Behind the Nearly 45% Revenue Surge, Zoomar Optics Gears Up for a Brighter Future

02/27 2026

02/27 2026

710

710

On February 27, Zoomar Optics unveiled its 2025 annual earnings preview, revealing a total operating revenue of 658 million yuan, marking a significant 44.79% year-on-year increase. Net profit attributable to shareholders reached 63.46 million yuan, up 18.77% year-on-year, while net profit excluding non-recurring items stood at 48.10 million yuan, a 3.74% rise from the previous year.

This disparity, where revenue growth substantially outpaces profit growth, is crucial for understanding the current development phase of this optical enterprise.

The 44.79% revenue hike is no mere coincidence. In its announcement, Zoomar Optics attributed this growth to its continuous efforts in enriching product lines, upgrading the product matrix, and achieving expansion across multiple sectors, including intelligent surveillance and sensing, mobile robotics and intelligent driving, high-definition shooting and display, as well as industrial processing and inspection.

This multi-faceted growth trajectory underscores the company's ability to form a scale effect within its optical lens product matrix, enabling it to capitalize on the prosperity cycles of diverse downstream application scenarios simultaneously. However, the relatively modest net profit growth belies the company's strategic investments aimed at fueling future growth.

Notably, the company completed the acquisition of a 51% stake in Hunan Daisy Optics Co., Ltd. during the reporting period. This move transcends mere financial consolidation for revenue enhancement; its deeper significance lies in the vertical integration of the industrial chain.

Daisy Optics' technological prowess in areas such as optical coating and laser optical components complements Zoomar Optics' strengths in precision optical lens design and manufacturing. This synergy aligns perfectly with the current high-growth cycle of the optical communication industry. As AI-driven data centers transition towards 800G and even 1.6T, optical interconnection becomes indispensable, and the surging demand for LiDAR and optical communication modules further underscores the strategic value of this acquisition.

Zoomar Optics' capacity expansion strategy is equally noteworthy. The gradual commissioning of its wholly-owned subsidiary, Pinghu Zoomar, despite incurring capitalized construction-period expenditures and trial-run costs that exerted pressure on net profit in the current period, lays a solid physical foundation for the company's subsequent capacity growth. Amidst widespread supply chain uncertainties in the industry, this counter-cyclical expansion of intelligent manufacturing capacity for high-end optical lenses reflects the company's optimistic outlook on downstream demand and its resolve to capture market share.

The continuous increase in R&D investment represents another strategic pillar. As product types, customer base, and application areas expand, the growth in R&D personnel salaries, material procurement, and equipment purchases, although diluting profits in the short term, stockpiles technological momentum for the company's future rapid development. Meanwhile, the share-based payment expenses recognized in 2025 from the restricted stock incentive plan introduced in 2024 also contribute to short-term profit fluctuations. However, the long-term value of this mechanism in stabilizing the core R&D team and fostering innovation vitality cannot be overstated.

Currently, the industry is transitioning from isolated technological breakthroughs to system solution competition, where simple lens or lens manufacturing can no longer meet the demands of complex scenarios such as machine vision, intelligent vehicles, and AI perception. Through internal R&D and external mergers and acquisitions, Zoomar Optics is constructing a vertical system that integrates optical components, lenses, and modules, with this solution capability becoming a new competitive threshold.

For Zoomar Optics, the 2025 financial report serves as a testament to its accumulated strength. Although expenses from R&D investment, infrastructure costs, and M&A integration have impacted short-term profit release, the 44.79% revenue growth attests to its product definition capabilities and market expansion efficiency. With the completion of capacity ramp-up at the Pinghu base, deeper integration and synergy with Daisy Optics, and the gradual conversion of R&D investment into high-value-added new products, the situation of revenue growth without proportional profit increase is expected to improve in the future.

In the optical field, which demands patience and accumulation, Zoomar Optics is building deeper moats for long-term competition, a strategy that will be validated through continuous realization in the coming quarters.

-

On the Eve of Its IPO, Avatr Finds Itself Embroiled in a 'Farce of Controversy and Belittlement'

-

![]()

Yutong Optics' Japanese Subsidiary Unveiled in Tokyo, Shifting Strategic Focus to Technology-Driven Growth

-

![]()

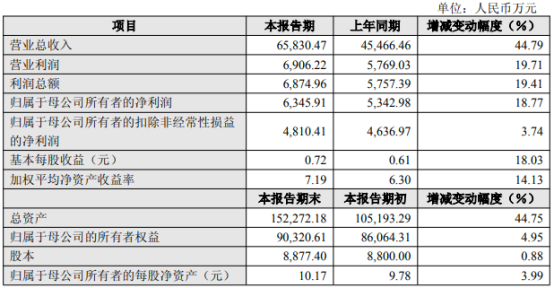

Half-Year Revenue Outstrips Last Year’s Total! Zhongrun Optics Forecasts 80.2% H1 Revenue Growth

-

![]()

Why Does AI Competition Start with Computing Power?

-

![]()

Apple AI Finally Makes Its Debut in China, Yet iPhone's 'AI Autonomy' Faces Uncertainty

-

![]()

Apple AI and QianWen Make Up Lessons: Alibaba Has Its Own 'Doubao Phone'

-

![]()

QianWen Joins Apple, Signal for Large Models to ‘Fade into the Background’

-

![]()

The ‘Anchor’ Strategy of Google Hidden Behind the Bleeding Financial Report