Will Emerging Car Manufacturers Initiate the 'Ultimate Showdown'?

04/13 2026

04/13 2026

413

413

Profitability Lifeline

After a decade of fierce competition, emerging automotive brands have finally entered a new era.

In 2025, several new players in the automotive industry successively announced their achievement of a single-quarter or full-year net profit turnaround, a milestone widely recognized within the industry as a critical juncture for profitability and even survival. Recently, with the release of the 2025 financial reports from various emerging automotive brands, the answers have become clear.

Leapmotor reported a net profit attributable to shareholders of RMB 540 million in 2025, marking its first full-year profit since inception. Xiaomi Auto achieved its first full-year operating profit of RMB 900 million. Li Auto's net profit plummeted by 85%, from RMB 8.045 billion in 2024 to RMB 1.139 billion in 2025, but it still outperformed other brands. XPENG Motors achieved profitability for the first time in the fourth quarter, with a net profit of RMB 380 million, while its full-year loss narrowed to RMB 1.14 billion, falling short of break-even. NIO also achieved its first single-quarter profit in the fourth quarter, but its net loss attributable to shareholders for 2025 remained a staggering RMB 14.94 billion. Seres has yet to release its latest financial report, but its Q1-Q3 2025 financial report showed a net profit of RMB 5.312 billion, up 31.56% year-on-year.

The emerging forces, who were still being debated as to 'who would survive' just two or three years ago, have now, one after another, crossed the profitability threshold, signaling the end of the 'era of burning money.' After more than a decade of rapid development, emerging automotive brands have undergone several rounds of elimination, with only a select few surviving.

As these emerging automotive brands reach the milestone of profitability turnarounds, the ultimate showdown has only just begun.

Profitability Inflection Point

For the emerging automotive brands as a whole, the 2025 financial reports serve as a positive signal, with several mainstream brands now demonstrating 'hematopoietic capacity,' or the ability to generate profits.

Despite a significant decline in profitability in 2025, Li Auto, as the earliest emerging automotive brand to achieve full-year profitability, still led in profits. Its full-year revenue reached RMB 112.3 billion, surpassing RMB 100 billion for the third consecutive year, with a net profit of RMB 1.139 billion. In 2025, Li Auto delivered 406,300 vehicles, experiencing its first annual sales decline.

Following closely was Xiaomi Auto, whose revenue exceeded RMB 100 billion for the first time in 2025, reaching RMB 106.1 billion, and whose annual operating income turned positive for the first time, at RMB 900 million. In 2025, Xiaomi delivered over 410,000 new vehicles, more than tripling year-on-year. The average selling price rose from RMB 234,500 to RMB 251,200, driven by high-end models such as the SU7 Ultra and YU7.

Leapmotor topped the emerging automotive rankings in 2025 with 596,600 deliveries, up 103.1% year-on-year. Its full-year revenue reached RMB 64.73 billion, up 101.3% year-on-year, with a net profit of RMB 540 million, achieving its first full-year profit. Leveraging its comprehensive breakthroughs in products and technologies in 2025, as well as the continuous improvement of its full-industry-chain layout, Zhu Jiangming, Chairman and CEO of Leapmotor, stated, 'In 2026, Leapmotor will aim for a new target of one million sales.'

Although NIO and XPENG Motors have not yet achieved full-year profitability, both saw turnarounds in the fourth quarter. NIO achieved an operating profit of RMB 1.25 billion in the fourth quarter, while XPENG Motors achieved a net profit of RMB 380 million, marking their first quarterly profits.

Notably, XPENG Motors' profitability was not only derived from vehicle revenue but also from a significant component: technology R&D services for Volkswagen.

Financial reports showed that XPENG Motors' service and other revenue reached RMB 3.18 billion in the fourth quarter, surging 122% year-on-year, with a gross margin of 70.8%. A relevant executive from XPENG Motors stated bluntly that XPENG Motors had achieved a 'profitability path vastly different from traditional automakers.'

In terms of automotive gross margin, XPENG Motors currently has a comprehensive gross margin of 18.9%, indicating enhanced profitability. Li Auto's comprehensive gross margin stands at 18.7%. Leapmotor's scale effects are gradually emerging, with a comprehensive gross margin of 14.5%. NIO's gross margin increased to 13.6%. Xiaomi Auto's gross margin reached 24.3%. Seres' comprehensive gross margin for Q1-Q3 2025 climbed to 29.38%.

Compared to Tesla's 17.2% gross margin in 2025, most emerging automotive brands demonstrated superior profitability, with gradually improving cost control and value realization capabilities.

