Are Traditional Fuel Cars Really Losing Their Market?

06/11 2026

06/11 2026

547

547

“Top Ten Best-Sellers: No Traditional Fuel Cars in Sight”

Author: Wang Lei

Editor: Qin Zhangyong

After new energy vehicles (NEVs) broke through the 60% retail market penetration barrier for the first time in April, May brought an unprecedented scenario in automotive sales rankings:

Traditional fuel cars were absent from the top ten best-sellers.

According to the May passenger vehicle retail sales rankings released by Dongchedi, all ten best-selling models were NEVs. Correspondingly, the retail market penetration rate of NEVs in May soared to a new record high of 63%.

Reflecting on the start of the year, traditional fuel cars still dominated seven out of the top ten best-sellers in January, dropped to six in February, and further declined to five in March. In just four months, traditional fuel cars swiftly transitioned from market mainstays to outliers, shifting from the dominant players to a minority presence.

Judging solely by this ranking, one might hastily conclude that “traditional fuel cars are no longer in demand, while NEVs are selling like hotcakes.”

However, the reality is still some distance from the narrative of “NEVs overtaking traditional fuel cars.”

01 “The Absence of Old Favorites”

You might think that “no traditional fuel cars among the top ten best-selling passenger vehicles in May” is already quite alarming. But in fact, more precisely, traditional fuel cars were absent from the top 16 positions on the sales chart.

