companies, Tencent, the "pillar" of Hong Kong stocks, is undoubtedly the most prominent. In the first half of this year, Tencent Holdings (00700.HK) contributed more than 40% of the Hong Kong stock market's repurchase volume with HK$52.3 billion, firmly occupying the throne of the "King of Repurchases" in Hong Kong stocks. In the second quarter, Tencent's quarterly repurchase amount reached HK$37.5 billion, doubling from HK$14.8 billion in the first quarter. The average repurchase price increased from HK$290.6 to HK$361.8, representing a nearly 25% increase.

China Ping An (02318.HK) closed down 0.54%. On the news front, China Ping An passively consolidated Lu Kong (06623.HK), with no change in Lu Kong's main business. On July 3, China Ping An and Lufax Holding issued a joint announcement on the Hong Kong Stock Exchange stating that due to China Ping An's election of stock dividends to receive corresponding dividends from Lufax Holding's special dividend distribution (after which China Ping An's controlling stake in Lufax Holding will reach 56.82%), it will passively consolidate Lufax Holding, triggering a mandatory general offer under the Hong Kong Takeovers Code.

BYD Co., Ltd. (01211.HK) closed up 1.91%. A report by market research firm Counterpoint Research on Tuesday, July 2, stated that Chinese electric vehicle manufacturer BYD is expected to surpass Tesla in pure electric vehicle sales in 2024, with BYD's pure electric vehicle market share expected to increase significantly. Counterpoint analysts wrote in the report that this shift underscores the dynamic nature of the global electric vehicle market.

Existing data shows that BYD's second-quarter battery electric vehicle sales increased nearly 21% year-on-year, reaching 426,039 units; while Tesla's second-quarter deliveries declined 4.8% to 443,956 units. Last year, BYD's total production, including pure battery-powered vehicles and hybrid vehicles, exceeded 3 million units, surpassing Tesla's 1.84 million units for the second consecutive year. However, in terms of pure electric vehicle production alone, BYD's 1.6 million pure battery passenger vehicle production level lags behind Tesla.

However, Counterpoint believes that China remains the dominant force in the pure electric vehicle market, with BYD leading the way. It is expected that China's pure electric vehicle sales will be four times that of North America by 2024; by 2027, China's market share in global pure electric vehicle sales will remain above 50%; and by 2030, China's pure electric vehicle sales will exceed the combined sales of North America and Europe.

Meanwhile, Deutsche Bank analyst Wang Bin wrote in a report that BYD Co., Ltd. (01211.HK) may achieve strong profit growth in the second quarter after setting a new monthly sales record in June. BYD's net profit for the second quarter is expected to be RMB 8.6 billion, representing a year-on-year increase of 26%. The net profit per vehicle in the second quarter is expected to increase from RMB 6,300 in the first quarter to RMB 8,000. The strong delivery of the Qin sedan family, especially the Qin L sedan, equipped with BYD's latest plug-in hybrid technology, has supported sales. Orders for the Qin L are three to four times higher than those for the Qin+ sedan without this technology.

A research report from Central China Securities pointed out that the current economy is in a stage of solid recovery, but the foundation for recovery is still unstable, requiring continued efforts to boost demand and promote a sustained recovery in sentiment. With the decline in PCE prices, the probability of the Federal Reserve cutting interest rates in September has increased. The overall stock index is expected to maintain a volatile pattern in the future, while still requiring close attention to changes in policy, capital, and external factors. We recommend that investors pay attention to investment opportunities in industries such as semiconductors, tourism and hotels, and batteries in the short term.

Huatai Securities also gave a similar view, noting that tourism demand remains strong, validating the resilience of emotional consumption. In the first half of 2024, holiday travel performance was better than per capita spending. Influenced by official promotion and thematic marketing, cost-effective and lower-tier city destinations have become a new trend in travel, with the "silver hair travel" market heating up and demand showing diverse and personalized new trends. Leading companies on the supply side are actively promoting content upgrades and project expansion, with transportation improvements and the recovery of aviation resource supply benefiting the enhancement of domestic tourism reception capacity and the recovery of cross-border tourist flows. Attention is recommended to be paid to layout opportunities during the summer peak season.

A Jefferies research report pointed out that after showing weak demand in May and June, China's sports apparel brands face downside risks in their 2024 retail sales targets. Even after adjusting the data based on changes during the 618 promotion period this year, the overall demand for sportswear in June was still weaker than in May. Factors such as consumer downgrading, insufficient product innovation, and ineffective Olympic marketing have all affected sales.

