How Did the Chip Industry ‘Latecomer’ Take the Lead in Listing? AXERA's Qiu Xiaoxin: Boundaries Are Key to Competitiveness

04/13 2026

04/13 2026

605

605

Author | Zhang Lianyi

How quickly can a chip company, founded just six years ago, achieve growth in the fiercely competitive field of intelligent driving?

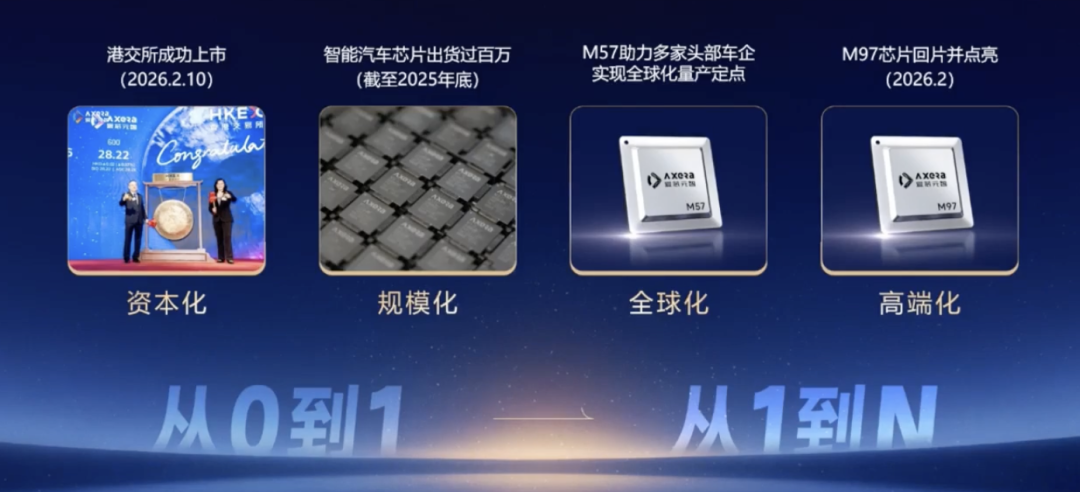

AXERA's interim response: Its first intelligent driving chip entered mass production for vehicle installation in June 2023. By the end of last year, the number of chips installed in real-world vehicles had surpassed 1 million. In February of this year, the company celebrated its listing on the Hong Kong Stock Exchange.

From a timeline perspective, AXERA is an undisputed ‘latecomer.’ Yet, judging by its results, it has achieved an acceleration rarely seen among industry newcomers.

On April 11, at the High-Level Forum on the Development of Intelligent Electric Vehicles (2026), Qiu Xiaoxin, founder and chairwoman of AXERA, described the company’s current status in the automotive sector as both a ‘latecomer’ and possessing ‘absolute new qualitative competitiveness.’ The former acknowledges reality, while the latter signals ambition. In her view, after completing the leap from 0 to 1, the next step is to scale from 1 to N, achieving broader and more scalable deployment.

Why can a pure chip supplier break through so quickly in the highly competitive intelligent driving sector? The answer lies in technological accumulation and a clear strategic positioning.

‘AXERA operates strictly as a Tier 2 chip supplier,’ Qiu Xiaoxin stated in an interview. ‘By clearly defining our boundaries, cooperation with upstream and downstream partners becomes straightforward because we respect and do not overstep their roles.’

In her view, boundaries are synonymous with competitiveness.

01

Four Chips: The Acceleration of a Latecomer

Although a latecomer in the intelligent driving field, AXERA’s deployment speed is remarkable.

From the first chip’s vehicle installation to shipping 1 million units, it took less than two years. How was this speed achieved? Qiu Xiaoxin attributes it to ‘cross-domain technological reuse’ and ‘precise product definition.’

Qiu Xiaoxin has repeatedly emphasized that AXERA is not merely a ‘pure in-vehicle chip company’ but rather a platform-based edge computing chip company. The company’s core technological IP had already undergone market validation in other product lines before entering the automotive sector.

‘When we use the same core technology to build in-vehicle products, the IP is already mature, eliminating the need for large-scale trial and error,’ she explained in the interview. ‘Latecomers have advantages. We understand where the industry’s demand has converged, allowing us to define products very precisely.’

In simpler terms: After L2 intelligent driving becomes a ‘regulation-driven standard component,’ market demand becomes crystal clear—achieving ultimate cost efficiency while meeting regulatory requirements. The core reason AXERA’s first in-vehicle chip, the M55H, quickly gained traction after its 2023 vehicle installation was not its groundbreaking technology but its precise market alignment.

