Sales Plummet by 60%: Are A00-Class Pure Electric Vehicles on the Verge of Extinction?

06/23 2026

06/23 2026

440

440

"From Boom to Bust": The Rise and Fall of Micro Electric Vehicles

Micro electric vehicles, once the kings of urban and rural markets due to their affordability, are now facing significant challenges.

"I haven't closed a single Panda deal in June, while the nearby Xingyuan has secured nearly 10 orders." "Most potential Wuling Hongguang MINIEV buyers have opted for Binco series models instead." "The number of customers interested in the Bestune Xiaoma has more than halved compared to last year..."

In mid-June, Bangning Studio visited several new energy vehicle stores in Beijing and noticed a stark contrast in customer interest. Micro electric vehicles are no longer the crowd-pullers they once were, with consumers now gravitating towards higher-tier, pricier models. Sales consultants also reported a sharp decline in the willingness of users to purchase micro electric vehicles this year.

At one point, a single model in this segment boasted monthly sales exceeding 60,000 units. However, in May of this year, the combined sales of the top ten models barely surpassed 30,000 units.

Data released by the China Passenger Car Association (CPCA) on June 16 revealed that from January to May 2026, sales of A00-class sedans reached 192,000 units, marking a 64% year-on-year decline—the highest drop among all segments. Their market share dwindled from 6% last year to a mere 2.7% this year, more than halving.

Within the A00-class sedan segment, micro electric vehicles were the primary sales drivers. In May, wholesale sales of domestic A00-class micro electric vehicles stood at just 87,000 units, a significant 44% year-on-year decline. Their share in the pure electric vehicle market plummeted to 10%, down 11.6 percentage points from the same period last year.

The CPCA also noted in early June that micro electric vehicles are under pressure, with sales in county and rural markets and for entry-level models experiencing a notable decline.

Micro electric vehicles once paved the way for the commuter market with their affordability and ease of use, becoming the driving force behind the popularization of new energy vehicles. Now, with sales continuing to plummet, they seem to be on the verge of being abandoned by users and the era.

▍01 The Sales Dilemma

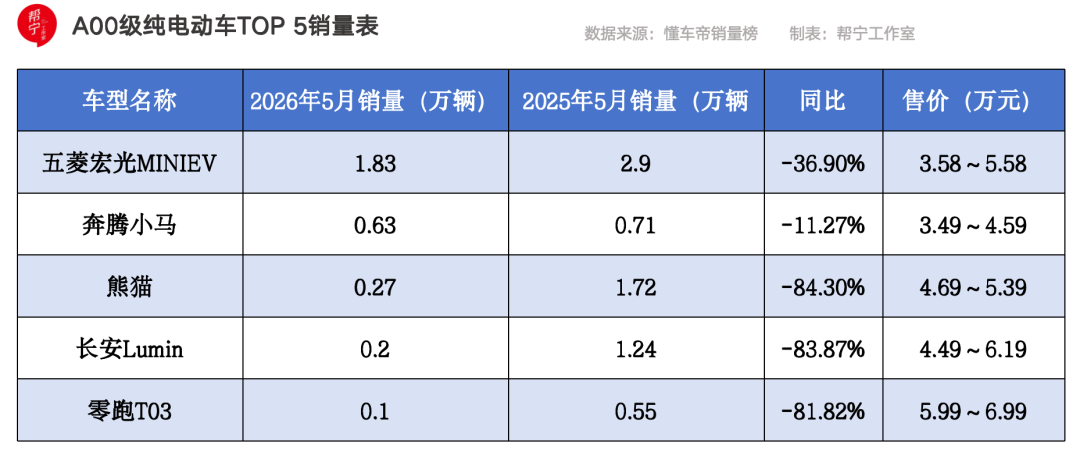

Focusing on specific models, the top five micro electric vehicle brands in May were Wuling Hongguang MINIEV, Bestune Xiaoma, Panda, Changan Lumin, and Leapmotor T03, with sales figures around 18,300, 6,300, 2,700, 2,000, and 1,000 units (979 units for Leapmotor T03), respectively.

