Li Auto Awards Executives 35 Million Shares Based on Performance Metrics

06/18 2026

06/18 2026

465

465

Introduction

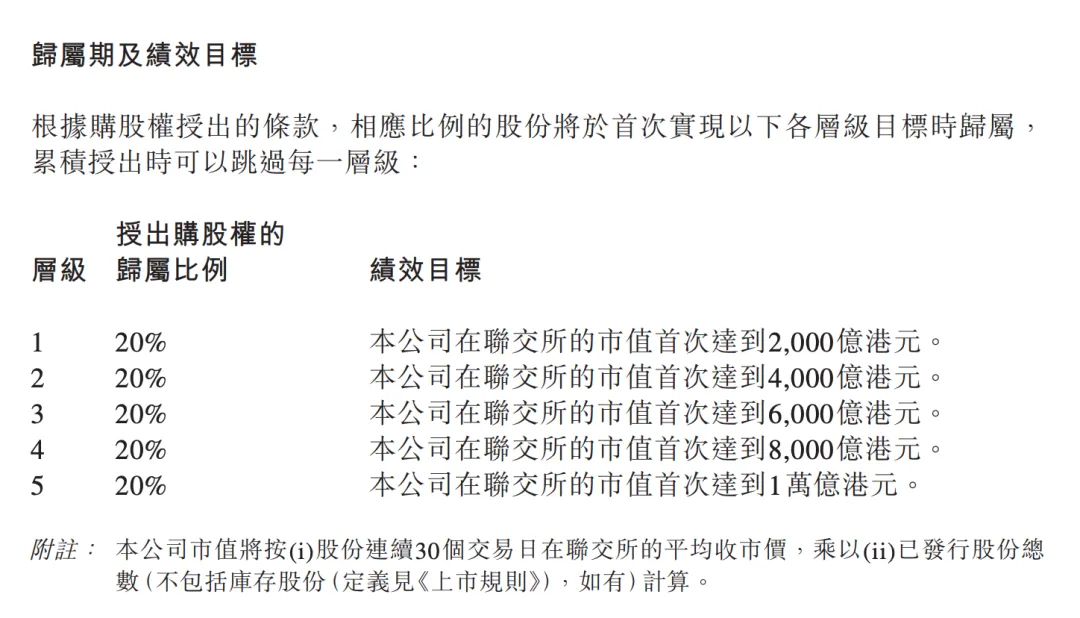

If the company fails to achieve a market capitalization of HK$200 billion, the executives receive nothing; only by reaching HK$1 trillion can they fully unlock these awards.

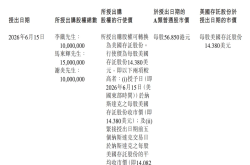

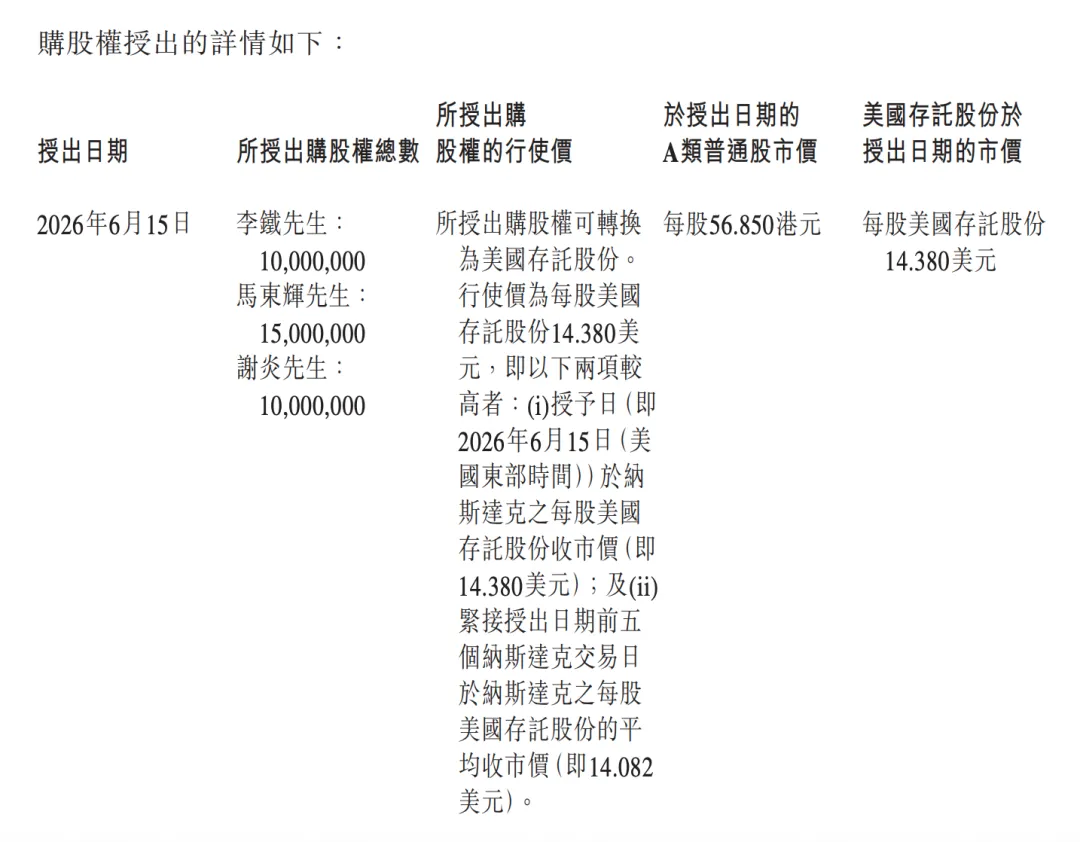

On June 15, Li Auto submitted a notification to the Hong Kong Stock Exchange, allocating a total of 35 million stock options—equivalent to 35 million Class A ordinary shares, accounting for roughly 1.62% of the outstanding shares—to CFO Li Tie, President Ma Donghui, and CTO Xie Yan.

