All Staff Face Pay Cuts/Salary Suspensions: This Leading Auto Dealer Group Can't Endure Any Longer

07/07 2026

07/07 2026

345

345

Lead-in

Introduction

Domestic sales plummet by 20%, and dealers are the first to bear the brunt.

Recently, an urgent internal memo issued by the Human Resources Department of the Lantian Group has been widely circulated in automotive industry circles and on social media platforms, sparking heated discussions across the internet.

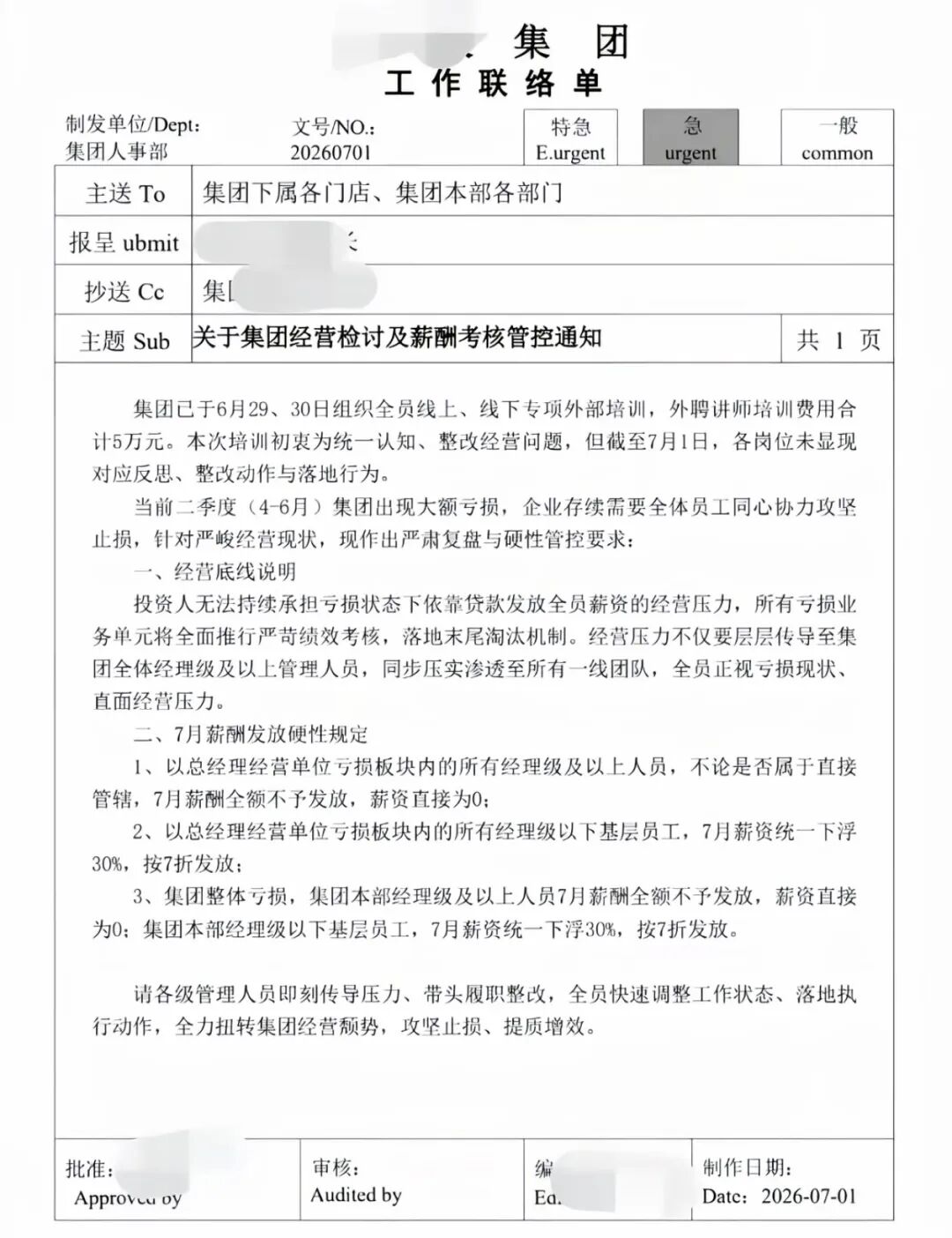

The memo reveals that due to significant losses in the second quarter, investors are no longer able to continue providing loans to support full staff salaries. Consequently, the group has implemented a differentiated salary control policy. Salaries for managers and above at the group headquarters and all unprofitable stores will be completely suspended in July, while on-duty grassroots employees will receive only 70% of their monthly wages. Simultaneously, the assessment mechanism will be tightened, with increased efforts to eliminate underperformers. Managers at all levels are required to fully communicate operational pressures, with all staff sharing the burden of losses.

In particular, the phrase "no longer able to continue providing loans to support full staff salaries" indicates that the Lantian Group has fallen into a precarious situation of cash flow difficulties and potential insolvency amid the downturn in the automotive retail industry.

In fact, at the end of June, the Lantian Group had just spent 50,000 yuan organizing a training session on operational rectification for all staff in an attempt to reverse the losses. However, the rectification efforts fell short of expectations, leading to the immediate implementation of pay cuts and salary suspensions. The stark contrast between spending money on training and rectification while directly cutting employee salaries has drawn sighs from many industry practitioners.

After the news spread, it sparked heated discussions among industry insiders, with a large number of netizens flooding the short video account of Lantian's Chairman Tang Guohua to leave comments seeking the truth behind the incident. Many netizens also pointed out that the plan carries obvious legal risks, as unilateral deductions and suspensions of labor remuneration would almost certainly result in employees winning arbitration cases.

In addition to the eye-catching salary policies, netizens also exposed the Lantian Group's strict internal management model.