Notably, only the Wuling Hongguang MINIEV managed to exceed 10,000 units in sales in May, whereas last year, three models—Wuling Hongguang MINIEV, Panda, and Changan Lumin—achieved this milestone. Furthermore, while the top four models recorded sales in the four-digit range in May, sales of the Leapmotor T03 and subsequent models fell short of 1,000 units.

In terms of pricing, micro electric vehicles predominantly fall within the 30,000 to 70,000 yuan bracket.

At a Geely Galaxy 4S store on Beijing's southern fourth ring road, a sales consultant mentioned that the 2026 Panda Warrior, launched on June 1, offers a pure electric range of 210 kilometers and is priced at 43,900 yuan after discounts. Including purchase tax (1,900 yuan), insurance (around 4,000 yuan), and a registration fee (500 yuan), the total cost comes to just over 50,000 yuan.

"This price definitely can't compare to last year, but it's a good deal for securing a (new energy vehicle) quota," the sales consultant remarked. "The changes in national subsidies and purchase tax have significantly impacted sales, with the number of customers buying it decreasing by more than half this year. In May 2025, this model sold nearly 20,000 units, but I recall that nationwide sales were less than 3,000 units in May this year."

What's behind these market fluctuations?

In response, Cui Dongshu, Secretary-General of the CPCA, stated that this is the result of multiple factors, including income levels, policies, demand, supply, and competition.

At the policy level, starting from January 1, 2026, the purchase tax exemption for new energy vehicles has been reduced from full exemption to a 5% reduction. For a 40,000 yuan micro electric vehicle, this translates to an additional purchase tax of around 2,000 yuan, accounting for more than 5% of the vehicle's price. This is significantly higher than the proportion of purchase tax in the price of mid-to-high-end vehicles, directly raising the bar for potential buyers.

Simultaneously, trade-in subsidy rules have been adjusted, with subsidy amounts now linked to vehicle prices. Mid-to-high-end models receive more subsidies, while micro electric vehicles, which previously relied heavily on subsidies to drive sales, have lost this policy support, further suppressing demand.

But that's not all. Early new energy purchase subsidies and automaker credit bonuses laid the foundation for micro electric vehicles to sell in large volumes at low prices. Now, with subsidies fully phased out and credit values significantly reduced, coupled with the implementation of new regulations on vehicle safety and battery thermal runaway protection, automakers face higher costs.

"Compared to mid-to-high-end electric vehicles, the core challenges in the entry-level micro vehicle segment revolve around the structural contradiction between cost and value," Cui explained. "For instance, models generally face thin profits or even losses; their size is inherently limited, leading to prominent safety shortcomings; cost constraints result in the normalization of feature reductions, fostering a fixed perception of being low-end and unsafe; technology upgrades are limited, trapping automakers in a vicious cycle of low quality and low prices; and the market survival space continues to narrow."

Under these multiple pressures, the profit logic of micro electric vehicles has collapsed.

"User preferences are shifting towards models with larger space, fuller configurations, and longer ranges," added Zhang Hong, a member of the expert committee of the China Automobile Dealers Association. "A00-class models fall short in these areas, making it difficult to meet consumer demands for family practicality, intelligent configurations, and reliable range. Their market space is being squeezed by A0-class and higher models."

Zhang believes that early users were more concerned about purchase costs and were willing to pay for low-priced micro electric vehicles. Now, they prioritize the comprehensive value of products, including range, intelligent configurations, safety performance, and space comfort. They no longer purely pursue low prices but hope to obtain a better user experience at a reasonable price.

At a Wuling 4S store on Beijing's eastern fifth ring road, Bangning Studio observed that customers showed more interest in the A0-class Binco series models compared to the Wuling Hongguang MINIEV. At the Geely Galaxy 4S store, customers gathered around the Xingyuan display vehicle, and most of the vehicles sold, as shown on the sales consultant's order page, were Xingyuan models, with no orders placed for the Panda yet.