Meituan-W (03690.HK) closed up 2.22%. On the news front, Meituan's "God Member" program has been comprehensively upgraded, covering multiple categories including takeaway services, food group buying, hotel accommodation, leisure entertainment, beauty and health, and home services for the first time. It is reported that this is the largest revision since the launch of the "God Member" product, providing consumers with more cost-effective services and benefits. This time, the "God Member" introduced a savings wallet with different red envelope specifications. After joining the "God Member" service, the basic 5-yuan God Coupon can expand different discount amounts based on different experience scenarios, with a maximum expansion of up to 100 yuan. As of July 4, the number of merchants signing up for the "God Member" has reached 5 million.

SenseTime-W (00020.HK) closed down 0.62%. SenseTime released its first "controllable" human video generation large model, Vimi, which is primarily targeted at C-end users and supports various entertainment interaction scenarios such as chatting, singing, and dancing. According to SenseTime, Vimi can generate single-shot human videos up to 1 minute long, with image quality that does not deteriorate or distort over time. Based on SenseTime's Daily New large model, Vimi can generate human videos consistent with target actions using a photo of any style, and can be driven by various elements such as existing human videos, animations, sounds, and text.

Kuaishou-W (01024.HK) closed down 4.58%. Morgan Stanley downgraded Kuaishou's stock rating from overweight to neutral due to rising sales and marketing expenses leading to a decline in the company's share growth and a slowdown in profit margin expansion. During the 618 shopping festival, Kuaishou's annual growth rate in live streaming e-commerce GMV fell from 124% in 2022 and 28% in 2023 to 12% in 2024. Its target share price was reduced from HK$70 to HK$55.

Hon Hai Precision Industry (06088.HK) rose by over 8%. CMB International said it is optimistic about Hon Hai Precision Industry's diverse growth drivers emerging in the second half of 2024 and 2025, benefiting from strong growth in AI servers, the AI mobile phone/PC upcycle, progress in new automotive business projects, and synergistic effects with its parent company Hon Hai Group in AI server and iPhone business. The current valuation level remains attractive. Guotai Junan pointed out that the rapid growth of the AI industry has brought many growth opportunities for data center interconnectivity, and optical module manufacturers and connector manufacturers such as Hon Hai Precision Industry will benefit from it.

In addition, Zhang Bokai, head of the technology industry research department of Goldman Sachs Greater China, analyzed that the shipment momentum of two major products, iPhone and AI servers, is the key to driving Hon Hai's future operational growth. Morgan Stanley raised its target price for Hon Hai to NT$255, citing the potential increase in iPhone replacement demand as Apple's smartphones hit the market.

AAC Technologies Holdings (02018) rose nearly 6%. HSBC issued a research report stating that it is optimistic about AAC Technologies' leading position in microphone and thermal management solutions ahead of the upcoming era of artificial intelligence (AI) mobile phones. HSBC believes that overheating issues may become a key factor that smartphone manufacturers need to address in terms of AI-phones, and is optimistic about AAC Technologies' business in this area, believing that the business is in a favorable position in terms of potentially migrating cooling technology from Apple in the future. In addition, the market is gradually realizing the important role of voice assistants in the upcoming era of artificial intelligence smartphones, which may trigger another round of microphone specification upgrades.

CCB International previously pointed out that the positive development of all its market segments will drive the continued recovery of its sales and profit margins for the 2024 fiscal year. AAC Technologies' improving prospects are mainly attributed to the rebound in the smartphone market; AI-driven opportunities from major US customers; improved utilization and average selling prices; and favorable changes in product mix.

XPeng Motors-W (09868.HK) rose 4.15%, NIO-SW (09866.HK) rose 5.03%, and Li Auto-W (02015.HK) rose 3.92%. On the news front, according to preliminary statistics from the China Passenger Car Association, from June 1 to 30, retail sales of passenger cars reached 1.755 million units, down 8% year-on-year and up 2% month-on-month. The cumulative retail sales for the year to date reached 9.828 million units, representing a year-on-year increase of 3%. Retail sales of passenger car new energy vehicles reached 864,000 units, representing a year-on-year increase of 30% and a month-on-month increase of 6%. The cumulative retail sales for the year to date reached 4.119 million units, representing a year-on-year increase of 33%.

Minsheng Securities pointed out that the singularity of automotive intelligence has arrived, bringing opportunities for independent technology output and incubation. Automotive intelligence will become an important factor in the competition among automakers. On July 3, XPeng Motors' XPeng MONA M03 made its global debut, targeting the 10-150,000 yuan market segment and is expected to officially launch in August. CICC believes that on a reasonable pricing basis, autonomous driving is expected to differentiate itself in this price range, and is optimistic about the subsequent sales performance of the MONA series models.