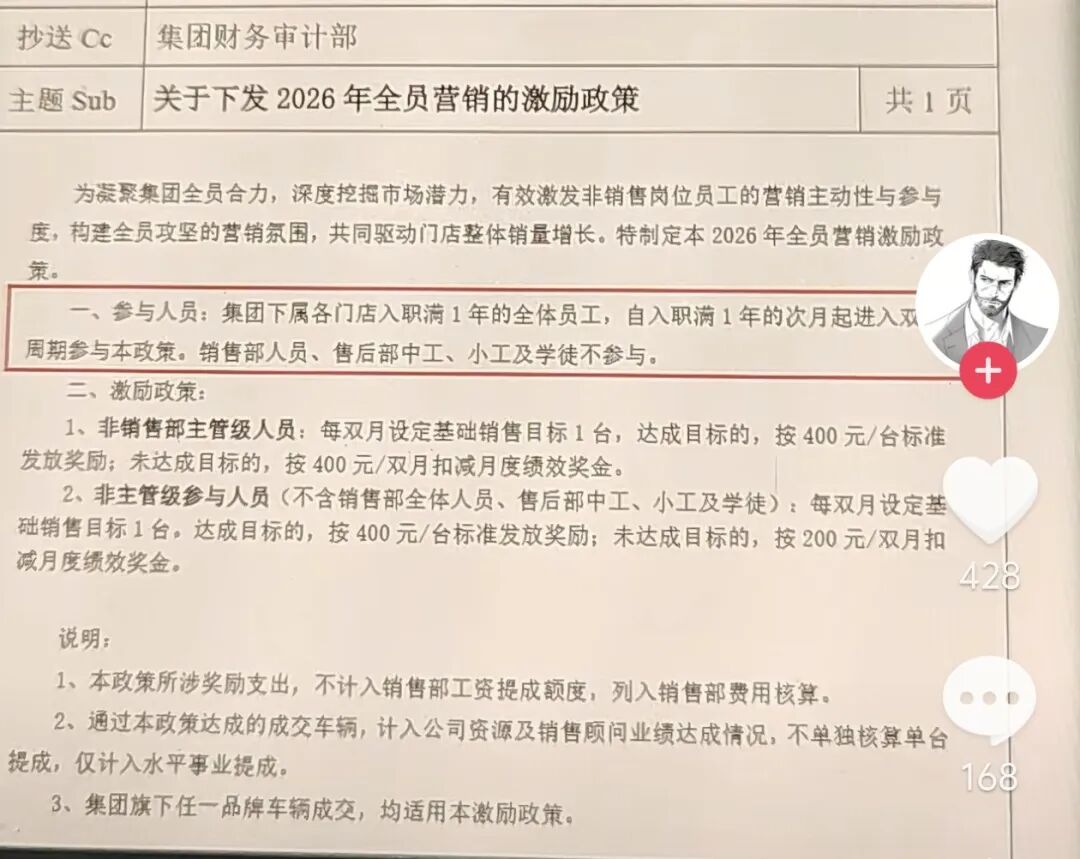

Earlier this year, the Lantian Group implemented an all-staff marketing incentive policy. For non-sales department supervisors, a sales target of 1 unit was set every two months, with a reward of 400 yuan per unit for those who met the target and a deduction of 400 yuan in performance bonuses for those who did not. For non-supervisory participants, a sales target of 1 unit was also set every two months, with a reward of 400 yuan per unit for those who met the target and a deduction of 200 yuan in performance bonuses for those who did not.

In daily assessments, Lantian's management has also faced criticism from outsiders. For example, front-desk staff caught looking at their phones while on duty would be fined 2,000 yuan, while failure to promptly answer work calls after hours would result in a 500 yuan fine. Other violations of group rules and regulations would incur fines ranging from 500 to 2,000 yuan.

At the same time, in terms of corporate culture, employees are required to blur the boundaries between work and off-duty hours, prioritize completing work before resting, and be willing to make personal sacrifices for work. This has been widely regarded by many as workplace PUA (Pick-Up Artist, here used metaphorically to describe manipulative or coercive workplace behavior), triggering a concentrated release of negative emotions from many employees online.

