Has CATL Dominated the Auto Market's Profits?

08/21 2025

08/21 2025

795

795

Who are automakers truly serving?

Earning 30.4 billion yuan versus losing over 1.8 billion yuan—these figures starkly illustrate the contrasting net profit performance of CATL and GAC Group in the first half of 2025.

"Power battery costs now account for 40% to 60% of our car costs. Am I not just working for CATL?" This lament by Zeng Qinghong, chairman of GAC Group, echoed at the 2022 World Battery Conference, where the notion that "automakers are working for CATL" gained widespread industry recognition.

Three years on, this trend remains largely unchanged. Even the combined net profit of all A-share listed automakers struggles to compete with CATL.

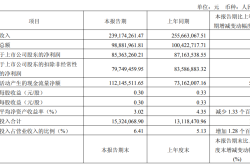

According to recent financial reports, CATL's operating revenue for the first half of the year reached 178.886 billion yuan, a 7.27% year-on-year increase, with a net profit of 30.485 billion yuan, up 33.33% year-on-year, setting a new record for net profit. In contrast, GAC Group sold 755,300 vehicles in the first half but expects losses of 1.82 billion to 2.6 billion yuan.

Selling cars pales in comparison to making batteries, leaving automakers feeling helpless.

"Ice and Fire" in Profit Distribution

Higher profit margins upstream than downstream, and greater gross profit margins for suppliers than system integrators, are common phenomena across industries. However, the profit disparity between vehicle manufacturers and battery enterprises is particularly striking.

In the first half of 2025, the auto industry's production and sales scale hit a new high, but profit margins declined compared to the same period last year. According to the China Association of Automobile Manufacturers, China's auto production and sales volume surpassed 15 million units for the first time in the first half of 2025, achieving double-digit year-on-year growth. However, National Bureau of Statistics data shows that in the first half of 2025, China's auto industry generated a total revenue of 5.09 trillion yuan, with a net profit of 244.4 billion yuan and a profit margin of 4.8%, a decrease of 0.2 percentage points from 5.0% in the same period last year.

Image source: CATL official website

Despite this, CATL's financial report for the first half of 2025 reveals astonishing profitability. Its net profit attributable to shareholders of listed companies was 30.485 billion yuan, a 33.33% year-on-year increase; net cash flow from operating activities was 58.687 billion yuan, up 31.26% year-on-year. In terms of main businesses, revenue from power battery systems amounted to approximately 131.573 billion yuan, a 16.8% year-on-year increase, accounting for 73.55% of CATL's total revenue during the same period, an increase of 3.65 percentage points compared to 69.9% in 2024.

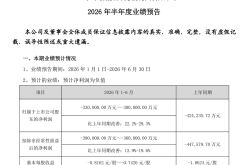

Listed automakers generally lag behind CATL in net profit performance. GAC Group expects a net profit loss attributable to shareholders of listed companies of 1.82 billion to 2.6 billion yuan in the first half of the year, turning a profit into a loss. BAIC BluePark anticipates a net profit loss of 2.2 billion to 2.45 billion yuan, while JAC Motors expects a net profit loss of approximately 680 million yuan.

Among the few listed automakers achieving profitable growth, Thalys stands out, but its net profit attributable to shareholders of listed companies is expected to be only between 2.7 billion and 3.2 billion yuan, a 66.20% to 96.98% year-on-year increase; non-deductible net profit is expected to be between 2.23 billion and 2.73 billion yuan, up 55.13% to 89.92% year-on-year. Foton Automobile also achieved a year-on-year increase of 87.50%, but its net profit attributable to shareholders of listed companies in the first half of the year was only 776.6 million yuan; non-deductible net profit was 530.05 million yuan.

Notably, CATL's gross profit margin for its power battery business was 22.41%, a slight decrease of 1.07% compared to the same period last year, making it the only business segment to experience a decline. Revenue from energy storage battery systems was 28.4 billion yuan, down 1.47% year-on-year, but operating costs fell by an even greater margin of 2.92%, pushing the gross profit margin up to 25.52%, an increase of 1.11 percentage points year-on-year.

Another noteworthy data point comes from the China Automotive Battery Industry Innovation Alliance. According to their data, in the domestic power battery enterprise vehicle loading volume rankings from January to June 2025, CATL remained at the top with a power battery loading volume of 128.6GWh, but its growth rate lagged behind the overall market, with a loading volume share of 43.05%, a year-on-year decrease of 3.33 percentage points, making it the company with the largest share decline among the top 15. This signifies that CATL faces certain challenges in maintaining its market share.

In Goldman Sachs' in-depth review of CATL's second-quarter 2025 financial report, the company's performance exceeded market expectations overall, but it showed signs of slowing revenue growth and profit pressure in its core power battery business segment. Goldman Sachs lowered its profit forecasts for CATL (03750.HK) by 1%, 5%, and 3% for 2025-2027, respectively, primarily reflecting the expected decline in battery unit gross margins, underpinned by intensified industry competition and persistent price pressure.

Breaking Free from CATL's Dominance?

While CATL is a partner to automakers, providing them with key power batteries to advance in the new energy vehicle sector, it also leverages its advantages in battery technology, production capacity, and other aspects to hold significant discourse power in collaborations, placing automakers in a relatively weak position in profit distribution.

Amidst cost reduction, efficiency enhancement, and price wars, subtle changes are underway. The cooperative relationship between some automakers and CATL is evolving, with some automakers beginning to strategize their entry into the battery industry.

