Stellantis Investor Day 2026 - A Comprehensive Analysis of the FaSTLAne 2030 Strategic Vision

06/08 2026

06/08 2026

573

573

In 2021, Stellantis was born with the ambition to reshape the global automotive industry. Formed through the merger of Fiat Chrysler and Peugeot Citroën, this automotive giant boasts 14 brands, 300,000 employees, and nearly 8 million annual vehicle sales. Led by legendary CEO Carlos Tavares, Stellantis bet big on the electrification wave, planning to invest tens of billions of euros to lead the transition to a pure electric era.

However, just a few years later, reality delivered a starkly different verdict. Consumers did not abandon internal combustion engine vehicles as quickly as expected, electric vehicle demand growth slowed, North American inventories spiraled out of control, and European production capacity sat idle. By 2025, Stellantis recorded its first full-year loss since inception, with a staggering net loss of €22.3 billion, leading to Carlos Tavares's departure.

Amid this major setback in its strategic gamble, the new management team convened its first Investor Day in 2026. This was not just a communication exercise with the capital markets but also a survival blueprint for Stellantis over the next decade: How would it emerge from crisis? How would it reshape itself amid the dual pressures of electrification, global competition, and the rise of Chinese automakers?

This article, Vehicle, is based on information from seven speeches by different leaders and a two-hour Q&A session during Stellantis Investor Day 2026. It summarizes and analyzes Stellantis's strategic directions under FaSTLAne 2030, covering overall strategy, product technology, global regions (North America, Pan-Europe, South America, Middle East, Asia-Pacific, China, etc.), and financial strategies. We hope this provides insights into global automotive trends, competitive landscapes, and inspiration for the globalization of the Chinese automotive industry.

I. Overall Strategy: Redefining "Multi-Brand, Multi-Regional" from a Liability to an Asset

What Was Said at Investor Day

CEO Filosa began with an industry assessment: The automotive industry is shifting from "globalization" to "multi-regionalization" and then to "regionalization." Europe is accelerating electrification, the U.S. is relaxing CO regulations and renegotiating trade terms, Chinese OEMs are launching full-scale offensives in all major markets except the U.S., cost pressures are structural, electrification timelines vary by region, and the competitive battleground has expanded to software, AI, ADAS, and batteries.

The crux lies in how he interpreted this assessment—he argued that precisely because the world is fragmenting, Stellantis's sprawling multi-regional, multi-brand structure is better suited than any other OEM.

This is the soul of the entire plan. In the previous era, multi-brand and multi-regional operations were Stellantis's original sin (internal friction, redundant investments, bloated decision-making). In this version, they have been rebranded as a competitive moat. The strategy is built on six pillars:

Brand Rationalization: Four global brands (Jeep, Ram, Peugeot, Fiat) + five regional brands (Chrysler, Dodge, Alfa Romeo, Citroën, Opel) + two "exclusive brands" (DS and Lancia) managed by Citroën/Fiat. Approximately 70% of product investments will focus on the four global brands, which will debut all global assets.

Capital Allocation: €60 billion over five years, with 40% allocated to global platforms/powertrains/technologies and 60% to brands and products.

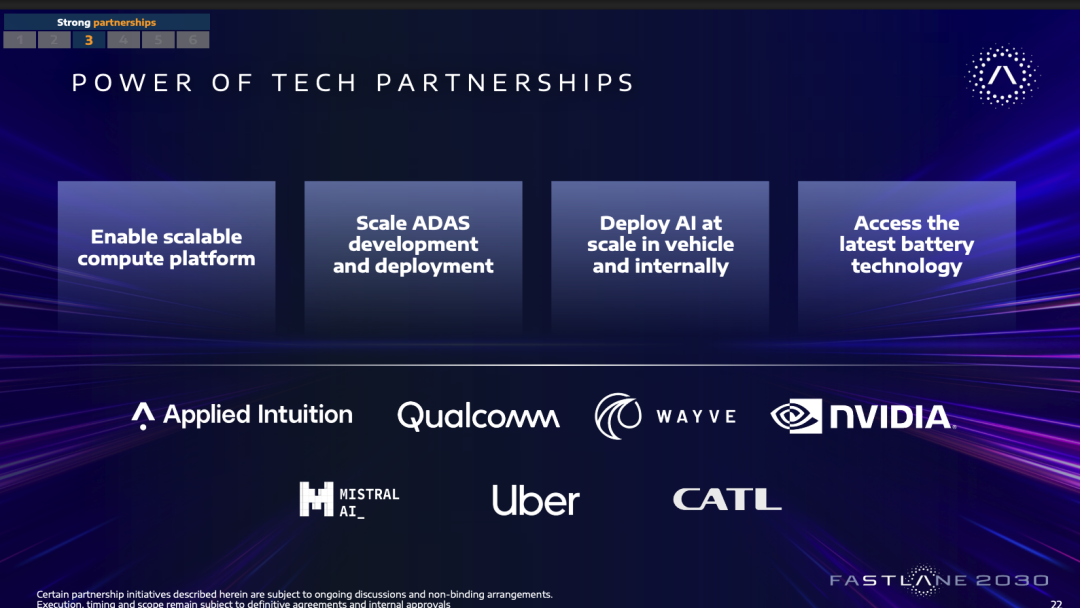

Partnerships: Leapmotor, Dongfeng, Tata, JLR, plus technology partners Qualcomm, Wayve, and Applied Intuition.