At first glance, this move appears to be a standard equity incentive practice. Yet, when considering the evolution of Li Auto's executive compensation framework in recent years, it seems more like a subtle 're-anchoring' strategy.

Let's clarify a prevalent misunderstanding right away: This is not a 'free share giveaway.'

The exercise price is established at USD 14.38 per ADS, adopting the higher value between the closing price on the grant date or the average price over the previous five days—effectively, the current market price. For these three executives to fully exercise their options, they must personally invest approximately USD 251.65 million to purchase the shares. If the stock price does not appreciate, not only will the options yield no profit, but their invested capital will also remain locked. This is fundamentally distinct from Restricted Stock Units (RSUs) with a nominal exercise price of 1 cent—the latter represents 'deferred salary that vests over time,' while the former is a bet on the company's ability to reach new heights.

The criteria for reaching new heights are explicitly outlined in the vesting conditions: five tiers of market capitalization thresholds—HK$200 billion, HK$400 billion, HK$600 billion, HK$800 billion, and ultimately HK$1 trillion—with 20% unlocking for each threshold surpassed, based on a 30-consecutive-trading-day average.

Currently, Li Auto's market capitalization in Hong Kong stands at approximately HK$115 billion, necessitating nearly a doubling to reach the first threshold and roughly an eightfold increase to attain the final tier. A ten-year timeframe is provided, but with a clawback provision—in cases of serious misconduct or reputational harm, even vested options must be returned.

More fascinating is a detail in the announcement that might easily be overlooked: The company is transitioning long-term incentives for core management from fixed time-based RSUs to market capitalization-linked stock options. Ma Donghui's RSU count has already been 'correspondingly reduced' to reflect this change, with similar reductions planned for other key executives' RSUs in the future.

This detail is the crux of the issue.

Time-based RSUs essentially function as retention expenses—they reward presence but do not inherently ensure performance. Especially during periods when early incentive batches expire and require renewal, Li Auto faced a decision: continue issuing RSUs, allowing executive compensation to accumulate annually as book expenses, or replace this predictable payout—which appears costly on paper but is disconnected from shareholder interests—with performance-based options that only hold value if the stock price increases.

Li Auto opted for the latter.

From a corporate governance standpoint, this decision signifies something far more significant than the monetary value: management's willingness to align their mid-to-long-term wealth accumulation with shareholder interests.

Li Tie has played a pivotal role in Li Auto's financial strategy from Series A funding to its U.S. IPO; Ma Donghui oversees vehicle R&D and supply chain manufacturing; Xie Yan leads system architecture and intelligence. If these three had chosen to steadily collect their remaining RSUs and depart, no one would have blamed them. Instead, by tying their largest potential earnings over the next decade to a mechanism where 'nothing is gained unless market capitalization exceeds HK$200 billion,' they demonstrate their confidence in the company's future.

Of course, outsiders may view the HK$1 trillion target as mere grandstanding. However, a closer examination of the tiered design—each threshold represents a HK$200 billion leap, demanding sustained performance rather than one-day spikes—reveals its true intent: shifting management's focus from quarterly or annual metrics to a three-to-ten-year horizon. Short-term tactics are ineffective; only by driving sustainable compound growth in product cycles, platform efficiency, gross margins, and brand premium can market capitalization thresholds be unlocked incrementally.

Ultimately, the most intriguing aspect of the announcement is not the quantity of shares awarded but Li Auto's rare move among automakers: dismantling entrenched interest structures and repricing executive loyalty in shareholder terms.

Whether this strategy leads to a HK$1 trillion market capitalization or a prolonged wait, time will reveal the answer on the stock price curve. But on this June afternoon, Li Auto has dismantled another segment of the invisible wall between management and retail investors.

-

![]()

Chinese New Energy Vehicle Design: Stepping Out of the Shadows

-

![]()

Li Auto Awards Executives 35 Million Shares Based on Performance Metrics

-

![]()

Rushing Towards AI 2.0: How Confident is Unisound?

-

经过今年上半年各路AI豪强对市场的反复教育,有一个判断,可能决定未来一两年的走向:

-

![]()

Global Tech Sector Sees Collective Panic: Is the AI Hype Finally Deflating?

-

![]()

Three Consecutive Rises in Heavy Truck Sales: Both New and Old Players are Betting on the Same Thing!

-

![]()

Why Can’t Vivo Bridge the High-End Perception Gap Despite Support from Authoritative Media?

-

![]()

Regulatory Measures and Industry Norms: The Transformation of GEO's Trajectory in the Second Half