Some automakers once deeply tied to CATL are now attempting to "decouple." For example, CATL was once XPeng's main supplier, but XPeng is now diversifying its battery manufacturers. After Ideal Auto invested in Sunwoda in 2022, it expanded its supply share to 10 vehicle models. NIO's stance is even clearer; after introducing CALB, its sub-brand Lido is directly supplied by BYD. In July this year, Farasis Energy announced that it had received a "Notice of Fixed-Point Development" for certain vehicle parts from GAC Group, selecting the company to develop and supply battery pack assemblies. According to customer sales forecasts and arrangements, supply will commence within the year.

Extending business into the battery industry has also become an option for some automakers. At the Shanghai Auto Show in April this year, Geely announced the integration of its battery business to form the "Ji Yao Tong Xing" company, with a capacity of 50GWh to be implemented this year, aiming for 70GWh by 2027 to meet one-third of its own demand.

GAC Group announced the establishment of the "Green Engine" battery company with a total investment of 10.9 billion yuan as early as August 2022. When it was officially registered in October 2022, it was renamed "InPower Battery," and by the end of 2023, two 12GWh mass production lines had been completed. In May this year, GAC announced that it will complete the construction of an additional 36GWh within a year and a half to meet the demand for 600,000 new energy vehicles. GAC's total planned battery project of 60GWh is expected to be realized by the end of 2026.

Notably, GAC Group even deregistered the battery company jointly established with CATL, although this was only a company focused on battery system production and did not involve key links such as cell manufacturing. This move underscores GAC Group's determination to fully rely on itself for power battery research and development and layout.

One of the key reasons automakers are seeking to break free from CATL's dominance is cost. CATL's product costs are often higher, and in the current context of fierce price wars and cost reduction as the main theme in the auto industry, this puts pressure on automakers' costs. Of course, building their own battery factories is not easy for automakers, requiring substantial capital investment, technological accumulation, and talent reserves, while also facing challenges like rapidly increasing production scale and technology update pressure.

Industry Changes in the Making

From an industry development perspective, in the early stages of new energy vehicle development, power battery technology was a core competitiveness. Through continuous R&D investment, CATL has taken a leading position in key technical indicators such as battery energy density, safety, and fast charging, and its high profits are to some extent a reasonable reward for its technological innovation.

However, as the industry matures, the coordinated development of various links in the auto industry chain becomes increasingly important. If the power battery segment monopolizes most profits while the vehicle manufacturing segment struggles, it may hinder automakers' investments in other areas like vehicle intelligence research and development, brand building, and after-sales service improvements, which is detrimental to the sustainable development of the entire auto industry.

With battery enterprises like BYD, EVE Energy, and CALB constantly catching up, market competition is intensifying, which may prompt CATL to reduce product prices and improve product quality and service levels to maintain its market position. At the same time, by cooperating with more battery suppliers, automakers can enhance their supply chain discourse power, reduce procurement costs, and improve profit conditions.

In fact, to strengthen the competitiveness of its power battery systems, CATL has continuously expanded its business, such as developing battery swapping services and skateboard chassis businesses. CATL is also actively deploying other businesses, including energy storage batteries, battery material recycling, and battery mineral resource ventures. In the first half of this year, the gross profit margins of these businesses all increased. Revenue from energy storage battery systems was 28.4 billion yuan, down 1.47% year-on-year, accounting for 15.88% of revenue, with a gross profit margin of 25.52%; battery material and recycling revenue was 7.887 billion yuan, down 44.97% year-on-year, with a gross profit margin of 26.42%; battery mineral resource business revenue was 3.361 billion yuan, up 27.86% year-on-year, with a gross profit margin of 9.07%. Exports are also a new development direction for CATL. Financial reports show that in the first half of the year, CATL's overseas revenue was 61.208 billion yuan, accounting for 34.22% of current operating revenue, with the main products sold overseas still being battery systems.

CATL stated in its financial report that it will face multiple risks in the future, including intensified market competition, fluctuations in raw material prices, and supply issues. Notably, recent rumors of production suspension at CATL's "Jianxiawo" lithium mine in Yichun, Jiangxi Province, have attracted significant market attention. This rumor reflects potential uncertainty in its raw material supply, further exacerbating raw material supply risks. In response to the risk of raw material price fluctuations, CATL stated that it has taken measures such as self-mining, investment cooperation, and signing long-term contracts to ensure the safety and stability of the supply chain.

With intensified market competition, automakers seeking diversified cooperation, and the increasing intrinsic demand for profit balance in industry development, a situation where one company monopolizes profits is unsustainable in the long run. The auto industry requires the joint efforts of enterprises across all industry chain links to achieve a reasonable profit distribution and promote the healthy, stable, and sustainable development of the entire industry through technological innovation and optimization of cooperation models.

-

![]()

Is Tencent AI Heading in the Right Direction?

-

Latest Update! Jinding Optics’ GEM IPO Review Now “Under Inquiry”

-

![]()

VOYAH’s CBO Sets Ambitious Target: Secure Top 3 Spot in Luxury BEV Market Within Two Years, Launch 4 New Models to Cover All BEV Segments

-

![]()

Sehwa Technology Invests 740 Million Yuan, Eyeing the Lucrative Optical Film Market!

-

![]()

150 Million Users, $40 Million ARR: AIShige Technology Enters the Final Round of AI Video Competition

-

![]()

StepOn Star Forays into Smartphone Manufacturing: A Rationally Sound Yet High-Risk Endeavor

-

![]()

TCL Zhonghuan: Embracing a New Story Despite Anticipated Losses

-

![]()

Forty Years On: From Volkswagen’s State-Backed Entry into China to BYD’s Hiring of a Former European Foreign Minister