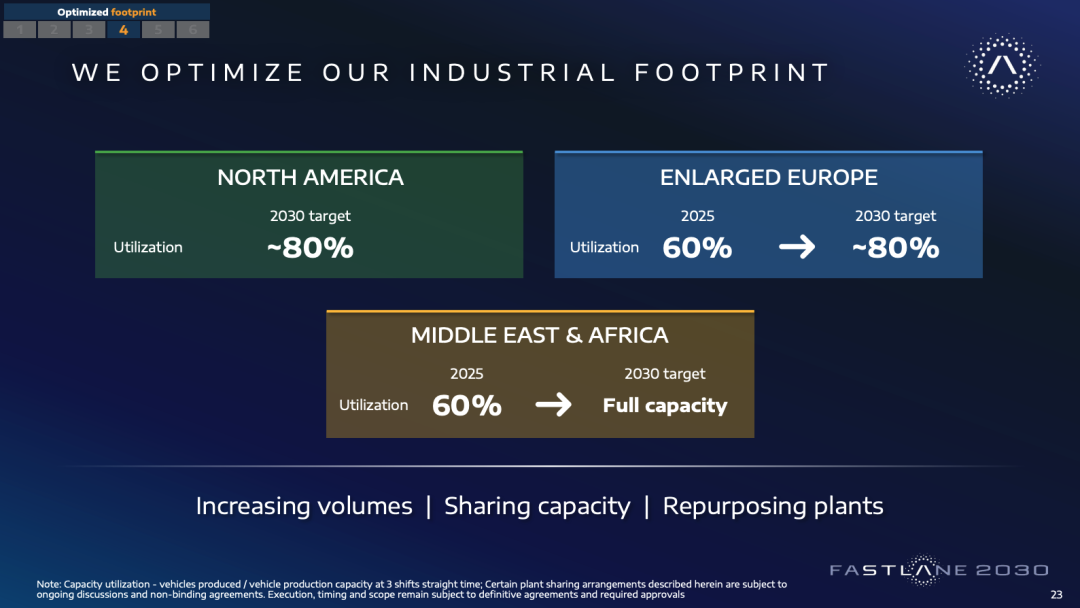

Capacity Optimization: Cut 800,000 units of European capacity without closing any plants, raising utilization rates from 60% to 80%.

Execution Discipline: Achieve €6 billion in cost savings by 2028 through the Value Creation Plan (VCP), achieve top-quartile quality in all segments and regions, and reduce R&D cycles from ~44 months to 24 months.

Regional Empowerment: Each region will manage its own P&L, plan, and execution. A notable move: Maserati was excluded from this discussion and will be addressed separately in Modena in December. Filosa stated, "Its strategy, product rhythm, and value creation are fundamentally different and warrant a dedicated discussion," effectively sidelining the brand long rumored to be up for sale.

Vehicle's Interpretation

I give high marks for the strategic direction. The assessment of "multi-regionalization" is spot-on—current global tariff barriers, diverging regulations, and regionalized supply chains are real trends, and Stellantis is one of the few players with genuine presence in North America, Europe, South America, the Middle East & Africa, and Asia-Pacific. Reframing structural burdens as structural advantages is not only self-consistent but also supported by reality.

Brand rationalization deserves the highest praise in this version. Clarifying the roles of nine brands, demoting DS and Lancia to managed status, and avoiding full-spectrum expansion for each brand—this addresses the biggest source of waste in the previous era. Tim Kuniskis's later remark in the North America section—"Chrysler isn't even competing with its own brands today"—underscores how severe internal friction was.

However, two points warrant caution:

First, "humility" is narrative, not performance. The repeated emphasis on pragmatism and hands-on execution is appropriate after the roll over (setback) of aggressive tactics, but investors won't pay for posture. The plan's real hard commitments are stacked in 2028, as detailed in the financial section later.

Second, Maserati's "postponement" essentially kicks the most thorny issue out of sight. A brand repeatedly rumored to be for sale, positioned as premium yet unable to articulate a clear profit path, being deferred in a plan claiming a "comprehensive reset"—this is not composure but indecision. However, it's possible that recent rumors of BYD acquiring Maserati are true, which is why it wasn't discussed this time.