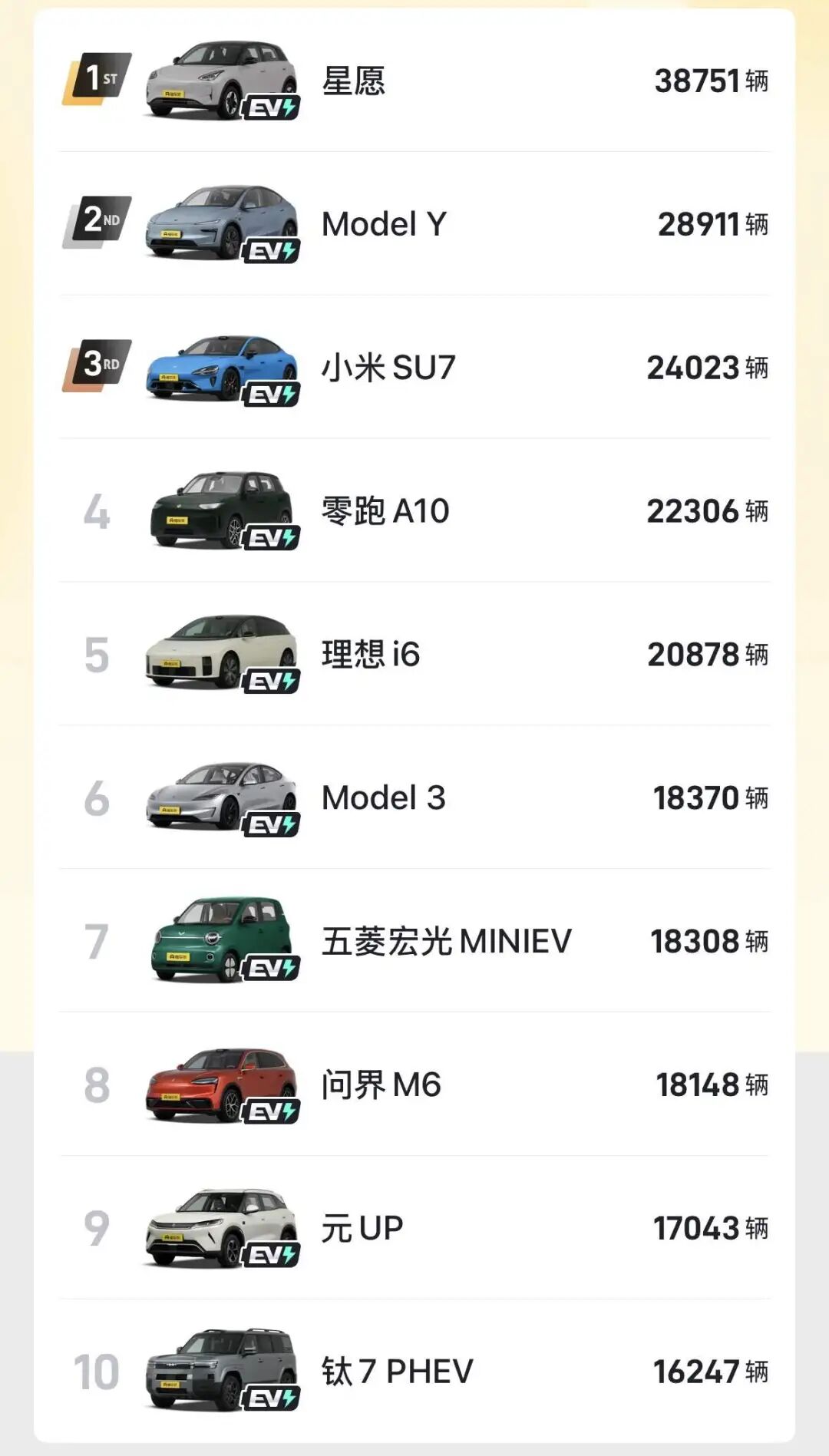

Let's first examine the passenger vehicle retail sales rankings released by Dongchedi:

Ranking first is the “national favorite” Geely Xingyuan, which topped the monthly sales chart with 38,751 units sold. Tesla Model Y followed with 28,911 units, while Xiaomi SU7, Leapmotor A10, and Li Auto i6 secured the third to fifth positions with 24,023, 22,306, and 20,878 units sold, respectively.

The remaining spots in the top ten all had monthly sales below 20,000 units, including the Model 3, Wuling Hongguang, Aito M6, Yuan UP, and Titan 7—all NEV models without exception. Moreover, domestic brands accounted for 80% of these top ten models.

The best-selling traditional fuel car in May was the Geely Boyue L, which ranked first among traditional fuel cars with 13,395 units sold but placed 17th overall. If we expand our view to the top 20 best-sellers in May, traditional fuel cars still held four spots: Boyue L, Lavida, Sylphy, and BinYue.

Among them were once iconic models, but their current sales volumes hover between 12,000 and 13,000 units.

More “iconic models” have seen even steeper declines. For example, the Toyota Corolla, which once consistently sold over 30,000 units per month at its peak, now sees its latest monthly sales drop to just over 3,000 units, ranking outside the top 100.

Joint venture stars like the Volkswagen Lavida and Toyota RAV4, which once sold 20,000 to 30,000 units per month, have also fallen outside the top 18. In the separate traditional fuel car rankings, only the top 13 models sold over 10,000 units per month, and none sold over 15,000 units.

However, just a month ago, the Geely BinYue was the last remaining traditional fuel car “holdout” in the top ten, but it has now dropped to 20th place. Two months ago, five traditional fuel cars were still on the list; in January, there were still seven traditional fuel cars, with joint venture models like Lavida and Sylphy still at the forefront.

In less than half a year, traditional fuel cars have gone from dominating the market to being completely sidelined, with their decline far exceeding expectations. At the same time, this objective fact means that the market share of traditional fuel cars is indeed continuously shrinking.