These phenomena are not isolated. A Wuling sales consultant in Suzhou, Jiangsu, mentioned that the current price of the Binco Pro is only 10,000 to 20,000 yuan higher than that of the Wuling Hongguang MINIEV but offers superior configurations and space. More than half of the customers who come to see the Wuling Hongguang MINIEV end up ordering models from the Binco series.

The Binco Pro has an official guide price ranging from 56,800 to 70,800 yuan, offering two pure electric range options of 330 kilometers and 403 kilometers, with a fast charging time of 35 minutes. The interior features a five-seat layout, standard cruise control, and optional automatic parking.

For a difference of just over 10,000 yuan, consumers get a comprehensive upgrade in range, space, configurations, and comfort. The preference of rational consumers is self-evident. A0-class models have collectively lowered their prices, achieving a leap in experience with a small price difference, forming a significant competitive threat to A00-class micro electric vehicles.

As a result, the entire A00-class micro electric vehicle market has fallen into a dilemma of low prices without profitability and upgrades leading to market loss. Industry reshuffling is already in full swing.

▍02 The Transformation Path

Several interviewees stated that, from the perspectives of travel needs, market growth, and industrial value, micro electric vehicles are not a sunset industry. The rigid demand for short-distance micro-travel has never disappeared, and the segment still possesses long-term development potential.

Cui Dongshu believes that the future micro electric vehicle segment will witness a surge in total volume, structural upgrades, and a highly concentrated development pattern, likely following the trajectory of traditional fuel micro-vehicle phase-outs. Small and medium-sized players will gradually be eliminated, with a significant trend towards industry oligopoly.

Overall, micro electric vehicles will shift from being a sales mainstay to serving as an entry point for automakers into lower-tier markets and a core category for overseas expansion. They will no longer be the main battleground for domestic industry competition.

However, from the perspectives of market rigid demand and growth potential, the value of micro electric vehicles is irreplaceable.

Firstly, there is the rigid demand support from travel scenarios. In domestic urban and rural areas, daily commutes of 5 to 15 kilometers, picking up and dropping off children, and grocery shopping are the most mainstream short-distance travel scenarios. Micro electric vehicles, with their compact size, easy parking, and low energy consumption, are perfectly suited for complex road conditions such as old residential areas and narrow rural roads. This basic demand will not disappear with consumption upgrades.

However, some industry insiders also believe that A00-class micro electric vehicles are destined to exit the Chinese market due to consumption upgrades and price reductions of A0-class vehicles, which have left A00-class vehicles at a disadvantage in terms of space, range, configurations, and safety.

Secondly, there is the vast compliant replacement space. Domestically, there are over 20 million non-compliant "old man's scooters" used for commuting, which lack compliant qualifications and pose significant traffic safety hazards. As traffic regulations tighten across regions and non-compliant models are gradually phased out, "old man's scooters" may be replaced by compliant micro electric vehicles, becoming a stable source of incremental growth for the latter.

Looking overseas, A00+A0-class affordable pure electric vehicles are the main force in new energy vehicle exports. In May, pure electric models accounted for 59.3% of total new energy exports, with A00 and A0-class pure electric vehicles accounting for 53.8% of pure electric vehicle exports, showing a slight year-on-year increase and proving their competitiveness in overseas markets.

The potential of lower-tier markets cannot be overlooked.

The largest incremental space for new energy vehicles in China is concentrated in third-tier and lower cities, counties, and villages. Entry-level models priced between 30,000 and 70,000 yuan are the most acceptable to users in these lower-tier markets.

From a positioning perspective, micro electric vehicles play a crucial role in cultivating first-generation new energy users and popularizing awareness of electric travel. They serve as vanguards for new energy vehicles to penetrate lower-tier markets.

Currently, charging infrastructure in some county and rural areas is still imperfect. However, with the integrated advancement of urban and rural infrastructure, the coverage of charging stations continues to improve, and the market penetration rate of micro electric vehicles will further increase.

