Antitrust 'Crackdown Wave' Hits the Automotive Industry

09/08 2025

09/08 2025

660

660

Antitrust enforcement in 2024 marks a transition from "sporadic crackdowns" to "systematic framework building," and from "case-by-case investigations" to "proactive rule-setting." For the automotive sector, this shift brings both compliance challenges and historic opportunities for systemic restructuring.

In June 2025, the State Administration for Market Regulation (National Antimonopoly Bureau) published the Annual Report on China's Antitrust Enforcement (2024) (hereinafter referred to as the Annual Report), signaling a pivotal shift: as the automotive industry accelerates toward intelligence and electrification, regulators are reshaping industry norms through a more forward-looking enforcement approach.

Through this Annual Report, one can clearly trace the evolution of policy and regulatory priorities, while also discerning profound transformations in the automotive industry regarding structural hierarchy, business practices, resource allocation, and compliance philosophies.

In contrast to the past "selective enforcement" approach, which focused on "high-profile cases and major penalties," the 2024 enforcement practices reveal a clear trend toward transformation—shifting from "reactive punishment" to "proactive prevention," with the automotive sector serving as a critical testing ground for this shift.

Firstly, there is a notable shift in policy stance. In early 2024, the State Administration for Market Regulation issued Reminder and Urgency Letters to the distribution networks of certain branded automakers for the first time, highlighting monopoly risks in their distribution management and demanding enhanced compliance oversight and self-inspection rectifications. This marked the first instance of the domestic antitrust regulatory system issuing a formal document as a "warning signal" to the automotive sales sector, widely seen within the industry as an upgrade in risk governance "from isolated points to systemic coverage."

Simultaneously, regulatory logic is advancing toward systemic governance. In 2024, a total of 17 new monopoly agreement cases were initiated nationwide, involving 78 enterprises and 1 industry association, with cumulative fines and confiscations exceeding 11.1 million yuan. Amid increasingly cross-regional brand operations and extended control chains, regulatory objectives have shifted from "investigating individual violations" to "mitigating systemic risks."

Governance Model in the Vehicle Inspection Industry

Vehicle inspections have long been a cornerstone of the automotive after-sales service system; however, in practice, this field has suffered from information asymmetry and restricted market access, becoming a breeding ground for price-fixing behaviors.

The Annual Report reveals that in 2024, 46 vehicle inspection agencies in Hunan, Tianjin, and Guizhou were investigated for participating in illegal monopoly agreements. Taking Tianjin as an example, in August 2023, 10 local inspection companies signed "Self-Regulatory Cooperation Guarantee Clauses," stipulating that the inspection price for small blue-plate vehicles would be no less than 150 yuan per vehicle, while establishing a "common fund" to distribute inspection revenues proportionally. This coordinated price-hiking behavior was deemed to violate Article 17 of the Anti-Monopoly Law, resulting in administrative penalties totaling 675,100 yuan imposed by regulatory authorities in October 2024.

From pricing agreements to profit redistribution mechanisms, these "alliances" demonstrated a high degree of organization and institutionalization, rather than being isolated market conspiracies. Therefore, regulatory efforts must not only "investigate violators" but also "dismantle cooperation networks"—breaking information monopolies, dismantling regional barriers, and fostering transparent pricing mechanisms.

More critically, the governance effects of such cases have begun to benefit end-users. Vehicle inspection prices have dropped by over 20% in some regions, and appointment waiting times have significantly decreased.

Antitrust, thus, serves not only as a regulatory tool but also begins to reflect its extended value as a livelihood policy, with its effects radiating toward both fair markets and public interests.

Tightening Compliance Red Lines in Distribution Systems

Compared to the "low-value, high-frequency" illegal characteristics in the inspection industry, compliance risks faced by branded automakers in their distribution systems manifest more as "implicit restrictions under high control."

The Annual Report discloses that in January 2024, the State Administration for Market Regulation formally summoned five joint venture and imported brands in China—Jaguar Land Rover, Audi, Volkswagen, BMW, and Mercedes-Benz—demanding self-inspections into potential illegal behaviors regarding price-setting, channel division, and sales incentive mechanisms, and urging strengthened compliance management.