As of now, the Lantian Group has not issued an official statement to confirm or refute this internal notice. However, the authenticity of the leaked document, which is fully marked with the group's internal document number and approval signatures, has been widely recognized by the industry.

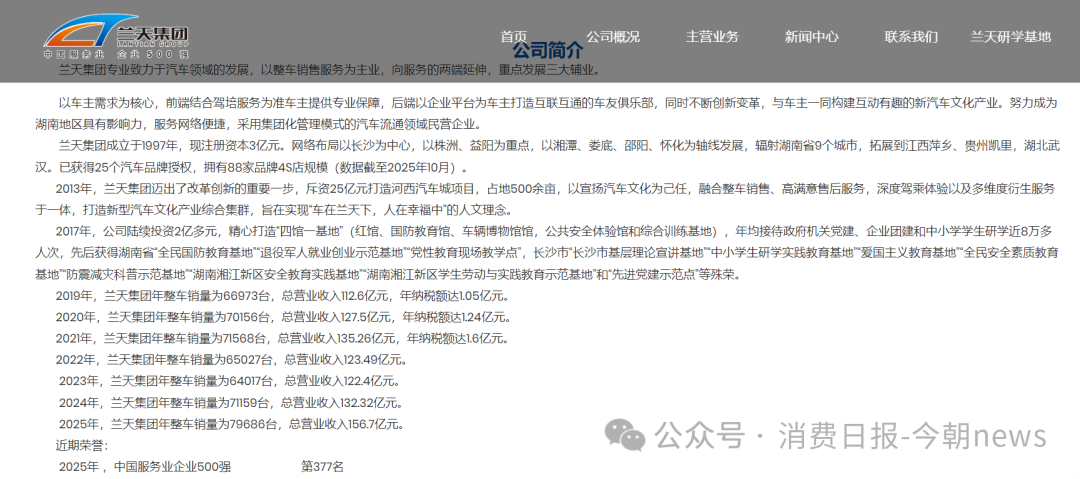

The Lantian Group, the protagonist of this controversy, is a top-tier private automotive circulation giant in Central China. Established in Zhuzhou in 1997, the company has grown over nearly three decades to rank 36th among the top 100 automotive dealers nationwide in 2025. Its business covers multiple locations across Hunan Province, with additional layouts in Pingxiang, Jiangxi; Kaili, Guizhou; and Wuhan, Hubei. Spanning four provinces—Hunan, Hubei, Jiangxi, and Guizhou—the group operates nearly 90 4S dealerships and represents 25 mainstream fuel and new energy vehicle brands. In 2025, the group's annual automotive sales approached 80,000 units, with overall revenue exceeding 15.6 billion yuan and over 3,000 employees on staff. It holds a pivotal position in the local automotive retail market in Hunan.