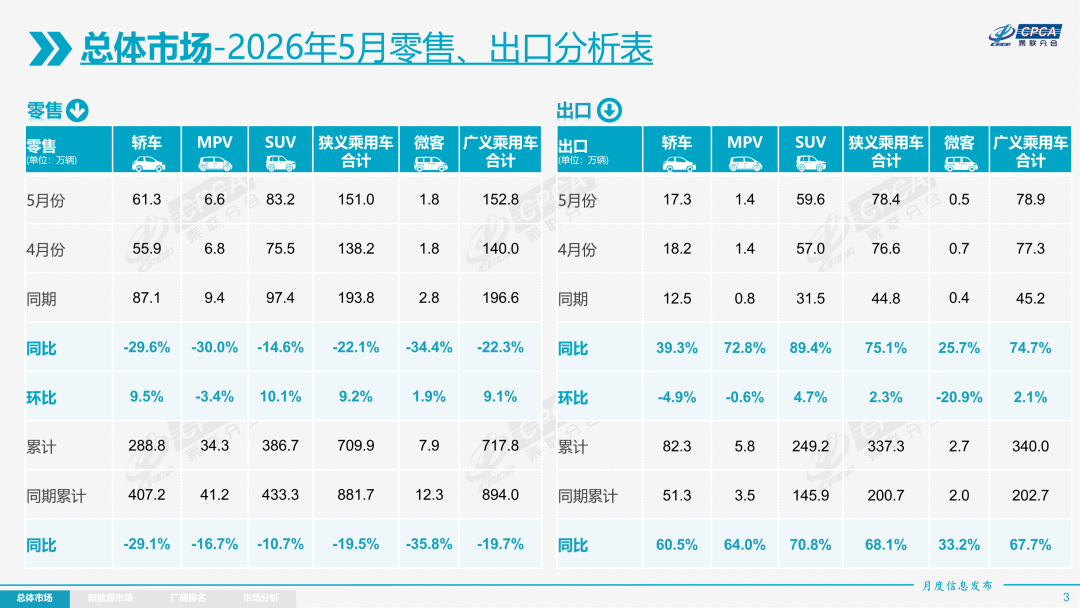

How fast is the decline? According to the latest data released by the China Passenger Car Association (CPCA), nationwide retail sales of traditional fuel passenger vehicles in May were 560,000 units, a sharp year-on-year decrease of 39%. Their market share also dropped to 37.1%.

In stark contrast, the pace of electrification substitution has exceeded expectations. Retail sales of NEV passenger vehicles reached 950,000 units, a year-on-year decrease of 7.5% but a month-on-month increase of 12.4%. The penetration rate further rose to 62.9%, setting a new historical record and increasing by 9.9 percentage points year-on-year and 1.6 percentage points month-on-month.

Meanwhile, wholesale sales of NEV passenger vehicles reached 1.352 million units, a year-on-year increase of 10.6% and a month-on-month increase of 10.3%, with the penetration rate exceeding 60% for the first time.

However, the newly broken record for NEV penetration must be viewed objectively. CPCA data shows that nationwide retail sales of passenger vehicles in May were 1.510 million units, a year-on-year decrease of 22.1%. In other words, while the NEV penetration rate surged to a historical high of 62.9%, the overall automotive market was actually shrinking significantly.

This cannot be simply attributed to rapid growth in NEV sales. In May, NEV sales also saw a year-on-year decrease, but traditional fuel car sales declined even faster. The CPCA estimates that traditional fuel cars contributed 82% of the year-on-year decline in the passenger vehicle market.

In other words, the 62.9% penetration rate reflects both the competitiveness of NEVs and the rapid contraction of the traditional fuel car market.

According to Cui Dongshu, Secretary-General of the CPCA, rising fuel prices have been the direct driving force behind this round of changes. High fuel prices have increased the operating costs of traditional fuel cars and influenced consumers' judgments about future vehicle expenses. When purchasing a car intended to be driven for five or even ten years, consumers now consider not just the initial purchase price but also the ongoing monthly costs.

This is particularly sensitive in the mid-to-low-end vehicle market, where the cost advantage of electric vehicles is substantial for those driving higher mileage.

However, fuel prices can only explain the speed of the decline, not the long-term trend. If traditional fuel cars still held significant competitive advantages, a single fuel price hike would not have caused them to collectively disappear from the top ten sales chart within a few months.

What truly changed consumer choices is that today's NEV models have closed the gaps in price, range, and product coverage while gaining advantages in power, smart cockpits, and functional experiences. The current rise in fuel prices has merely accelerated changes that were already slowly unfolding.

02 Internal Combustion Engines Aren't Going Away

It is evident that although the NEV penetration rate has continuously broken historical records in recent months, this is largely not due to a flourishing automotive consumption market but rather to the rapid decline of traditional fuel cars in the existing market.

Thus, this is not simply a story of “NEVs overtaking traditional fuel cars.” More accurately, it reflects a scenario where, against a backdrop of weak consumer confidence and a shrinking overall automotive market, the foundation of traditional fuel cars has collapsed precipitously.

Especially in May, sales of mainstream joint venture traditional fuel cars plummeted by 41%. Faced with a continuously shrinking market share, traditional fuel car manufacturers have had virtually only one response: price reductions.

Cui Dongshu stated that from January to May 2026, a total of 32 conventional traditional fuel car models saw price reductions, 13 more than the same period last year. From affordable compact cars to luxury vehicles costing tens of thousands of dollars, the magnitude of price cuts has grown larger.