Although this action did not directly lead to administrative penalties, its symbolic significance cannot be overlooked. For a long time, brand owners have influenced sales pricing and distribution through methods such as "suggested retail prices," "regional blockades," and "rebate structures," weakening dealers' independent bargaining power and substantially interfering with the normal operation of market competition.

Against the backdrop of rapid electric vehicle (EV) adoption and high inventory levels of traditional models, persisting with "inventory pressure + price control" strategies will not only intensify price competition but may also trigger prohibitive clauses on "vertical monopoly agreements" in the Anti-Monopoly Law.

In the future, the distribution system is expected to evolve toward greater transparency, digitization, and diversification. For instance, some emerging brands adopt a hybrid model of direct sales and authorized distribution, combined with C2M (Customer-to-Manufacturer) approaches to reduce channel layers and enhance user reach efficiency, providing a practical path for traditional brands' compliance transformation.

Centralized Trend in M&A Reviews Intensifies

In 2024, the automotive manufacturing sector emerged as the most concentrated sub-industry for M&A reviews within the manufacturing field. Out of 213 M&A cases in the manufacturing sector for the year, 31 involved automotive manufacturing, accounting for nearly 15%.

Behind this high density lies automakers' comprehensive competition for technology, data, and channel control amid the backdrop of "new three modernizations" (electrification, intelligence, and connectivity), with M&A serving as a core tool.

The Annual Report points out that regulators will continue to encourage rational integration and support strengthening and excellence; however, they will remain highly vigilant toward M&A cases involving critical market shares that could form monopoly structures.

This also implies that M&A activities in key areas such as intelligent driving, chips, and power batteries, if affecting market structure or restricting competition, will face stricter reviews and higher information disclosure thresholds.

For enterprises, the path of simply acquiring control through capital will be restricted, and cooperative models such as "platform collaboration" and "joint control" based on compliance will become more viable options. For example, mechanisms like cross-shareholding and joint research and development not only comply with regulatory requirements but also achieve mutual benefits for multiple parties.

Early Warning on Oligopoly Risks in the Charging and Battery Swapping Sector

The Annual Report specifically issues a competitive assessment opinion on the charging and battery swapping infrastructure industry, pointing out that some regional platforms have exhibited oligopolistic tendencies, manifesting as price convergence, closed interfaces, and account barriers, which may jeopardize the openness and diversity of the electric vehicle ecosystem.

This warning signal stems from the continuous promotion of charging pile "new infrastructure" layouts by national and local governments in recent years, as well as market concentration driven by multiple rounds of financial subsidy policies. However, behind rapid expansion, issues such as non-uniform standards and lack of interoperability mechanisms among platforms have become increasingly prominent, with poor interface compatibility and weak account interoperability between different platforms significantly raising user switching costs and limiting overall industry competitiveness.

Regulatory focus has also shifted from "quantity growth" to "platform openness." This not only affects end-consumer experiences but also determines automakers' service ecosystem extension capabilities.

It is anticipated that in the future, platform operators will face clearer institutional constraints and transparency requirements, such as promoting open interface protocols, strengthening cross-platform compatibility mechanisms, and standardizing data upload obligations, becoming key directions for antitrust governance in the infrastructure sector.

Image: From the Internet

Article: Auto Review

Layout: Auto Review

-

When Cost-Effectiveness Falters, Mobile Phone Sub-brands Engage in a Survival Showdown

-

![]()

Automotive-Grade Fragrance Generator: Safety as the Foundation, Pleasant Aroma as the Norm

-

![]()

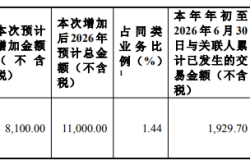

Tengjing Technology’s Revenue Projected to Soar by Over 50% in First Half of 2026!

-

![]()

Insta360 Ramps Up 'Bundling' with Upstream Optical Supply Chain with 110 Million Yuan in Related Procurement

-

![]()

Following NIO and CATL’s Footsteps, Guangzhou Nurtures Another Billion-Dollar Unicorn

-

![]()

No Choice for Mobile Phone Companies | Waves

-

![]()

From Jiyue to Li Auto and Saido: The Expedition of AI Cars Has Just Begun | Business Wave

-

![]()

Why Chinese Domestic Brands Are Embracing the Supercar Race Despite Its Unprofitable Nature