Against the backdrop of a year-on-year decline of over 20% in terminal retail data in the first half of this year and the overall poor survival status of the dealer industry, the salary suspensions and pay cuts at Lantian are merely a microcosm of the deteriorating survival conditions of dealers. The combination of the company's own shortcomings and systemic industry-wide challenges has led to a concentrated outbreak of multiple pressures, ultimately pushing cash flow to the brink of insolvency and necessitating short-term survival through cost-cutting measures, including labor costs.

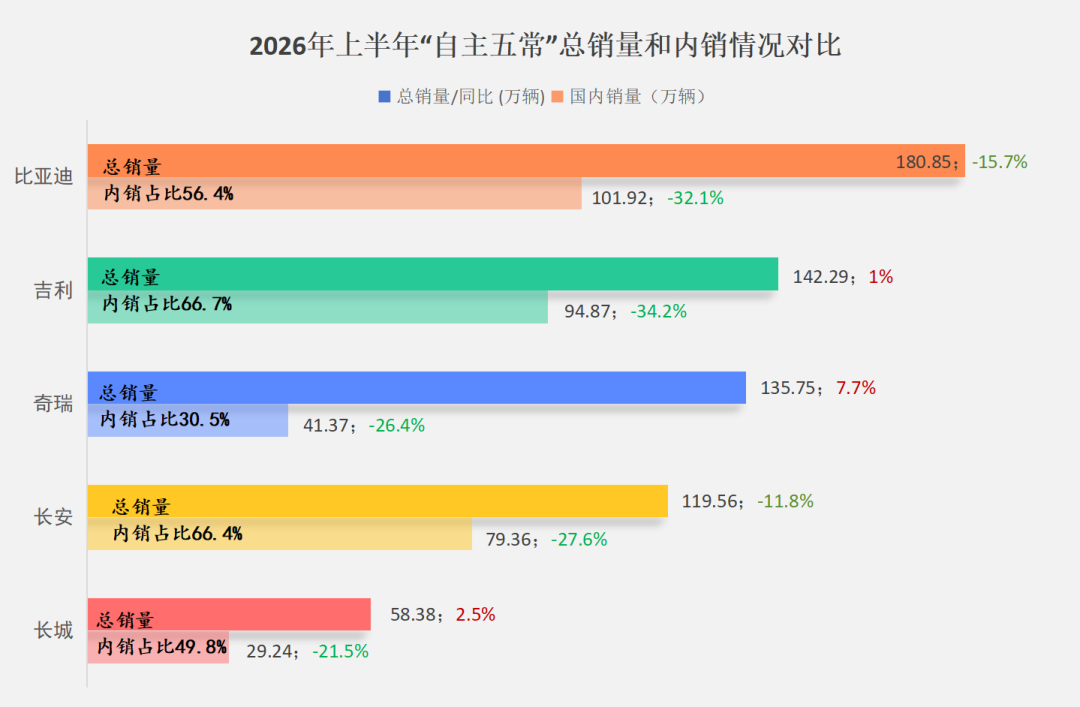

In the first half of 2026, domestic passenger vehicle retail sales declined by approximately 20% year-on-year. Leading domestic brands such as Chery and Changan saw domestic sales drop by more than 25%, while BYD and Geely experienced declines exceeding 30%. The decline in the joint-venture fuel vehicle market was even more severe.

Industry data shows that in June 2026, China's automotive dealer inventory alert index stood at 57.2%, remaining above the 50% threshold for 48 consecutive months. Over 80% of dealers are facing varying degrees of inventory backlogs, with the channel side confronting threefold pressures of "price inversion, capital occupation, and expanding store losses."