II. Product & Technology: Bowing to Chinese Rivals While Taking "Buy, Don't Build" to the Extreme

What Was Said at Investor Day

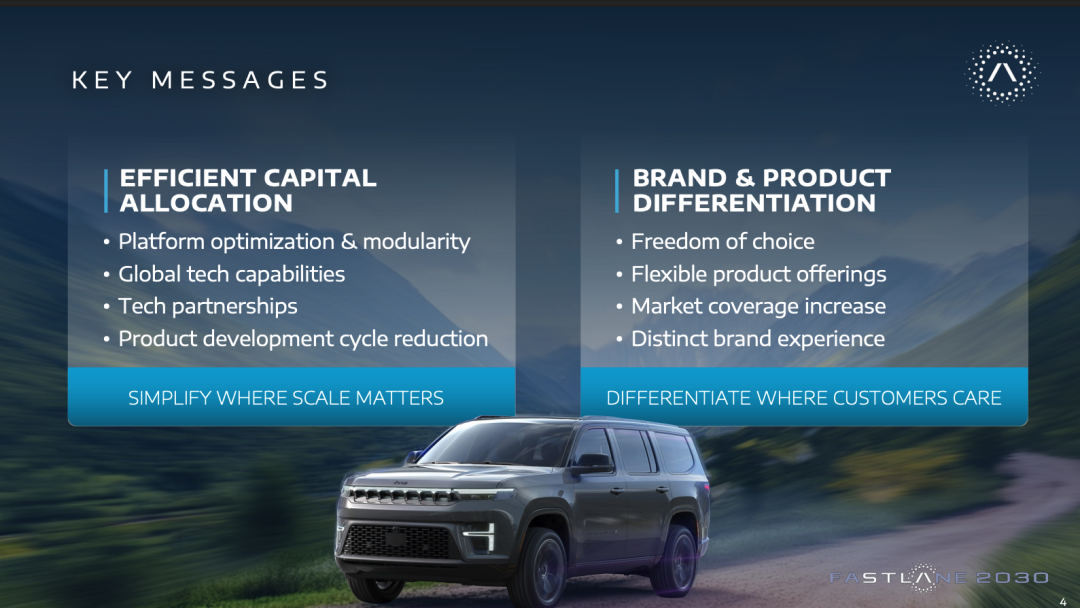

Chief Product Planning Officer Davide Mele and CTO Ned Curic framed this chapter around the theme: "Reduce where scale matters, differentiate where customers care," with technology serving as the lever for both.

In product technology, the focus was on platform architecture and software/electronics.

Platform Side - The Star is STLA One:

A single architecture supporting different powertrain modules via universal interfaces, claiming to avoid the cost burdens of traditional multi-energy architectures. From 2027, it will cover B/C/D segments, target over 2 million units, and support 30+ models by 2035.

Consolidating five existing platforms into one yields ~20% cost savings (from modular design + new battery solutions).

Battery two-step approach: First, adopt LFP to reduce costs and dependency on critical raw materials; then, implement cell-to-body integration to further cut costs, weight, and complexity. 800V architecture.

Mele stated bluntly: This is the path to "close the cost gap with Chinese OEMs selling in Europe and ultimately achieve BEV cost parity."

Software/Electronics Side - Three Key Components Launching in 2027:

STLA Brain: Halve the number of fragmented ECUs, centralize into a high-performance computing unit with up to 6x the computing power and 1,000x the bandwidth, with native OTA capabilities. Deployed in Europe in 2026, the U.S. in 2027, and covering 5 million units by 2035.

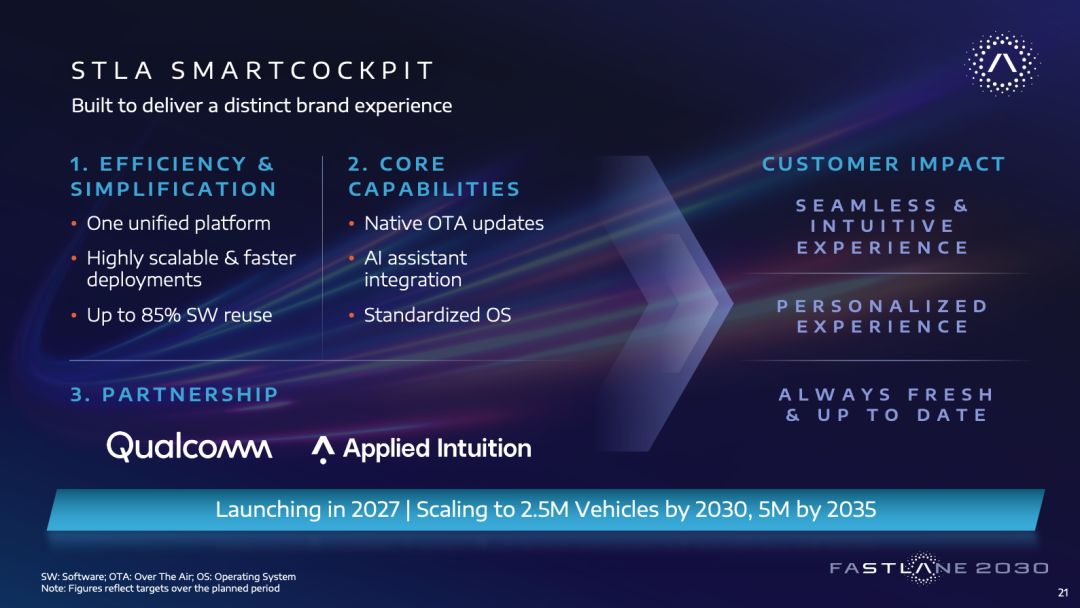

STLA SmartCockpit: Consolidate 12 standalone systems into one cockpit platform across all brands and regions, AI-native, supporting 21 languages, with 85% software reusability.

STLA AutoDrive: Cut costs of existing L2+ systems by 70% while covering 8x more roads; announce a partnership with Qualcomm + Wayve to launch door-to-door, hands-free, supervised autonomous driving in North American products by 2028.

AI in R&D: Accelerate simulations by up to 300x, boost software productivity by 37%, and reduce vehicle development cycles from ~4 years to 24 months.