JP Morgan also issued a research report stating that Geely Automobile's first-quarter results this year met expectations and predicted that both the profit margin in the second quarter and the second half of the year would improve, reaching similar levels as in the second half of 2023. The bank expects Geely to achieve its sales target of 1.9 million units this year, mainly based on the company's launch of a new generation of plug-in hybrid electric vehicles (PHEV) and accelerated sales of existing models. In addition, due to economies of scale and cost savings through the group's shared platform, the bank expects Geely's profit margin performance to continue to improve. Based on the above factors, JP Morgan set Geely's target price at HK$10 and maintained a "neutral" rating.

Bilibili-W (09626.HK) closed up 2.45%. Morgan Stanley issued a technical research report stating that Bilibili's share price has a roughly 70-80% chance of rising in the next 60 days, giving it a US target price of $15 and a rating of "in line with the market." Morgan Stanley expects Bilibili to raise its third-quarter earnings guidance when releasing its second-quarter results in August to reflect the boost in advertising revenue driven by its gaming vertical.

The bank also expects Bilibili's third-quarter gaming revenue to increase by more than 700 million yuan on a quarter-on-quarter basis, representing a year-on-year increase of over 70%, mainly driven by the newly launched game "Three Kingdoms: Strategy of the World" on June 13. This forecast demonstrates Bilibili's strong growth potential in the gaming sector and its positive prospects in the advertising business. As a video sharing website with young people as its main user group, Bilibili's business growth and market performance have always been closely watched by investors and analysts.

Weimeng Group (02013) rose by over 0.69%. On the news side, recently, Weimeng Marketing and Tencent Advertising jointly held the "Service Vision Soars Up Global Growth" clothing industry GGP closed door event in Shanghai. At the event, Tencent Advertising awarded Weimeng the "Clothing Industry GGP Service Provider" license, and the two sides will work together to support the overall business growth of clothing brands in areas such as integrated marketing, video account live streaming operations, and online and offline integrated management.

According to a recent research report by Open Source Securities, Weimeng is a core agent of Tencent's social advertising, benefiting from macro recovery and video account growth. In 2023, the company's gross revenue from commercial solutions increased by 44.5% year-on-year. Revenue increased by 60.5% year-on-year, and the company is expected to continue to benefit from video account dividends in the future. Some customers of precision marketing and SaaS business overlap to have synergistic effect. At the same time, the company actively expands channels such as Kwai and Little Red Book.

For the subsequent trend of the market, the Swedish Pension Colonial First State expressed its focus on Chinese securities with lower prices, seeking to increase emerging market risk exposure to diversify its asset portfolio. The company manages a pension and wealth scale of AUD 150 billion (USD 101 billion) and currently has no risk exposure in the Chinese market.

Bank of China International has released a research report, predicting that the Hong Kong stock market will continue to fluctuate significantly in the second half of this year. However, it is cautiously optimistic about the trend of the Hong Kong stock market in the second half of this year, believing that the "National Nine Articles" will play a key role in the healthy development of the Hong Kong stock market. At the same time, it also looks forward to introducing more policies in the second half of this year to improve the liquidity of the Hong Kong stock market.

The bank pointed out that the current valuation of the Hong Kong stock market is still attractive, and it is expected that the Hang Seng Index will see a 20010 point mark at the end of the year. It is optimistic about high interest stocks, companies benefiting from the Southern Link, and high growth stocks with strong competitive advantages in their industries.

BOC International recommends Tencent (00700. HK), CCB (00939. HK), ABC (01288. HK), ICBC (01398. HK), CMB (03968. HK), China Mobile (00941. HK), Meituan-W (03690. HK), Xiaomi-W (01810. HK), PetroChina (00857. HK), Sinopec (00386. HK), CNOOC (00883. HK), Fuyao Glass (03606. HK), China Shenhua (01088. HK), China Telecom (00728. HK), China Railway (00390. HK), Huaneng International (00902. HK), China Power (02380. HK), Wanzhou International (00288. HK), Pinduoduo (PDD. US), and Kwai - W (01024. HK).

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

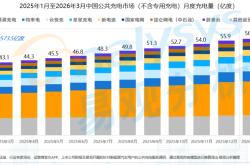

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

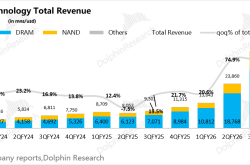

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!