It's exploding, completely exploding, with huge good news coming, and everyone is going wild!

06/11 2024

06/11 2024

759

759

This is the 939th original article from the front of new energy. Click on the 'Front of New Energy' above to follow and "star" this account. The article only records the thoughts of "Front of New Energy" and does not constitute investment advice. The author does not have a group, does not charge for stock recommendations, and does not manage finances on behalf of others. -------

After a long period of sluggishness, the new energy vehicle market finally ushered in great good news in May!

Time flies so fast, blink of an eye, another month has passed, and the results of the monthly "big test" for new energy vehicle manufacturers are out again. This time, they generally achieved good results, but the differentiation is also very serious. Some continue to be fierce, some are making a comeback, and of course, some are still sluggish.

01 Aion and Lixiang caught a break

Aion, which performed well in 2023 but showed signs of decline in 2024, sold 40,073 vehicles in May, down 11% year-on-year but up 42.5% month-on-month.

Although it's not as high as the peak of 50,000 vehicles, it's already quite impressive to achieve a monthly sales of 40,000 in this year's fast-paced new energy vehicle market, especially when the online car-hailing market is shrinking and Aion's sales are mainly focused on online car-hailing.

For Aion, if it wants to return to its peak or even make further breakthroughs, the core is to launch new models as soon as possible and figure out how to leverage its B-end reputation to make breakthroughs in the C-end market, rather than always being positioned in the online car-hailing market.

Actually, BYD's approach is worth learning from, which is to use cutting-edge technology to reposition users' minds. Of course, the premise is that GAC has corresponding technical reserves, as not everyone can be like BYD with so many technical reserves.

Aion and Lixiang's performance has been highly similar since last year and this year, both shining brightly last year but encountering some setbacks this year, and their performance in May was also similar.

Lixiang delivered 35,020 new vehicles in May, also the first brand to announce sales, up 23.8% year-on-year, regaining the title of the sales champion among new forces. This is naturally due to the launch of L6, which delivered over 15,000 vehicles in May.

We have talked about Lixiang several times before. Objectively speaking, it is a very excellent company, but it also faces a lot of competitive pressure. Too many competitors are targeting it, especially NIO, which is almost pixel-level imitation from product to marketing.

This is a problem that industry leaders have to face. Whether they can stand out from this competitive environment and find a breakthrough for further progress depends on the management team.

The company will no longer launch pure electric models in the second half of the year, mainly relying on the L series to support sales. Besides price reductions, what other cards do they have? This is a concern, and Lixiang needs to move faster.

02 Xiaopeng Motors' "small" status may not last

NIO delivered 20,544 vehicles in May, setting a new record!

This is very rare and congratulatory. The main reason is naturally the new BaaS policy. Although many people think that the battery leasing cost of seven or eight hundred to a thousand yuan per month is not low, especially for some pure electric car owners, from another perspective, many NIO target users also spend that much on fuel every month. With similar costs, switching to a better-experienced car is not a bad deal.

We have talked a lot about NIO before. We always say that it has many cards in its hand and has built a good brand. Its cars are also good in terms of positioning, appearance, interior, and configuration. The painstakingly built battery swap network is also gradually attracting more partners. In addition, it has also launched a sub-brand called LeDao, which has quite a few highlights.

However, NIO cannot be said to have completely reversed its situation now. The record sales in May were also driven by the launch of Xiaomi's SU7 and the promotion of the new BaaS plan, but how sustainable it is remains to be seen. In addition, it is still uncertain whether LeDao will succeed and whether its sales will affect the main brand NIO. We'll have to wait and see.

Compared to NIO and Lixiang, which seem to be climbing out of the hole, Xiaopeng is still in the hole and has clearly fallen behind. In May, Xiaopeng sold a total of 10,146 vehicles, up 35% year-on-year and 8% month-on-month, but mainly due to its poor performance last year and this year.

The problems of Xiaopeng Motors have been mentioned many times, both product and marketing issues, which are big problems. Although He Xiaopeng has been working hard to improve for more than a year, there has been no significant change in these two issues.

Previously, when He Xiaopeng was interviewed, he hinted that there might be the possibility of developing hybrid or extended-range vehicles, which is indeed a possibility to survive. But if Xiaopeng cannot make up for its shortcomings in product and marketing, launching any new product will be useless.

Xiaomi delivered 8,630 vehicles in May, aiming for over 10,000 vehicles in June and promising to deliver at least 100,000 vehicles and striving for 120,000 vehicles in 2024. Lei Jun is indeed Lei Jun. If Xiaopeng doesn't change quickly, Xiaomi will take over the "small" position in the "NIO-Xiaopeng-Lixiang" trio, just like how Baidu (B in BAT) has actually become ByteDance.