Curic made a rare admission for a Western automotive CTO: "In terms of speed, the Chinese are truly setting the benchmark, and we're catching up by changing how we build cars."

Vehicle's Interpretation

The most notable aspect of this chapter is its candor. A CTO of a Western century-old giant openly acknowledging that Chinese rivals set the speed benchmark and incorporating "closing the cost gap with China in Europe" into platform KPIs—this would have been unthinkable five years ago.

The technical approach represents the ultimate in "capital-light" strategies. AutoDrive narrows in-house development to vehicle integration and HMI, outsourcing the toughest AI driving models to Wayve and compute to Qualcomm; affordable EVs directly "leverage the Chinese EV ecosystem." The logic is clear: Avoid doubling down on areas where the company lacks expertise and which are capital-intensive. For a company just returning to positive cash flow, this is rational.

However, the risks are substantial:

First, 2027 represents an "all-in" gamble with simultaneous launches. STLA One, STLA Brain, SmartCockpit, and AutoDrive—platform, EE architecture, cockpit, and ADAS—all debut in 2027. Any automaker knows that launching a new platform + new suppliers + new technologies together is a recipe for quality issues. Stellantis has already taken large impairments due to quality/warranty problems. Putting all eggs in the 2027 basket leaves zero room for execution errors, though this may be forced by circumstances.

Second, "buy, don't build" saves capital but erodes capabilities. Building ADAS and affordable EV cores on external partners (Qualcomm, Wayve, Chinese ecosystem) makes short-term financials attractive but cedes long-term technological leadership. When these capabilities become decisive, the gap between "integrators" and "owners" will become apparent. This paradox will resurface in the Europe and Asia-Pacific sections.

Third, the ~20% cost reduction is the linchpin of the European story. Achieving EV-ICE price parity in Europe and selling e-Cars below €15,000 hinges entirely on STLA One delivering these savings. Failure would further erode already thin European profit margins.

III. Regional Strategies: Three Distinct Postures Toward Chinese Rivals

This is the most revealing and strategically telling part of the plan. Reading the five regions together reveals that Stellantis has adopted three entirely different postures toward Chinese rivals: building walls and avoiding direct competition in North America, leveraging partnerships for coexistence in Europe and the Middle East & Africa, and counter-offensives in Asia-Pacific.

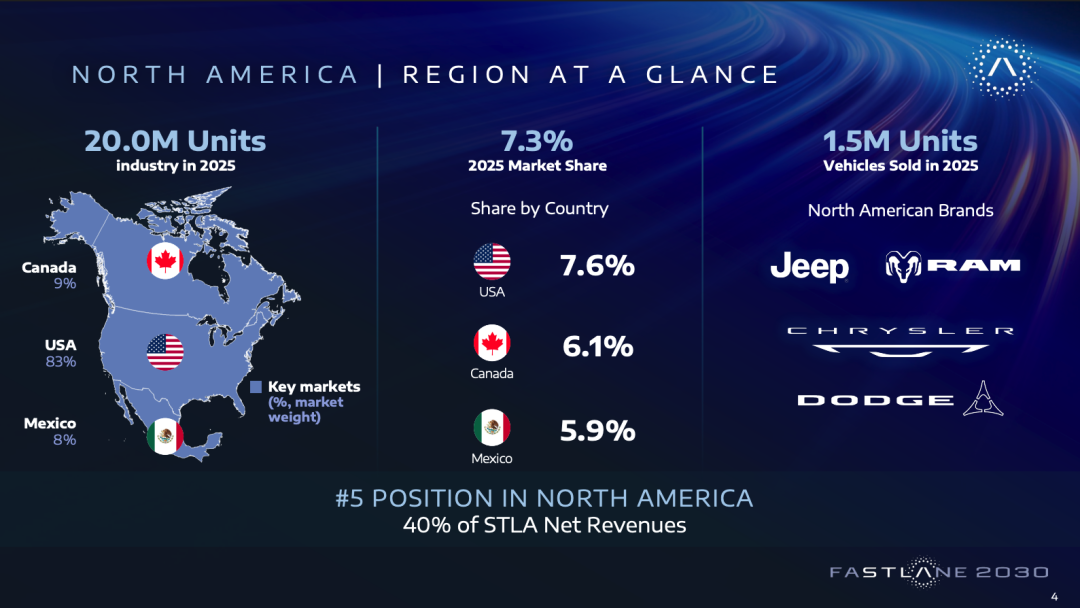

North America: Cash Cow and the Place to 'Build Walls'

North America is led by Filosa herself because it represents the 'biggest opportunity for growth and profitability'—accounting for 40% of today's Group revenue and contributing 60% of future profit growth. Targets: +25% revenue, AOI margin of 8–10%, market coverage expanding from 60% to 90%+.

North America Brand Chief Tim Kuniskis boiled his entire chapter down to one credo: 'Product is king.' 2025 baseline: North American industry at 20M units, U.S. at 16.6M, Stellantis selling 1.5M/1.3M—ranking fifth with 7.6% share. But in segments where it truly competes, its share doubles to third place. The logic: With industry growth stalling by 2030, 'showing up in more segments' alone can drive 35% growth.