‘When L2 becomes a mandatory standard component, automakers become highly focused on performance and cost, especially cost requirements under regulatory compliance. We happened to create a product that meets automakers' requirements.’

The M55H is just the starting point. Examining AXERA’s strategic deployment in the intelligent driving field reveals a clear, step-by-step approach: four chips, progressively covering the market from low to high.

First chip: M55H, the stepping stone. Mass-produced for vehicle installation in June 2023, it secured entry into automakers' supply chains.

Second chip: M57, a tool for cost reduction and efficiency improvement, aiming to democratize intelligent driving. Launched in 2024 for the L2 market, it operates at less than 3 watts of power consumption under a 125-degree junction temperature, integrates an MCU to maximize BOM cost optimization, and supports multiple solutions ranging from 8-megapixel front-view integrated machines to small domain controllers combining parking and driving functions.

‘When we provided the data to Global Tier 1 suppliers, they didn’t believe it and insisted on testing the boards themselves. After testing, they were convinced.’ Another strategic value of this chip is its suitability for ‘overseas expansion’—it supports Europe’s stringent DMS/OMS standards and has accompanied Chinese automakers' overseas models, even securing design wins from global Tier 1 suppliers for local models.

Third chip: M76H, targeting mid-to-high-level intelligent driving markets, focusing on domain controller solutions combining parking and driving functions.

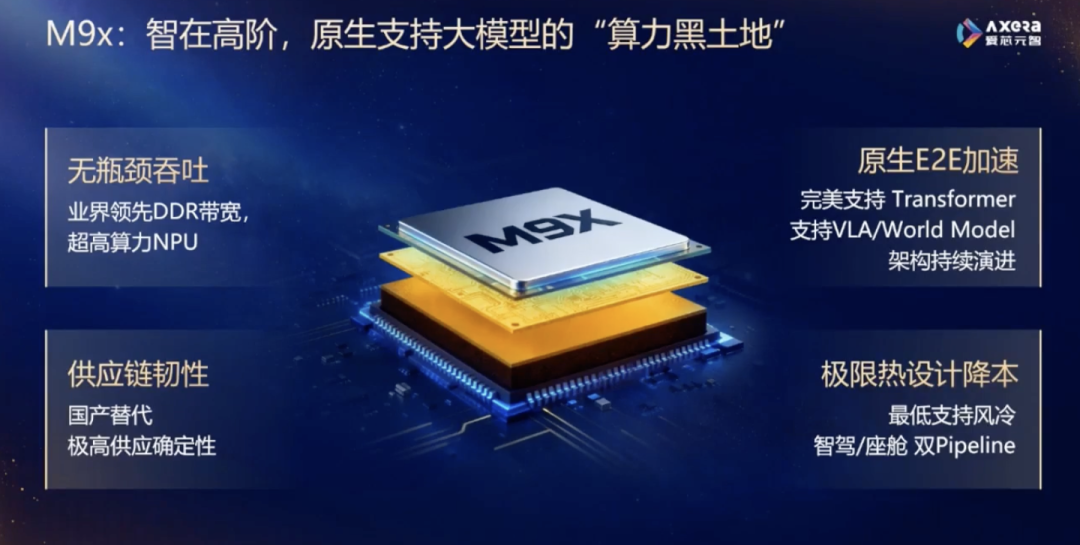

Fourth chip: M9X series, aiming for the high end. A typical representative is the M97, planned in the second half of 2024 and taped out in January this year. This chip aims to benchmark against the industry’s most advanced intelligent driving chips, with mass production scheduled for the end of this year and ramping up next year.

Its core breakthrough lies in solving the ‘memory wall’ problem—DDR bandwidth is increased to over 460 GB/s, supporting native Transformers, VLA, and world models. Qiu Xiaoxin’s expectation for the M97 is to enable high-level intelligent driving to penetrate the 150,000 to 300,000 yuan vehicle segment, down from models priced above 300,000 yuan.

Qiu Xiaoxin noted that AXERA typically launches new products every two years to keep pace with algorithmic upgrades.