Leopard Motors delivered 18,165 vehicles in May, up 51% year-on-year and 16% month-on-month. Although the month-on-month growth rate is not too impressive compared to other manufacturers, Leopard has performed well this year, unlike other manufacturers who struggled in the first few months of this year.

We have talked about Leopard Motors many times before and quite like this company. While continuing to make steady progress in the domestic market, further breakthroughs will depend on international business, and it is expected to be the first to go on sale in Europe in September.

03 The strength of established automakers

ZEEKR delivered 18,616 new vehicles in May, up 16% month-on-month and 115% year-on-year, setting a new record! After refreshing its lineup at the end of February this year and adopting the approach of price reductions and increased volumes, ZEEKR has stabilized itself in this highly competitive market with its product strength, especially its competitiveness in hardware.

With a solid foundation and strong support from the Geely Group, ZEEKR deserves a better future, which is also a reflection of the strength of traditional automakers.

SL03 delivered 14,371 vehicles in May, doubling year-on-year and increasing 13% month-on-month. Although it's not bad, it's actually a bit lower than expected from our perspective. Besides the changing market, it's also related to the strong cost-effectiveness of its sibling brand Qiyuan. The Qiyuan A07, a B-class car, only costs the price of an A-class car, and can achieve a range of 710km with a landing price of 160,000 yuan. It also has a frameless door and good looks. Even in the highly competitive Chinese new energy vehicle market, its cost-effectiveness is still prominent, which explains why it sold 13,557 vehicles in May.

Although SL03 and Qiyuan have made some distinctions in positioning, as Qiyuan's cost-effectiveness becomes more prominent, SL03's attractiveness will inevitably decrease, and its subsequent sales may be significantly affected.

Wenjie did not disclose its sales separately in May but instead released data with HarmonyOS Intelligence, delivering 30,578 new vehicles in total, up 3.19% month-on-month. Among them, the Wenjie M9 delivered 15,873 vehicles in May. In addition, the new M5 has reached 20,000 orders in just one month since its launch, and the newly launched M7 Ultra exceeded 12,000 orders on its first day. Although the title of the sales champion among new forces was taken back by Lixiang, with Huawei's support, Wenjie's sales are still worth looking forward to.

Finally, the main event is still BYD.

04 BYD unleashes a double whammy

BYD sold 331,800 new energy vehicles in May, up from 240,200 in the same period last year and 313,200 in April. Cumulative sales from January to May reached 1.2713 million vehicles, maintaining a relatively rapid growth trend overall.

There's no way around it; BYD really has a lot of cards. Just the price war alone is enough for BYD to play for a while. Of course, in the increasingly competitive Chinese new energy vehicle market, price wars alone are clearly not enough. Ultimately, it still comes down to product strength, and the core of product strength is technology.

Therefore, at the end of May, BYD grandly launched its fifth-generation DM technology, which achieves the world's highest engine thermal efficiency of 46.06%, the world's lowest fuel consumption of 2.9L per 100 kilometers under power loss conditions, and the world's longest comprehensive range of 2,100 kilometers. At the same time, it also released the Qin L DM-i and the Seal 06 DM-i, which are supported by cutting-edge technology. Along with the price tag, the starting price of the Qin L equipped with the fifth-generation DM technology is 99,800 yuan...

Leo even wants to sell his Han EV and get a Qin L, but after being stabbed in the back by BYD too many times, he can't make up his mind to switch to their cars – "I recommend it if you buy, but I won't buy it if I buy."

Overall, the sales of most automakers have gradually recovered in May, and as competition intensifies, the cost-effectiveness of many cars is becoming more prominent, and the market is rebounding quickly. However, inevitably, as the penetration rate of new energy vehicles has reached a relatively high level, industry differentiation is inevitable. The time and opportunities left for players on the field are getting fewer and fewer. Those who can't make a breakthrough this year will face increasing troubles in the future.

-

![]()

Personnel Shuffle: Independent Director Mi Xuming Steps Down from OFILM

-

![]()

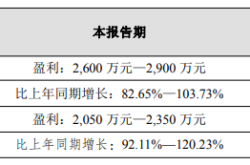

Net Profit Anticipated to Skyrocket by 103%: What Gives This Optical Company a Competitive Edge?

-

In Just One Year, China Unveils Unicorns Valued at 10 Trillion Yuan!

-

![]()

6 Park Companies Shine at WAIC: How Hong Kong Science Park Bridges AI from Research to Industry

-

![]()

Wang Wenjing’s Third Act: Can Yonyou Reinvent Itself in the AI Era?

-

![]()

Performance Coupe Entry Threshold Reduced to 170,000 Yuan: Assessing the 2027 Exeed ES's Prospects

-

![]()

Battery "Crisis" for 4 Million New Energy Commercial Vehicles

-

【Focus】Fluorinated Photosensitive Polyimide (FPSPI): A High-End Subdivision of PSPI with Great Potential in High-Tech Industries