Brand-by-brand surgery:

Chrysler adds three $25K–$35K crossovers to fill utility gaps;

Dodge revives the 'Muscle Car Brotherhood' with a V8-powered Charger;

Jeep launches Recon, Cherokee, Grand Cherokee, and '12 for 12' monthly Wrangler variants;

Ram creates the 'highway performance muscle pickup' segment with 5.7L V8 Rumblebee, 392 HEMI, and even a 777-hp SRT variant;

SRT acts as a 'multiplier' across Dodge/Jeep/Ram, delivering 2–3x the net margin of parent brands. The return of the legendary HEMI V8 is a repeated keyword.

Shifting resources to North America is strategically sound—it's a profit pool of real money and a tariff-protected haven from Chinese rivals. Filosa also acknowledged the 'wall-building' logic in Q&A: New North American trade terms make idle capacity 'very attractive' to potential partners.

But Wall Street raised two immediate objections I agree with:

Grabbing 35% volume in a zero-growth market means pure conquest. Barclays' Henning Cosman asked directly: 'Your assumption assumes both volume and price growth—how will competitors retaliate?' That's a fair question. Trying to take share while assuming pricing power remains intact seems optimistic.

Trading down dilutes margins. Reintroducing sub-$30K Chryslers and smaller Rams boosts coverage but drags down the product mix. Even the CFO admitted North American mix will remain 'neutral' through the plan period.

An undercurrent I must highlight: The high-profile return of V8s and HEMIs essentially corrects the previous EV-first misstep. The press conference detail says it all—last year, Dodge sold 125K units with *just one* all-electric, two-door Charger model. Translation: Killing gasoline variants to force EV adoption crippled the brand. Now bringing back ICE options as 'freedom of choice' admits the prior path was too narrow.

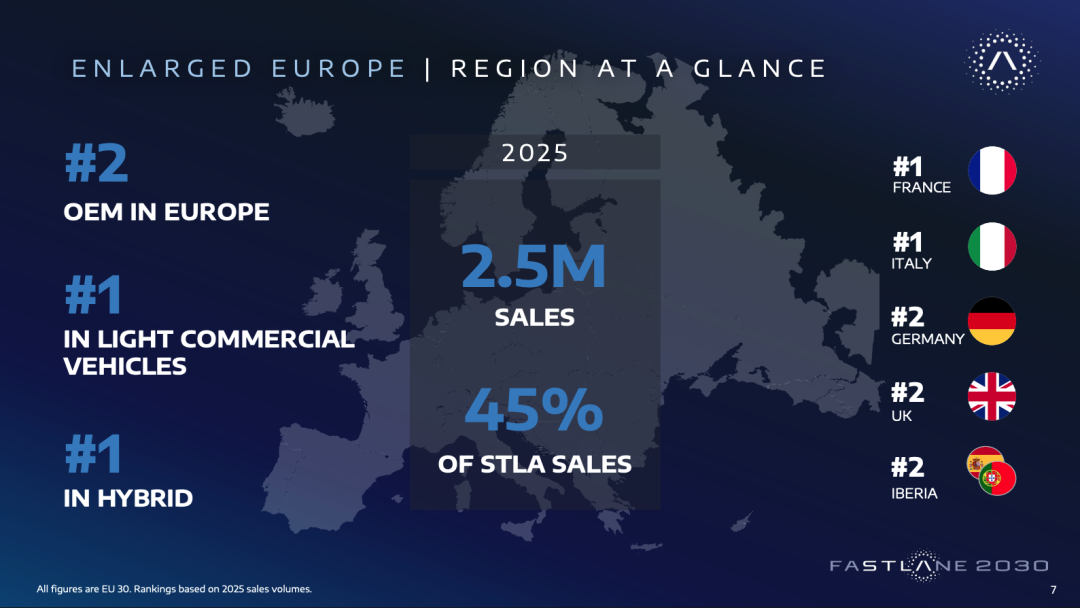

Pan-Europe: Thinnest Profit Margin, Main Battleground for 'Leveraging China'

'Enlarged Europe' was presented by COO Emanuele Cappellano.

At 2.5M units sold in 2025 (nearly half of Group volume), Europe ranks #2 among OEMs, #1 in commercial vehicles and hybrids, led by France and Italy. But target margins are just 3–5% AOI with +15% revenue. Three priorities: Brand differentiation + coverage expansion (+25%), cost reduction (€3B from VCP + STLA One savings), and plant utilization rising from 60% to 80% (cutting 800K capacity without closing factories, repurposing plants like Poissy for parts/circular economy hubs).

Highlight products: e-Car platform launching in 2028 with EVs built in Europe under €15K, achieving BEV-ICE cost parity; Citroën revives the 2CV; Fiat launches Topolino, Grande Panda, Grizzly; Peugeot debuts seven new models (four on STLA One); Opel's electric C-SUV developed jointly with Leapmotor within two years.

Partnerships are explicit in Europe:

Leapmotor International (51% JV) sold 34K units in Europe in 2025, doubling this year, sharing Madrid and Zaragoza capacity;

New 51% European JV with Dongfeng, combining Rennes plant for capacity sharing, even planning to produce Dongfeng's premium Voyah brand in Italy's Ram factory.

