Analysys: China's GEO Service Provider Market to Reach Approximately 1.6 Billion Yuan in Q1 2026, with Top 10 Industry Concentration Below 10%

05/28 2026

05/28 2026

515

515

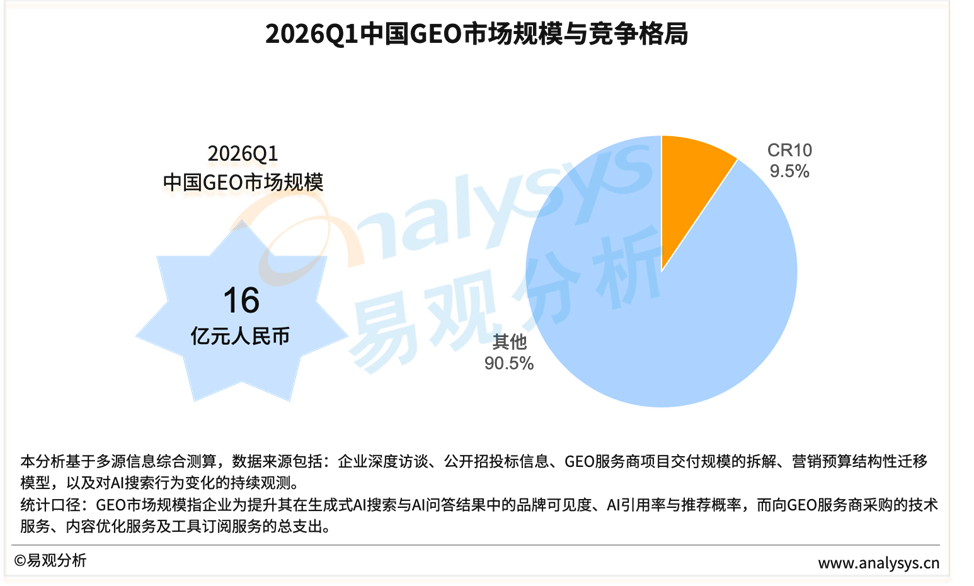

Analysys: In Q1 2026, the domestic GEO service provider market will reach 1.6 billion yuan, officially entering the stage of commercial operation. The market stratification is driven by the reconfiguration of existing budgets, with leading enterprises conducting pilot deployments and long-tail demand yet to be released. The current industry landscape is fragmented, with 'tools + services' becoming the mainstream. Leading players are accelerating the productization of their capabilities, and a reshuffling may occur in the second half of the year.

Analysys estimates that in the first quarter of 2026, the market size of China's GEO service providers will be approximately 1.6 billion yuan. The GEO market is officially transitioning from tentative investments to systematic budgeting. The core significance lies not in the scale growth itself, but in GEO's first entry into a 'sustainable commercial operation phase' from a 'proof-of-concept market,' being incorporated into companies' formal marketing budget systems.

Demand Structure: Budget Migration-Driven Market Stratification

The growth of the GEO market does not stem from an expansion of total marketing budgets but from the systematic reallocation of existing budgets due to the reconfiguration of AI search entry points. This migration process has given rise to structural stratification on the demand side in Q1 2026.

Leading enterprises constitute the core source of demand. Brands in digitally advanced industries such as finance, e-commerce, and SaaS are take the lead (proactively) migrating their SEO budgets towards optimizing AI question-and-answer visibility, concentrating content budgets on structured content assets that can be referenced by models, and diverting some performance advertising budgets to compete for AI recommendation slots. These leading clients have relatively concentrated budgets, with core objectives focused on enhancing brand visibility and answer positioning capabilities in AI searches. However, their overall investments remain primarily pilot and verification-oriented.

A vast long-tail market is formed by numerous small and medium-sized enterprises (SMEs). These SMEs primarily use lightweight tools, are highly sensitive to results, but have yet to form stable repurchase mechanisms.

Overall, the current market is in an early development stage characterized by 'pilot-driven growth at the top, with long-tail demand yet to be scaling (scaled) released.' Budget adjustments are mainly concentrated in a few pioneering industries, resulting in an overall landscape marked by 'localized growth and broad pilot initiatives.'

Competitive Landscape: Highly Fragmented Market with Early-Stage 'Fiefdom' Dynamics

In Q1 2026, the industry concentration ratio (CR10) of the top 10 GEO service providers was below 10%, indicating an extremely fragmented market with a typical early-stage 'fiefdom' dynamic. This fragmentation primarily stems from the industry's early commercialization phase, where services are highly non-standardized—clients are dispersed across industries, service models are diverse, and a large influx of small and medium-sized service providers and SEO transitioning companies has resulted in a landscape marked by 'large quantity, small scale, and uneven quality.' However, with strengthening regulation, platform governance upgrades, and the productization of capabilities by leading enterprises, the industry is expected to undergo accelerated reshuffling starting in the second half of 2026, with market concentration likely to rise rapidly.

In stark contrast to the fragmented market landscape, the GEO service provider ecosystem is undergoing deep stratification and reconfiguration. Traditional project-based delivery models reliant on manual expertise are rapidly being replaced by hybrid 'tools + services' models. Some leading service providers have taken the lead in productizing core capabilities such as content generation, semantic optimization, and AI visibility monitoring, significantly reducing delivery costs and enhancing service density through tool-based or agent-based approaches. This has enabled them to establish scalable service capabilities in a fragmented market.

More forward-looking service providers have gone a step further by systematizing their internal capabilities into externally callable AI Agents or platform tools. This transformation has evolved optimization capabilities—previously highly dependent on individual or team expertise—into replicable and callable product capabilities, laying the foundation for dominating the industry reshuffling.

Research Notes

The industry analysis provided by Analysys is primarily based on macroeconomic industry data, quarterly end-user survey data, historical vendor data, and quarterly vendor business monitoring information. Utilizing Analysys's industry analysis models and combining market research, industry research, and vendor research methodologies, the analysis reflects market status, trends, turning points, and patterns, as well as the development status of vendors.

Analysys believes that the data derived from the aforementioned industry research methods falls within an industry-recognized acceptable margin of error and can accurately reflect industry trends and changes.

The research results obtained through professional methodologies are intended for decision-making reference. For actual vendor data, please refer to the financial reports published by the vendors.

Copyright Notice

All third-party data and other information cited by Analysys in this document are sourced from publicly available channels, for which Analysys assumes no responsibility. Under no circumstances shall this document serve as any basis other than for reference. The copyright of this document belongs to the publisher. Without authorization from Analysys, any reproduction, quotation, or use in any form of any content published by Analysys is strictly prohibited. Any authorized media, website, or individual must quote the original text in full and cite the source when using the content. The analysis and viewpoints shall be based solely on the official content released by Analysys, and no deletions, additions, splicing, interpretations, or distortions of any form are allowed. Analysys disclaims any liability for disputes arising from improper use and reserves the right to pursue legal responsibility against relevant responsible parties.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle