Auto Market Sees 17% Drop in Q1, but Trade-Ins Drive 246.8 Billion Yuan in Sales

04/13 2026

04/13 2026

530

530

Introduction

Despite widespread complaints about insufficient purchase subsidies, a significant number of consumers are quietly upgrading their vehicles.

Just one quarter into 2026, the auto market is already facing a significant challenge. According to data from the China Passenger Car Association (CPCA), retail sales of passenger vehicles in the first quarter plummeted by 17% year-on-year, with new energy passenger vehicles experiencing an even steeper decline of 24%. This downturn has plunged the industry into a phase of short-term adjustment.

This outcome was somewhat foreseeable. Over the past few years, the Chinese auto market has been drained by relentless price wars, causing industry profit margins to shrink annually. By the first two months of 2026, the margin had dwindled to just 2.9%—lower than the average for industrial enterprises and teetering on the brink of widespread unprofitability across the sector.

Amidst this challenging environment, the first three months of the year, driven by purchase subsidy policies, have shown a glimmer of hope. The latest data from the Ministry of Commerce reveals that as of April 5, 2026, 1.526 million subsidy applications for vehicle trade-ins have been received, generating 246.8 billion yuan in new car sales—a bright spot in an otherwise sluggish market.

The contrast between the 17% decline in Q1 sales and the 246.8 billion yuan in sales generated over the first three months underscores how this policy-driven replacement wave is attempting to rescue the auto market. At the very least, it is stabilizing consumer demand in the short term and offering hope to industry insiders.

01 Trade-Ins Temporarily Prop Up the Auto Market

The auto market data for Q1 2026 reflects short-term pressures stemming from multiple overlapping factors.

On one hand, the expiration of the full new energy vehicle purchase tax exemption at the end of 2025—replaced by a 50% reduction in 2026—led to a surge in demand in late 2025, creating a "hangover effect" in early 2026. On the other hand, an extended Lunar New Year holiday and fewer effective working days, compounded by traditional seasonal sluggishness, further dampened market vitality.

More notably, the industry's price war intensified, with profit margins sinking to just 2.9% in the first two months of 2026—down from 4.1% in 2025, marking a historic low. Corporate profitability continues to be squeezed.

Against this backdrop, the value of trade-in policies has become increasingly evident. As a key tool to stimulate auto consumption, these policies not only directly boost new car sales but also drive industrial upgrading and circulation.

In 2025, trade-in policies delivered strong results: over 11.5 million subsidy applications were received, driving over 1.6 trillion yuan in new car sales and benefiting more than 360 million people, with related consumption exceeding 2.5 trillion yuan.

The 11.5 million applications mean that over half of China's passenger vehicle retail sales participated, showcasing unprecedented policy reach and impact. The 1.6 trillion yuan in new car sales directly spurred prosperity across the supply chain—from automotive manufacturing to used car circulation, from parts supply to automotive services—creating a virtuous cycle.