Although the outlook is optimistic, the growth dilemma is an urgent issue that needs to be addressed.

Cui Dongshu proposed that over the next 1 to 3 years, the core breakthrough logic for micro electric vehicles will be a shift from low-price internal competition to a new development model featuring scale-based cost reduction, value empowerment, and scenario segmentation. This requires coordinated adjustments from policies, the industry, and automakers.

At the policy level, it is necessary to implement dedicated product standards for affordable electric vehicles, introduce a simplified C6 dedicated driver's license system, and form a full-chain regulation covering vehicles, people, and roads. Simultaneously, continue subsidies for rural areas, credit incentives, and purchase tax preferences, improve charging infrastructure in counties, and support the popularization of lower-tier markets.

At the industry level, it is essential to build shared modular platforms and low-cost supply chains, promote industry-wide technology cost reductions, establish a unified safety rating system, regulate market order, and squeeze out non-compliant models through price reductions.

At the automaker level, it is crucial to adhere to a low-price strategy while achieving baseline upgrades in product safety, range, and intelligence. Focus on segmented scenarios such as home commuting, shared leasing, and overseas exports. Reconstruct the cost system through technological iteration and supply chain optimization to ensure low prices without compromising quality, creating high-cost-performance affordable commuter models.

At present, automotive manufacturers like Wuling, Leapmotor, and Chery have taken the initiative. The Wuling Hongguang MINIEV has rolled out a long-range variant boasting a range exceeding 300 kilometers. Meanwhile, the Leapmotor T03 has incorporated advanced safety features, such as active braking, with the goal of enhancing user confidence through product enhancements.

Zhang Hong posits that tailored models can also be developed for specific scenarios, including urban commuting, shared mobility, logistics distribution, and senior travel, to cater to a wide array of demands. (Here, “segmented scenario” is adjusted to “specific scenarios” for better fluency and understanding in English, and the redundant “segmented scenarios” in parentheses is removed.)

Moreover, it is essential to foster collaboration among automakers, battery producers, charging infrastructure operators, and technology firms to collectively construct an intelligent transportation ecosystem. This will facilitate resource sharing and leverage the complementary strengths of each participant.

Simultaneously, new policies could be implemented to incentivize technological and model innovations by automakers, support emerging business models such as vehicle-to-grid interaction and battery swapping, and foster sustainable industry growth.

It is foreseeable that, through multi-stakeholder collaboration, micro electric vehicles priced in the tens of thousands of yuan range will not vanish. Instead, they will shed their former reputations for being low-priced and low-specification, evolving towards refinement, standardization, and scenario-based development. These vehicles will continue to play a pivotal role as trailblazers in the popularization of new energy vehicles.

-

![]()

【OFweek Weike Cup】Fair Optics Officially Nominated for 2026 Outstanding Contribution Award in Optical Industry Application Solutions

-

![]()

The Competitive Landscape of Financial AI Agents in the 'Long Tail' Market: FinTech Subsidiaries, Financial Leasing, Consumer Finance, AMCs, and Other Players Making Quiet Strides

-

![]()

【OFweek Weike Cup】Fair Optical Officially Enters for the 2026 Optical Industry Annual Innovation Product Award

-

![]()

【OFweek Weike Cup】Wuhan Changjin Photonics Nominated for 2026 Optics Industry Outstanding Component Supplier

-

![]()

【OFweek Weike Cup】Xinyuan Optics Officially Enters for the 2026 Outstanding Contribution Award for Advanced Manufacturing Process Solutions in the Optical Industry

-

![]()

Who Dominates the World Cup: Lenovo, Hisense, or Mengniu?

-

![]()

【OFweek Weike Cup】Shijia Photonics Participates in the 2026 Excellent Optical Component Supplier Award

-

![]()

【OFweek Weike Cup】Dingxinsheng Optics Officially Enters for the 2026 Optical Industry Annual Innovation Product Award