A New Chapter Begins

However, after reaching the profitability inflection point, the challenges in 2026 become even more daunting. According to the strategic plans announced by several emerging automotive brands, 'AI + chips' will become the new 'battleground,' an area requiring even more massive investments.

XPENG Motors' physical AI landscape is expanding comprehensively, starting from intelligent electric vehicles to flying cars, Turing AI chips, VLA autonomous driving models, humanoid robot IRON, Robotaxi, and more. Li Auto is gradually transforming into a 'technology-driven' company, with AI accounting for over 60% of its R&D investment. Its self-developed chip, Mach 100, will enter mass production in Q2 2026. NIO's self-developed chip, 'Shenji' second generation, has successfully taped out, and it has established a Shenji chip subsidiary, raising over RMB 2.2 billion in funding, to develop self-driven intelligent driving chips and layout embodied robots.

Leapmotor defines 2026 as the 'inaugural year of intelligent driving,' planning to launch a nationwide city navigation assist function in Q2 2026. By the end of the year, Leapmotor aims to complete the construction of its intelligent driving base model and advance the R&D of assisted driving solutions based on AI large models. Xiaomi plans to invest RMB 60 billion in AI over the next three years, accelerating its transformation into an AI-empowered ecosystem company encompassing people, vehicles, and homes. Currently, Xiaomi's AI large model capabilities have begun to integrate into its various core businesses.

Zhang Xinghai, Chairman of Seres Group, stated externally that Seres will seize the opportunity of integrating 'artificial intelligence + automobiles' to accelerate the application of AI technologies in vehicle control, intelligent cockpits, autonomous driving, and other scenarios. It will also boldly explore new tracks such as embodied intelligence to provide long-term support for continuous industrial upgrading.

As technology competition intensifies, increased investments will undoubtedly pose greater challenges to corporate operations and profits. In 2025, Li Auto's R&D investment reached RMB 11.3 billion, a record high, with AI-related investments accounting for 50%. Li Auto will continue this investment strategy in 2026. XPENG Motors invested RMB 9.5 billion in R&D in 2025, with RMB 4.5 billion in AI-related investments. In 2026, it plans to increase its physical AI R&D capabilities to RMB 7 billion, attempting to build long-term competitive moats through technological differentiation.

NIO's R&D expenses showed a gradual quarterly decline in 2025, from RMB 3.18 billion in Q1 to RMB 2.02 billion in Q4. Qu Yu, CFO of NIO, stated during the Q4 and full-year 2025 financial results conference call that the company would maintain quarterly R&D investments of RMB 2 billion to RMB 2.5 billion in 2026.

Leapmotor's R&D expenditures in 2025 were RMB 4.29 billion. Regarding 2026, which Leapmotor positions as the breakthrough year for its intelligent driving, a relevant executive stated that 'R&D expenses will see a very significant increase' compared to 2025.

Overall, several mainstream emerging automotive brands are now entering a new phase where scale and profitability are equally important, and technology and efficiency determine success. Companies with full-stack self-research capabilities, precise positioning, and efficient operations will take the initiative in industry reshuffling.

However, while laying out AI and focusing on autonomous driving hold immense potential for future development, they will clearly not contribute significantly to revenue and profitability in the short term. The profitability 'lifeline' for emerging automotive brands remains critical. Facing new competitive scenarios such as profitability, gross margin, AI technology, and ecological synergy, the ultimate showdown for emerging automotive brands has already entered a 'hell mode.'

-

![]()

AI Stranded at the Dock of the Era

-

![]()

New Progress! OFILM's Acquisition of Minority Stake in OFILM Microelectronics Approved

-

![]()

From Setbacks to a Potential 1.6 Billion Yuan Deal: What Has Seer Technology Achieved?

-

![]()

Why Has a Former Bottom-of-the-Barrel Destination Become a New Hotspot for Chinese Brands Going Global? | Xiaguang FM

-

![]()

The Hidden Battle of 618 Efficiency: Kunshan Asia No.1, AI, and JD.com's Logistics Performance This Year

-

New Energy Vehicle Safety Baseline Further Strengthened: MIIT Initiates 2026 Safety Hazard Inspections

-

![]()

China Office Intelligent Agent Platform Market Research Report 2026

-

![]()

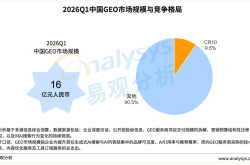

Analysys: China's GEO Service Provider Market to Reach Approximately 1.6 Billion Yuan in Q1 2026, with Top 10 Industry Concentration Below 10%