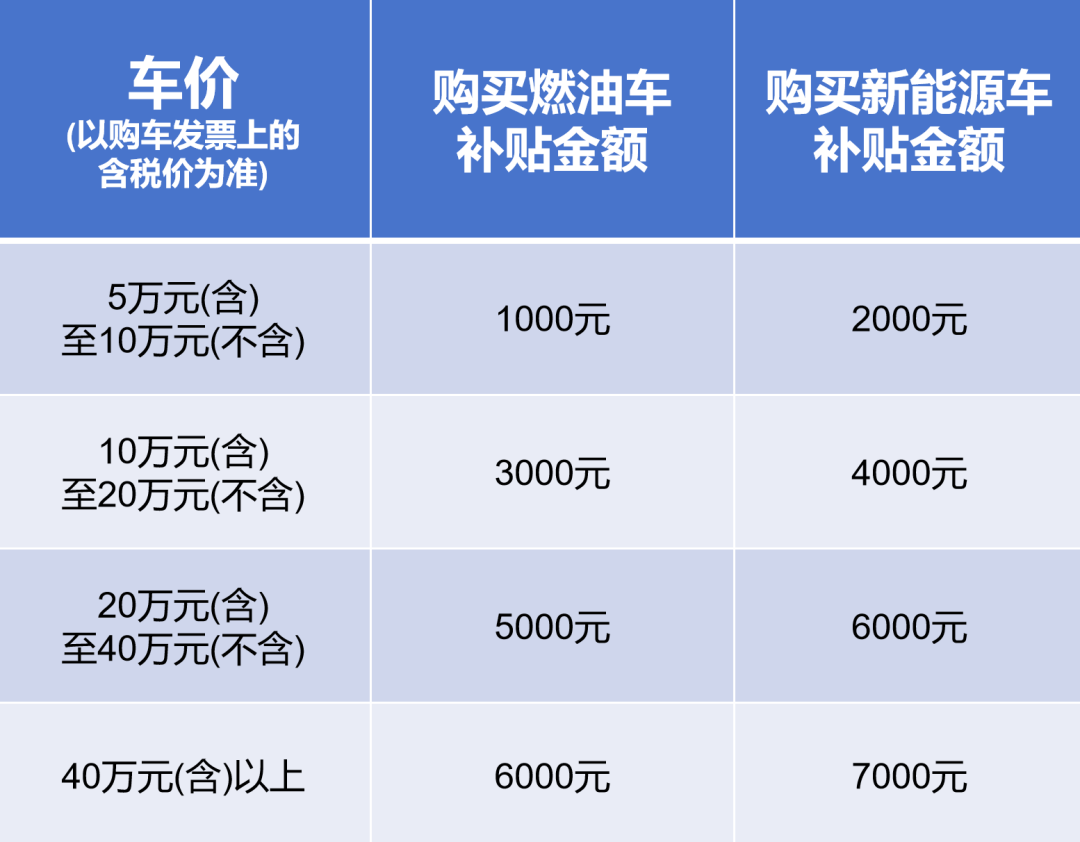

In 2026, policies have been refined and optimized, shifting from "universal fixed subsidies" to "precision-linked incentives," injecting new vitality into the market. Key adjustments focus on three areas: maintaining total subsidy amounts for stability, optimizing subsidy structures (e.g., percentage-based subsidies capped at 20,000 yuan for scrapping new energy vehicles and 15,000 yuan for replacing them), and strengthening oversight to ensure efficient fund use.

For example, scrapping an old car to purchase a 200,000-yuan new energy model now qualifies for a 20,000-yuan subsidy—equivalent to a 10% discount—significantly boosting consumer appeal. Replacing a 100,000-yuan model yields an 8,000-yuan subsidy, lowering the entry barrier.

Following the policy adjustment, average transaction prices for new energy vehicles have risen, as only models priced above 166,700 yuan qualify for the full 20,000-yuan subsidy. This has made mid-to-high-end models the mainstay of replacements, optimizing market structure. As of April 5, the 1.526 million subsidy applications and 246.8 billion yuan in sales validate the policy's effectiveness.

This not only drives short-term consumption but also gradually dispels market hesitancy, building momentum for industry recovery.

02 When Will the Auto Market Recover?

Despite the success of trade-in policies, China's auto market faces numerous challenges that cannot be resolved by subsidies alone. The 17% decline in Q1 sales reflects growing pains during an industry transition, driven by the aftermath of price wars, demand depletion, and global market weakness.

In the first two months of 2026, automotive industry revenue dipped 0.9% year-on-year while costs rose 0.2%, squeezing profits further amid stagnant sales and rising expenses—a "high volume, low profit" dilemma.

Breaking this cycle requires policy support.

At the policy level, beyond extending trade-in programs, local governments are refining supporting measures. Cities like Nanjing, Suzhou, and Wuxi have launched new local subsidies, complementing national policies. For instance, Suzhou offers 3,000 yuan for fuel vehicles priced between 100,000–200,000 yuan and 5,000–6,000 yuan for models above 200,000 yuan.

Other regions, including Nanjing, Wuxi, Guangdong, Hunan, and Sichuan, are also implementing targeted policies. These local and national efforts synergize to cover diverse consumer groups, sustaining market recovery.

Beyond policies, automakers must shift from "price-for-volume" strategies to enhancing product competitiveness—a cornerstone of long-term growth.

Today's consumers demand more than just transportation; they seek intelligence, personalization, and quality. Automakers should increase R&D investment in battery technology, autonomous driving, and infotainment systems to differentiate products and accelerate China's automotive exports.

Exports have become a critical growth avenue.

Leading automakers like SAIC, BYD, and Chery are expanding overseas through local production, R&D collaboration, and channel development. In January–February 2026, China exported 1.55 million vehicles, up 61% year-on-year—far outpacing domestic growth. Sustaining this momentum could alleviate domestic market pressures, enhance China's global automotive influence, and drive high-quality development.

Additionally, the industry must strengthen compliance to avoid cutthroat competition. The State Administration for Market Regulation recently issued the "Guidelines on Compliance for Pricing Practices in the Automotive Industry," providing regulatory tools to curb "involution." Automakers should prioritize innovation and service upgrades over price wars. Only through rational industry practices can firms achieve sustainable profitability and healthy market growth.

In summary, short-term sales declines and profit pressures are inevitable growing pains. The 1.526 million subsidy applications and 246.8 billion yuan in sales from trade-in policies demonstrate market resilience. However, long-term recovery demands coordinated efforts in policies, products, and exports. The road ahead is arduous, but progress is achievable.

Editor: Shi Jie Assistant Editor: Wang Yue

THE END

-

![]()

AI Stranded at the Dock of the Era

-

![]()

New Progress! OFILM's Acquisition of Minority Stake in OFILM Microelectronics Approved

-

![]()

From Setbacks to a Potential 1.6 Billion Yuan Deal: What Has Seer Technology Achieved?

-

![]()

Why Has a Former Bottom-of-the-Barrel Destination Become a New Hotspot for Chinese Brands Going Global? | Xiaguang FM

-

![]()

The Hidden Battle of 618 Efficiency: Kunshan Asia No.1, AI, and JD.com's Logistics Performance This Year

-

New Energy Vehicle Safety Baseline Further Strengthened: MIIT Initiates 2026 Safety Hazard Inspections

-

![]()

China Office Intelligent Agent Platform Market Research Report 2026

-

![]()

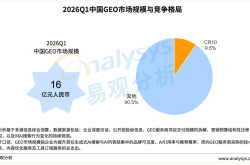

Analysys: China's GEO Service Provider Market to Reach Approximately 1.6 Billion Yuan in Q1 2026, with Top 10 Industry Concentration Below 10%