02

Dumbbell: The True Shape of the Intelligent Driving Market

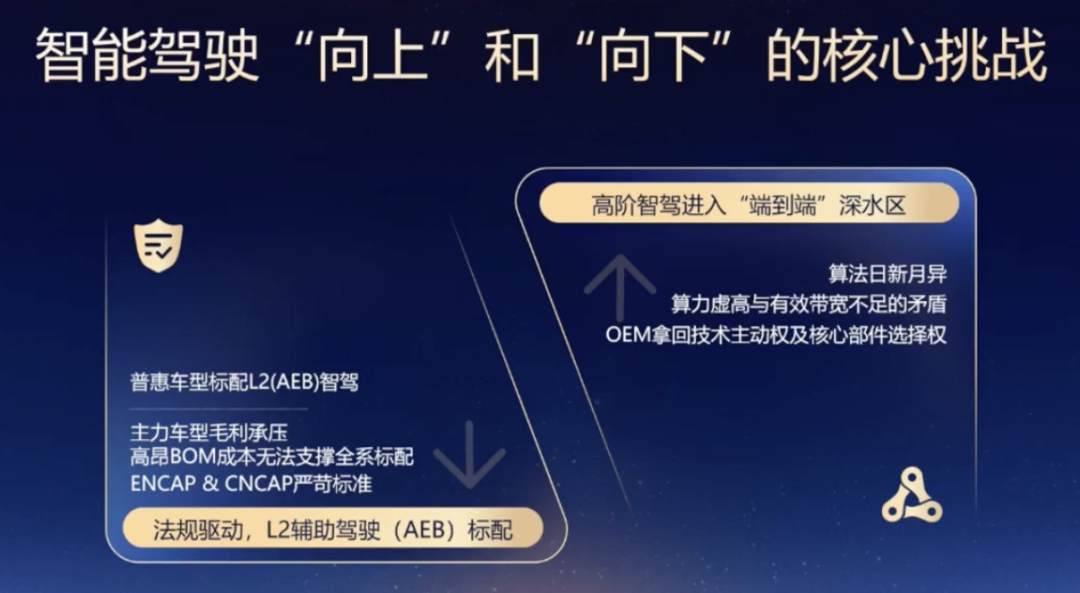

Through her in-depth deployment in the intelligent driving vehicle sector, Qiu Xiaoxin has gained further insights into the industry: The intelligent driving market resembles a dumbbell, not a pyramid.

At one end of the dumbbell is the regulation-driven L2 standard market, characterized by extreme cost sensitivity.

This market’s features: Vehicle models have extremely low gross margins or even operate at a loss, yet intelligence is a must-have. Qiu Xiaoxin’s exact words: ‘Mainstream models face tremendous gross margin pressure but still need to achieve intelligence.’

The M57 is tailored for this market. In addition to its previously mentioned low power consumption and integrated MCU, it supports multiple solution formats—not limited to front-view integrated machines but also capable of small domain controllers combining parking and driving functions, as well as covering European strong-standard products like DMS/OMS. Qiu Xiaoxin said the goal is to achieve ‘unified intelligence across fuel and electric vehicles,’ providing consistent computational support across powertrain platforms to avoid redundant development waste.

A direct result of this ultimate efficiency: Chinese automakers are starting to take domestic chips overseas with them.

‘Domestic chips' market share will rapidly climb to 80-90% within the next two to three years, driven by regulations,’ Qiu Xiaoxin predicted. Her rationale is that after several years of validation, domestic chips now adequately meet Europe’s stringent regulatory requirements, and the pace of import substitution in new vehicle adoption is accelerating.

At the other end of the dumbbell is the computational anxiety in high-level intelligent driving.

This end follows entirely different logic. Algorithm iteration is too fast. From rule-driven to end-to-end, then to VLA large models, the underlying foundational models are still evolving. Qiu Xiaoxin admitted that whether high-level intelligent driving chips can truly meet the needs of algorithm partners and automakers ‘actually remains a question mark.’

She stated that the current ‘memory wall’ pain point faced by high-computational-power platforms means that simply stacking computational power without matching high bandwidth leads to idle capacity. The M97’s design approach directly increases DDR bandwidth to prevent computational power from being bottlenecked by bandwidth.

‘We hope to enable high-level intelligent driving in the 150,000 to 300,000 yuan vehicle segment at a lower cost and better experience,’ she said. Platforms like Thor-U have excessively high domain controller costs, typically appearing only in models priced above 300,000 yuan. AXERA aims to use a more optimized cost structure to truly democratize high-level intelligent driving.

Facing the industry’s heated discussion on the ‘cabin-driving integration’ trend, Qiu Xiaoxin offered a calm judgment.

She did not deny the value of this technological direction but pointed out a key obstacle at the implementation level: It lies not in the chips themselves but in automakers' organizational structures.