Europe is the plan's weakest link by far. At 3–5% margins, Jefferies' Philippe Houchois criticized it on the spot—saying Stellantis operates like a 'two-story business': North America remains a vertically integrated traditional automaker, while Europe keeps shedding assets and vertical integration. 'You save on capital intensity but lose EBIT long-term. What's Stellantis' long-term competitiveness in Europe then? A distribution business?'

That hit hard. In industry terms: When you let Leapmotor build cheap EVs, give Dongfeng's Voyah premium slots, and become increasingly a 'channel + assembly + brand skin,' your European moat shrinks to just brand and distribution—which erode over time.

Even sharper was RBC's Tom Narayan's 'baguette' question: 'You call the five regional brands a 'national team' against China, yet invite Chinese partners inside—what stops them from biting your baguette?' Filosa replied: These JVs are 'distribution + sourcing + capacity sharing' with Stellantis holding 51% and distribution rights, co-selecting products to avoid cannibalization.

The honest answer exposes the problem: Stellantis' European reliance on Chinese partners is about 'control' not 'capability.' Control can be negotiated and mutually beneficial, but it doesn't create technological barriers. Once partners grow stronger, control becomes questionable. Management admitted European profit forecasts are 'deliberately conservative,' benchmarked against competitors' already low margins—a double-edged statement: either leaving room or lacking confidence.

South America: The Only Place 'Actually Defending' Against Chinese Automakers?

COO Herlander Zola: South America accounts for 5% of global industry volume but nearly 20% of Group sales. By 2025, it leads in volume (22%+ share) and exceeds 30% in Brazil/Argentina.

The strategy is defensive counterattack: Entry-level relies on Fiat's brand trust (Chinese struggle here); pickups represent the largest profit pool where Chinese haven't entered yet, leveraging Ram + new Dakota + Rampage/Toro/Strada (Strada leads region for five years); SUVs supplement with Jeep + Leapmotor. New growth frontiers are Andean markets like Chile/Colombia, importing Jeep/Peugeot from China/India to raise share from 5% to 10%.

The moat is concrete: High localization, industry's strongest supplier network, robust dealer network, 4,000+ local engineers, and biohybrid (electric + ethanol) tech tailored for the region.

Targets: Double-digit revenue growth, 8–10% margins, maintaining #1 position.

This is the chapter I respect most among the five regions. It's the only market 'defending against China through real capabilities, not Chinese partnerships.' Localization, ethanol hybrids, pickups (high-margin segments Chinese can't enter yet), and decades of brand trust form genuine moats, not narratives. Zola said, 'Our starting point is unreplicable by any Chinese player,' which holds true in South America.

The small irony: Even Andean growth relies on 'imports from China and India.' Clearly, 'Chinese supply' is now an irremovable thread in Stellantis' global tapestry.