Take the Civic as an example: a few years ago, it cost over 170,000 yuan to purchase, but now the base model costs around 90,000 yuan, while the high-end version costs about 100,000 yuan, according to sales staff at a Dongfeng Honda 4S dealership. Additionally, the Audi A6 saw a massive price drop of 91,000 yuan, and the Kia Sportage is now being sold at a flat price of just 109,900 yuan. Some traditional fuel models have seen price reductions approaching 30%.

The latest data disclosed by Cui Dongshu shows that in May this year, the average price of conventional traditional fuel car models with price reductions was 166,000 yuan, with an average reduction of 25,000 yuan, representing a 14.9% price cut. In the first five months of this year, the average price of new car models with price reductions in the overall passenger vehicle market was 241,000 yuan, with an average reduction of 32,000 yuan, representing a 13.1% price cut.

However, these high promotional discounts have not led to a rebound in sales; instead, inventories have continued to accumulate.

Data from the China Automobile Dealers Association shows that in April 2026, the comprehensive inventory coefficient for automobile dealers reached 1.89, up 7.4% month-on-month and 34% year-on-year, far exceeding the safety warning line of 1.5. The soaring inventory pressure reflects that sales speeds are far behind the pace at which manufacturers are pushing inventory onto dealers.

This is because when consumers see car prices continuously dropping, it easily creates a negative cycle: the more frequently prices are reduced, the more consumers feel that waiting longer will lead to even lower prices. As a result, they hold onto their cash, delaying purchases.

When price reductions shift from a short-term promotional tactic to a constant expectation, their ability to stimulate demand quickly diminishes and even begins to erode consumer confidence.

Additionally, dealers increasing discounts to clear inventory and frequent price reductions harm the interests of existing owners and the residual value of used cars. Weakening residual values further reduce consumers' willingness to purchase, leading dealers to reduce showroom space, sales staff, and marketing resources.

Manufacturers' strategic shifts are also influencing the mindset of traditional fuel car consumers. Nowadays, more and more automakers are redirecting resources away from traditional fuel cars toward NEVs. Traditional giants like Volkswagen, Toyota, and Honda are still selling traditional fuel cars, but the pace of new product releases has obviously slowed, and R&D resources are increasingly being allocated to electrification platforms and intelligent technologies.

For consumers, the signal they perceive is that even automakers themselves are moving toward NEVs, raising questions about how much longer traditional fuel cars will remain viable. Thus, traditional fuel cars are losing not just sales but also the sense of security they once provided.

Of course, the “mass exodus” of traditional fuel cars does not mean the internal combustion engine will exit the market. On the May sales chart, the Aito M6 and Titan 7 PHEV still come equipped with engines. The strong sales of extended-range and plug-in hybrid models indicate that a significant portion of consumers still value the convenience of fuel-based energy replenishment.

Additionally, among China's automotive exports in May, NEVs accounted for 54%, with the remainder primarily consisting of traditional fuel products. For automakers like Chery and Geely, which are actively expanding overseas, mature traditional fuel car platforms remain essential assets in their global strategies.

Cui Dongshu, Secretary-General of the CPCA, also stated that in the long run, “traditional fuel cars will not disappear entirely but will shrink significantly,” potentially evolving into a pattern of “high-end premium offerings + specialized utility vehicles.” For example, stable demand will persist among long-distance, high-frequency users, in regions with inadequate charging infrastructure, and in certain off-road and special-purpose markets.

-

![]()

MiniMax Price Adjustment Sparks Public Outcry: Is the $300 Billion Market Cap Myth at Risk?

-

![]()

Why Do All Cars Look Alike These Days?

-

Don't Just Focus on Financing Amounts—Look at the 'Order Truth' Behind the Commercialization of Embodied AI

-

![]()

Are Traditional Fuel Cars Really Losing Their Market?

-

![]()

Comprehensive PPT Guide to Understanding CAAM Production and Sales Data: Auto Production and Sales Declines Narrow Again in May; New Energy Vehicle Market Share and Auto Exports Reach New Monthly High

-

![]()

Chinese Cars Seize Overseas Markets: The Advent of a Winner-Takes-All Era

-

![]()

Will WeChat Start Charging Fees?

-

![]()

Cross-border 'Golden Window' in 2026: Chinese Products Sweep Across Southeast Asia