AI Chips Inundate the Market: Can Cambrian Emerge as China's 'NVIDIA'?

06/03 2026

06/03 2026

621

621

Cambrian's ascent can be credited to both the opportunities of the era and its inherent strengths. Conversely, its decline mirrors a confluence of multifaceted factors, notably market dynamics.

Beyond Huawei Ascend and Cambrian, a multitude of firms, including Moore Threads, Biren, Enflame, T-Head, Hygon, and Kunlunxin, are jostling for supremacy in the AI chip arena.

Even in the AI and chip sectors, which are currently awash with speculative capital, there will inevitably come a time when the tide recedes and the dividend peak is reached. Overseas, AI computing power is flourishing, while domestically, every player aspires to be the next NVIDIA, or at least the next Intel or AMD. However, industrial competition ultimately hinges on commercialization outcomes, and establishing a forward-looking competitive moat is equally vital—posing the greatest challenge to those still in the fray.

Over the past few years, Cambrian's stock price has been on a wild ride, with market sentiment oscillating and numerous debates ensuing. On the surface, the company has transitioned from losses to a single-quarter profit of 1 billion yuan, even surpassing Kweichow Moutai to claim the top spot in the A-share market. Some argue that Cambrian is now undergoing a long-overdue valuation correction. But is this truly the case?

01 Comparable to the chip industry's 'Moutai,' yet teetering on the brink of A-share dominance

Focusing solely on Cambrian's stock price trajectory over the years, certain moments indeed evoke the thrill of a 'rollercoaster' ride. In February 2024, Cambrian's stock price briefly dipped below 100 yuan. By August 28, 2025, it officially surpassed Kweichow Moutai with a closing price of 1,587.91 yuan, becoming the highest-priced stock in the A-share market—a feat accomplished in under two years.

The battle for the 'stock king' crown was equally dramatic: On August 27, 2025, Cambrian briefly overtook Moutai during intraday trading before retreating by the close. Subsequently, its stock price fluctuated wildly, opening high one day and low the next, enduring a prolonged period of volatility. News searches for Cambrian's stock price reveal a near-simultaneous reporting of both gains and declines.

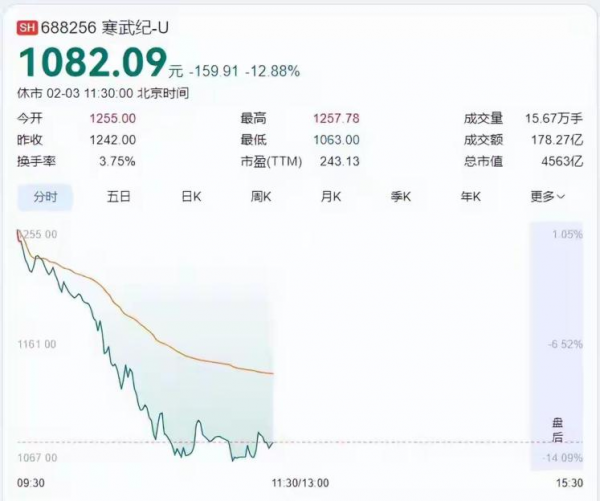

This extreme volatility is not an isolated incident from years past. Even in 2026, Cambrian's stock price has continued to experience significant ups and downs. For instance, on February 3, 2026, its stock price plummeted during intraday trading, falling nearly 13% by midday, with its market capitalization retracting to around 450 billion yuan, evaporating over 70 billion yuan in value.

In the following months, it fluctuated amid turbulence until recently surging. On April 30, Cambrian's market capitalization hit 716.8 billion yuan with a daily limit-up, and its stock price reached 1,699.96 yuan. By May 6, its market cap exceeded 800 billion yuan, and by May 20, it had jumped from 716.8 billion to 860 billion yuan in less than three weeks. By June 1, however, it seemed to fall back below the 800 billion yuan mark.

Looking back, the impact of these fluctuations is twofold. On one hand, the overall rise of chip stocks and the booming AI industry provide some valuation support for Cambrian. Solid performance data has convinced the market that Cambrian has transitioned from a money-burning R&D phase to a virtuous cycle of profitability and self-sufficiency.

On the other hand, doubts about Cambrian's stability persist. Every stock price surge is accompanied by questions of a 'bubble,' with netizens discussing these concerns after each major decline. This back-and-forth emotional tug-of-war reflects investors' fear of missing out on the next domestic NVIDIA while worrying about becoming bag-holders—a contradictory mindset that inevitably exists.

Typically, capital markets act as amplifiers of expectations. Once an industry is in the spotlight, funds tend to price in a decade's worth of growth into current stock prices.

However, this premature euphoria is eventually tempered by reality. Cambrian's rollercoaster market performance essentially reflects the market's oscillation between irrational exuberance and rationality—and, in truth, represents the inevitable path for China's domestic AI chip industry from speculative hype to value investing.

02 The rationale behind gains and the dilemma of declines

A deeper analysis reveals that Cambrian's market cap fluctuations stem from a tug-of-war between high valuations, real-world growth rates, and competitive dynamics. In the short term, AI computing demand remains robust, but unsustainable high growth, market share erosion, and a return to rational valuations are likely trends. In the medium to long term, success hinges on technological breakthroughs, ecosystem development, and customer expansion.

Specifically, the previous surge had inherent logic.