‘The cabin team and the intelligent driving team are two separate teams. When developing on the same chip, resource competition becomes inevitable. For example, how should bandwidth be allocated? Which has higher priority for NPU cores? The safety levels of these two applications also differ,’ she said. ‘Implementation complexity is very high, so go-to-market time will be very long.’

Her view is that a more pragmatic path at this stage is to iterate intelligent driving and cabin chips separately but with the same board design, eliminating redundant peripheral components wherever possible. ‘This approach significantly shortens go-to-market time and may be more beneficial for automakers.’

Regarding the high-end market, her judgment is clearer: ‘High-end chips should remain separate at least for now. This allows cabin and intelligent driving chips to iterate independently and quickly. Binding them together slows down iteration speed. It’s the same logic as separating AP and baseband chips in high-end mobile phones.’

03

Boundaries Equal Competitiveness: Returning Autonomy to OEMs

As a chip supplier, the topic of ‘automakers' trend of self-developing chips’ seems unavoidable.

Qiu Xiaoxin’s response avoids taking sides and instead breaks down the issue from a commercial logic perspective.

‘Chips require scale and volume. If automakers developing their own chips have sufficient scale to justify the return on investment, they will proceed. But if not, they will still use third-party suppliers,’ she said. ‘Even companies developing their own chips use third-party products. It’s not black and white.’

She cited a counterexample to illustrate the value of self-development: Amazon developing cloud chips, Google developing TPUs, and Microsoft developing chips make sense because the volumes are large enough. However, in the automotive industry, whether each automaker's volume can justify the R&D cost of a chip is questionable.

In her view, there are currently three models in the intelligent driving chip field: First, automakers self-develop chips, handling everything from chips to algorithms, hardware, and final mass production and delivery themselves. Second, suppliers offer integrated hardware and software solutions, handling everything from chips to algorithms and partial mass production through third-party suppliers. Third, a more open and respectful business model that adheres to industry specialization.

AXERA clearly follows the third model, with Qiu Xiaoxin drawing a very clear boundary: Tier 2 chip supplier.

This positioning may not sound glamorous, but amid increasingly intense supply chain competition, it has become a competitive advantage. ‘After clearly defining our boundaries, cooperation with upstream and downstream partners becomes very simple because we do not overstep their boundaries.’

She used a vivid expression: ‘Return autonomy to OEMs and leave integration space to Tier 1 suppliers.’

For Tier 1 suppliers, a chip supplier with clear boundaries means their value space will not be eroded. This is why AXERA, as a latecomer, secured design wins from multiple leading Tier 1 suppliers and overseas automakers within two years.

Qiu Xiaoxin further explained this logic: The value of independent chip companies lies in their ability to remain neutral, selling chips to different automakers and achieving commercial closure through scale.

In the interview, Qiu Xiaoxin remarked, ‘I feel we’ve been quite lucky.’

This statement sounds modest, but when considered alongside her previous remarks, you realize this ‘luck’ is backed by a clear decision-making logic: Entering during the L2 regulation-driven window, rapidly launching precisely defined products using validated technological foundations, winning trust from ecosystem partners through clear boundaries, deploying four chips to cover both ends of the dumbbell market, ultimately completing the leap from 0 to 1 within two years and successfully going public.

Of course, going public is not the finish line. She said the next step is to go from 1 to N, achieving broader and more scalable deployment.

-END-

-

![]()

AI Stranded at the Dock of the Era

-

![]()

New Progress! OFILM's Acquisition of Minority Stake in OFILM Microelectronics Approved

-

![]()

From Setbacks to a Potential 1.6 Billion Yuan Deal: What Has Seer Technology Achieved?

-

![]()

Why Has a Former Bottom-of-the-Barrel Destination Become a New Hotspot for Chinese Brands Going Global? | Xiaguang FM

-

![]()

The Hidden Battle of 618 Efficiency: Kunshan Asia No.1, AI, and JD.com's Logistics Performance This Year

-

New Energy Vehicle Safety Baseline Further Strengthened: MIIT Initiates 2026 Safety Hazard Inspections

-

![]()

China Office Intelligent Agent Platform Market Research Report 2026

-

![]()

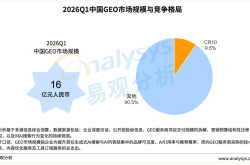

Analysys: China's GEO Service Provider Market to Reach Approximately 1.6 Billion Yuan in Q1 2026, with Top 10 Industry Concentration Below 10%