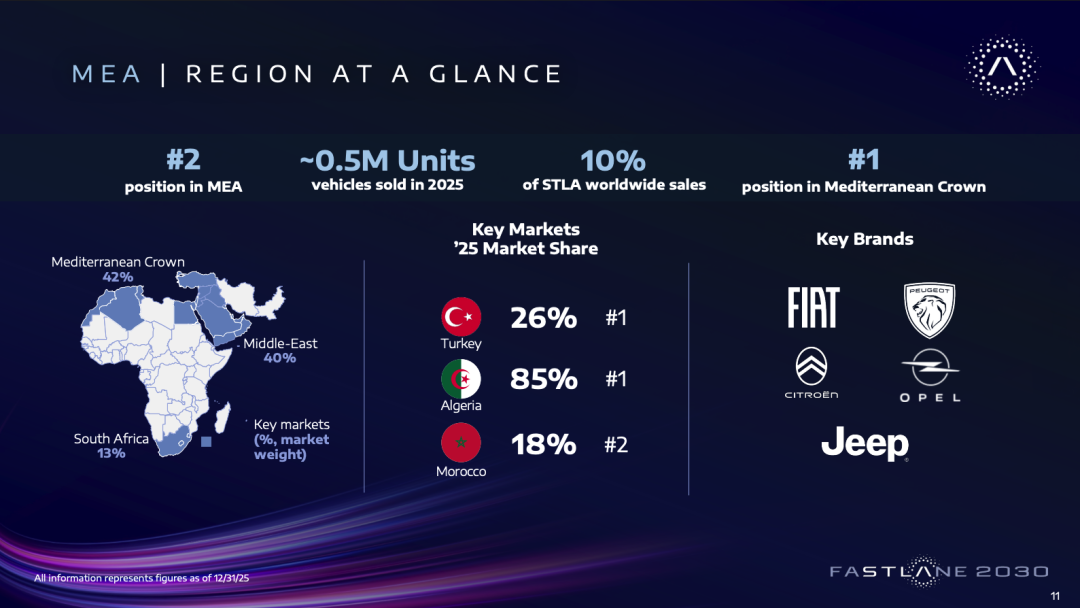

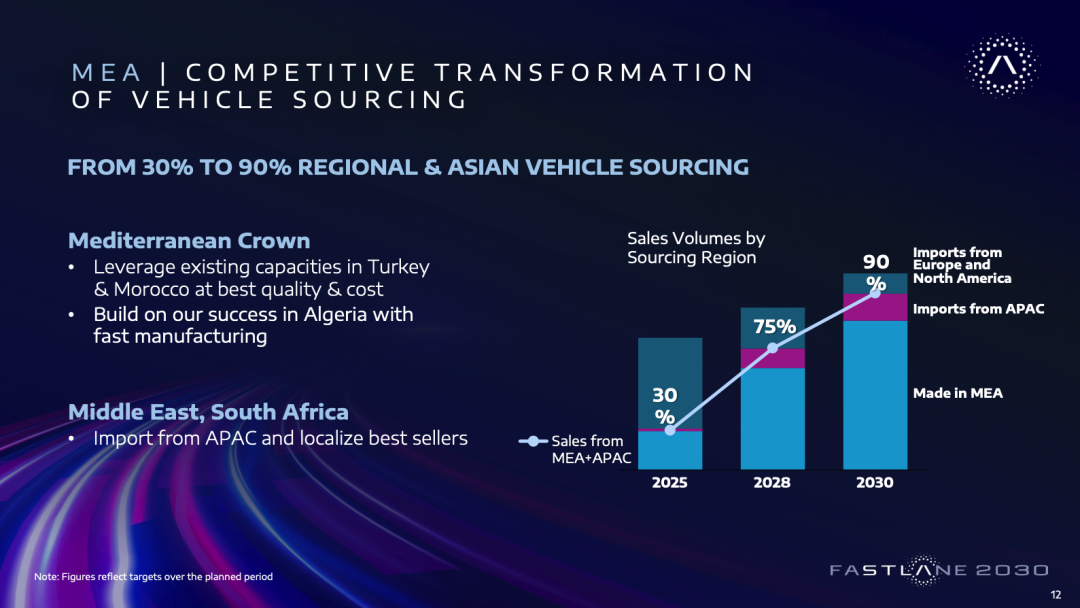

Middle East & Africa: Fastest Growth, Essentially 'Sourcing Arbitrage'

COO Samir Cherfan: Targets +40% revenue with double-digit margins, already #2 in the region for four years running with 500K+ annual sales.

The core move is raising 'local production + Asian imports' from 30% to 90%: Leveraging 800K capacity in Northern Mediterranean (Turkey via Tofa JV with Koç Group) and Morocco, supplementing with low-cost SUV/pickup imports from Asia (including Jeep CKD projects from India/China). 22 product lines drive 90% of sales with just €300M annual investment (supported by regional subsidies and partner co-investments).

40% growth is the highest among the five regions, but see clearly its essence—this is primarily sourcing arbitrage: Produce where cheap, source where cheap. Double-digit margins are proven, so the story is credible. But its heavy reliance on Asian (including Chinese) imports, plus currency and geopolitical risks, makes it a 'high-return but high-exposure' portfolio. Impressive growth, but the gold content needs discounting.

Asia-Pacific: Turning 'China Threat' into 'Global Product Engine'

COO Grégoire Olivier's chapter was shortest but strategically most significant: Asia-Pacific goes capital-light, relying on partners for local growth and global exports. Three plays:

Leapmotor: Stellantis is its largest shareholder (~20%) with two board seats, exclusively distributing its non-China sales through 51%-owned Leapmotor International. Leapmotor sold 600K BEVs in 2025 (global #6); International buys at cost and hit 11K monthly sales after 18 months. Target: 180K units next year.

Dongfeng: A 34-year partner developing four models ('two Jeeps, two Peugeots') via DPCA JV, built at Chinese costs for global export, primarily funded by DPCA (keeping asset-light).

Tata: Building a new Jeep model in India for global supply.

Total: Exporting to 50+ countries over five years with €60B+ in vehicle/model sales; Asia-Pacific itself doubles in scale with 4–6% margins.

This is the plan's smartest chapter. It neatly translates 'China threat' into 'global product and cost engine.' The Leapmotor equity stake is the real crown jewel—gaining Chinese-level cost structures and electrification speed without building from scratch. This move is far smarter than traditional giants' direct confrontation with China.

But stay sober: 4–6% margins indicate a thin-margin volume/export business, not a profit engine. And it deepens the European paradox—the more Stellantis relies on Leapmotor/Dongfeng products for global expansion, the deeper its structural dependence on Chinese partners becomes. Capital-light means ceding technological and product leadership.

IV. Financial Chapter: All Hard Commitments Piled Up for 2028

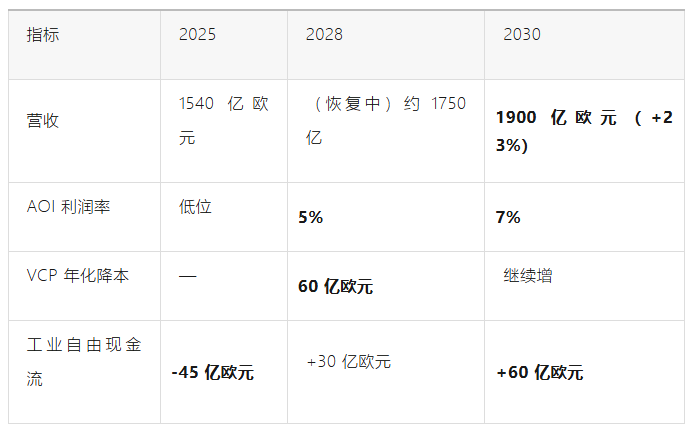

What Was Said on Investor Day

CFO Joao Laranjo presented a five-year framework with five key anchors:

Industrial free cash flow turns positive by 2027;

Five-year investment of €60 billion, approximately 7% of annual revenue, with 60% of product investment (around €22 billion) allocated to North America;

Balance sheet: Industrial net cash to grow from €6.7 billion to €15 billion+ by 2030, with total industrial liquidity around €57 billion;

Financial Services (SFS) presented by Jon Nelson: Managing €85 billion in net receivables, with U.S. business growing 21x in four years (average FICO score of 762, maintaining quality), contributing €150 million+ in AOI and €500 million in dividends to the group by 2030, positioned as a "counter-cyclical shock absorber."