The fact that a top 100 automotive dealer group with annual revenue of 15.6 billion yuan cannot withstand losses underscores that the industry downturn has spread to top players. Regardless of size or region, with domestic sales declining this year, dealers nationwide may face a round of deep culling, while the development landscape at the dealer level will also undergo some reshaping.

Firstly, the fuel vehicle channel will be the first sector to be cleared out in this round of reshuffling. In 2025, 4S outlets for joint-venture and luxury brands contracted by 5.7% and 5.8%, respectively. With continued weakness in domestic retail sales this year and fuel vehicles being hit by high fuel prices, the pace of store closures will accelerate. Automakers and dealers that solely focus on joint-venture fuel vehicles and lag in new energy vehicle (NEV) transformation will face sustained survival pressures. Only those dealerships that have proactively positioned themselves in domestic NEVs and established comprehensive after-sales systems for the three core components of electric vehicles (batteries, electric motors, and electronics) can rely on incremental growth to stabilize their core business.

Secondly, the community of interests between automakers and dealers is gradually disintegrating. During market upswings, automakers and dealerships shared the benefits of sales growth. However, as the market contracts, automakers, in an effort to stabilize wholesale figures, continue to impose unrealistic wholesale targets on the terminal market, shifting all inventory and loss risks downward to dealers. Currently, dealer satisfaction has plummeted to a historical low of 60.8 points, with channel trust continuously eroding. The earlier rumors of conflicts between Chery and its dealer network, which spread throughout the industry, are a direct reflection of this supply-demand contradiction. When survival becomes an issue, there is no such thing as dignity.

With inventory pressures remaining undigested, dealers have only two paths to self-rescue: either shut down loss-making stores or cut labor costs. However, either choice will impact the stability of the entire vehicle distribution channel, inevitably forcing automakers to adjust their inventory pressure, assessment, and rebate rules, thereby affecting the overall performance of the retail market.

The era of industry upheaval is accelerating, signaling the definitive end of the era of reckless store expansion. Lean and refined operations will become the only path to survival for automotive dealers. This crisis and the need for lean operations are also sounding an alarm for automotive OEMs.

In previous years, domestic brands went on a frenetic channel expansion spree, with BYD approaching 8,000 outlets and Chery and Geely each exceeding 2,000 stores. When market growth was sufficient, more stores meant stronger coverage capabilities. However, with a significant decline in domestic retail sales now and a shrinking market pie, excessive stores only lead to intra-city price-cutting and intensified competition. This is the fundamental reason why most dealers are trapped in the industry quagmire of price inversion and thinning profit margins despite sales growth.

The China Automobile Dealers Association has also provided clear guidance, stating that the primary task for dealers at present is to cut costs and stem losses by building new profit models through used car sales and full-cycle after-sales services. The era of relying solely on new vehicle price differentials for profit is over. All automotive dealer groups, including automakers, must embark on lean operations, dynamically adjusting stores with prolonged losses and low output, reducing redundant manpower, and abandoning the old mindset of trading scale for market share.

It is certain that more dealers will face cash flow crises in the future, with pay cuts, layoffs, store transfers, and closures becoming industry norms. Well-funded automotive groups that have proactively completed their new energy vehicle positioning may continue to integrate smaller dealerships facing operational difficulties.

As upstream OEMs, in the face of these changes, they need to rebalance their wholesale targets with the terminal market's capacity to bear them, adjust inventory control and rebate distribution mechanisms, and rebuild a symbiotic and win-win cooperative relationship with dealers. After all, in the short term, dealers and OEMs remain inextricably linked.

The collapse of the dealer system affects not just cash flow and profits but also, more critically, represents the final buffer mechanism for the entire industry to cope with downturn cycles. Once this buffer is breached, there will be no one left to sound the alarm before the next shock. When facing terminal demand fluctuations, OEMs will no longer have dealers to take the first hit.

Editor-in-Charge: Li Sijia Editor: He Zengrong

THE END

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models