Breaking down the 2028 margin bridge: Revenue growth +2.1 points, industrial cost reduction +5 points (including 3.6 from VCP), financial services +0.5, offset by raw material inflation -1.4 and SG&A +0.6.

Vehicle's Interpretation

First, this is a heavily "back-loaded" plan. 2026 is about "stabilization," with cash flow turning positive in 2027. The real hard outcomes—3% AOI margin, €3 billion in cash flow, full ramp-up of new Ram pickups, and maturation of Chrysler's new models—are almost entirely concentrated in 2028.

During Q&A, Filosa was repeatedly asked why 2028 is so critical. His answer: Because that's when all product launches and sales volumes will materialize. The problem is that pinning success on flawless execution in a single year is itself the greatest vulnerability.

Second, the "transmission rate" of the €6 billion VCP cost reduction is the linchpin of overall credibility. Oddo's analyst directly questioned: In a competitive environment where everyone is cutting costs, why should such a high proportion of this €6 billion translate to AOI? The CFO's response—that total sales costs exceed €100 billion, making the €6 billion share "not unreasonable," and that this is a net figure with raw material headwinds listed separately—holds logical weight. However, the industry-wide question of whether cost reductions will truly convert to profits rather than being eaten up by price wars remains unanswered, and difficult to resolve on the spot.

Third, the two-tiered profit structure is glaring. North America at 8–10%, Europe at 3–5%—confirming Houchois' earlier "two-tier business" observation in the financial numbers. With North America contributing 60% of profit growth, the plan's fate is highly tied to execution in one region, even one brand (Ram). The eggs remain too concentrated in one basket.

Fourth, risks are laid bare on the table, which deserves credit. Cumulative raw material headwinds of 1.4 points by 2028, USMCA negotiations, and European regulatory reviews were all disclosed by the CFO. For a financial leader who recently weathered a crisis, openly listing these risks is more credible than painting a rosy picture.

Final Thoughts

After reviewing the full day of Stellantis Investor Day 2026 presentations, the backbone of FaSTLAne 2030 can be summarized in three sentences:

Learn cost and speed from Chinese competitors, prove discipline and cash flow to Wall Street, and admit to yourself that the old path was wrong.

Its greatest strength is its clarity. The multi-regional approach is well-judged, brand pruning is ruthless, and capital-light strategies (outsourcing autonomous driving, leveraging China's ecosystem for affordable EVs, relying on Leapmotor in Asia) demonstrate smart cost savings. Even the CTO was willing to admit publicly that "the Chinese set the benchmarks." For a recently stabilized giant, this unpretentious, Apologizing attitude is now its most valuable asset.

Its greatest risk stems from the same source. Capital-light implies capability-thin. Europe faced analyst questioning about whether it "only remains a distribution business," while Middle East/Africa growth relies on procurement arbitrage, and Asia's structure enshrines dependence on Chinese partners. When critical affordable EVs, autonomous driving, and export products are all built on others' platforms, short-term financials may look impressive, but long-term moats are quietly eroding. Combined with a full suite of new technologies launching in 2027, all hard metrics deferred to 2028, and profit highly concentrated in North America—this is a plan with extremely low tolerance for error.

For readers following China's auto industry, this plan offers another intriguing angle: For the first time, a Western century-old giant so openly treats Chinese companies as both "rivals to be walled off" and "engines to be leveraged." The Leapmotor partnership merits ongoing attention—it represents both Stellantis' sharpest tool for recovery and its farthest step in ceding technological control.

So back to the original question: Is this clarity or just a placebo?

Vehicle's verdict: It wins through clarity, but clarity alone doesn't generate profits. Filosa himself said it best: Success "isn't achieved in a day, but earned day by day." The plan looks sound on paper, but the real test comes in 2028: All launches must occur on schedule, quality must avoid further scandals, the €6 billion cost reduction must translate to profits, and North America must capture 35% market share without price wars.

If any link fails, FaSTLAne will revert to an ordinary lane.

We'll reconvene then to check the accounts.

Deep analysis is hard work. Your likes, loves, and shares motivate us to keep producing high-quality information.

Source: This article is based on the complete official presentation scripts from Stellantis 2026 Investor Day. Data and statements are taken directly from the original scripts; judgments and evaluations represent the author's personal views and do not constitute investment advice.

References and Images

Stellantis Investor Day 2026 - FaSTLAne 2030 - Overall Strategy PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - Product Technology PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - Pan-Europe PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - North America PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - South America PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - Middle East PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - Asia PDF

Stellantis Investor Day 2026 - FaSTLAne 2030 - Q&A Transcripts PDF

*Unauthorized reproduction or excerpting strictly prohibited-

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once