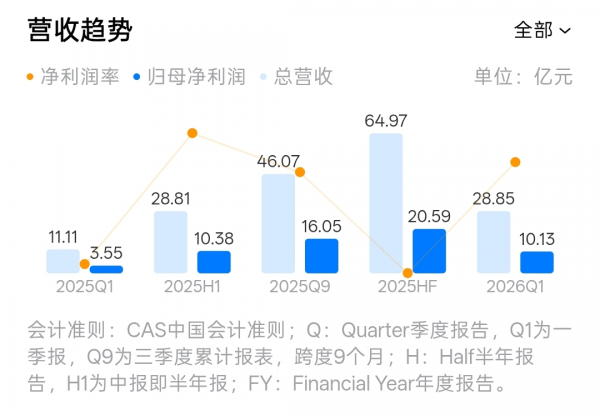

The most direct support came from explosive revenue growth. In Q1 2026, Cambrian reported 2.885 billion yuan in revenue, up 159% year-over-year, with net profit reaching 1.013 billion yuan, up 185% year-over-year. Operating cash flow turned positive for the first time at 834 million yuan. Objectively, this stellar performance reflects a concentrated release of demand for domestically controlled AI chips amid import substitution trends.

With global AI capital expenditures reaching $700–800 billion, domestic cloud providers and AI computing centers have ramped up procurement of domestic chips amid external technology blockades. As one of China's earliest AI chip pioneers, Cambrian naturally became a major beneficiary. Its orders are now booked through 2027, with advance payments and contract liabilities surging—jumping nearly 400 million yuan in a single quarter. This underscores strong downstream restocking demand, high order visibility, and extreme demand certainty.

Another supporting factor is improved product competitiveness. Cambrian adheres to a full-stack self-research approach, forming a 'cloud-edge-device' product matrix. Its flagship product, the MLU590, uses a 7nm process and delivers 512 TOPS of INT8 peak performance, rivaling NVIDIA's A10. In February 2026, Cambrian unveiled its next-gen HNLPU architecture, further fueling market hopes of catching up to international leaders.

However, when sentiment fades, issues are magnified. The foremost question is whether valuations are truly excessive.

In August 2025, economist Ma Guangyuan noted that Cambrian's P/E ratio exceeded 4,000x, while NVIDIA's was just 57x. Even now, Cambrian's forward P/E exceeds 260x, far above the semiconductor industry's ~60x average. Based on 2025 net profit of 2.059 billion yuan, its market cap-to-profit ratio exceeds 400x.

While market valuations are inherently subjective, the real concern is whether the company can justify these lofty figures.

In terms of growth, Cambrian's momentum has slowed. In Q4 2025, revenue hit 1.89 billion yuan, up 9.4% quarter-over-quarter, but net profit fell 19.8% quarter-over-quarter to 455 million yuan—the second consecutive quarterly decline (Q3 2025 saw a 17% drop). This suggests that after rapid growth, Cambrian is entering a period of volatility and adjustment.

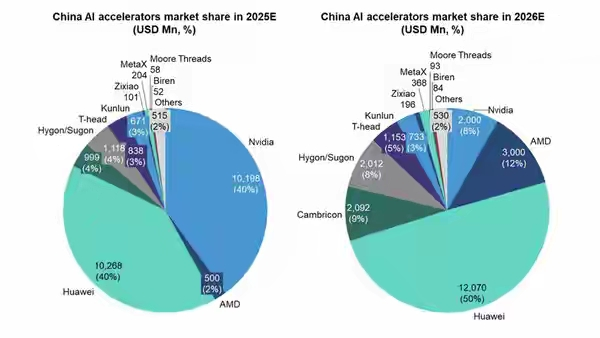

Shifting focus to the market, Huawei Ascend's rise is reshaping China's AI chip landscape. According to IDC and multiple investment banks, Huawei will capture 50% of China's AI chip market in 2026, with AMD taking 12% for second place and Cambrian likely third.

Critically, Huawei boasts a complete software-hardware ecosystem and strong customer resources, with leading enterprises likely placing large orders.

Meanwhile, NVIDIA is not standing still.

Despite export controls, NVIDIA still dominates the global high-end AI chip market and has consolidated its position through price cuts and specialized chips. In high-end training chips, the gap between Cambrian and NVIDIA remains wide.

Simply put, all industries follow a similar pattern: initial hype and bubble inflation, followed by a post-bubble correction and value rediscovery. Cambrian's rise reflects both era-driven opportunities and its own strengths, while its decline embodies multifaceted market forces.

03 Will domestic chips follow the mobile internet era's 'big fish eat small fish' dynamic?

China's AI chip industry now stands at a critical juncture. As the market matures, competition will intensify, and industry consolidation is inevitable. The future domestic chip market may mirror the mobile internet era's consolidation.

The first risk is escalating intense domestic competition. Beyond Huawei Ascend and Cambrian, dozens of firms—including Moore Threads, Biren, Enflame, T-Head, Hygon, and Kunlunxin—are competing in the AI chip space.

These companies have distinct strengths: some excel in general-purpose computing, T-Head leverages Alibaba Cloud's stable customer base, and niche players focus on high-end training chips. A price war has already begun to erode industry profits.

The second risk is overreliance on a single business line.

Take Cambrian: nearly all its revenue comes from cloud-based AI chips (99.3% in 2024, 99.7% in 2025). This single-business dependency weakens risk resistance. Moreover, its top five clients accounted for 92.36%, 94.63%, and 88.66% of revenue in the past three years, respectively, indicating high customer concentration.

If the computing market cools or industry demand weakens, Cambrian will face significant pressure. In contrast, Huawei offers a diversified portfolio—including Ascend AI chips, Kunpeng server chips, and Kirin mobile chips—mitigating risk.

Ecosystem development also poses risks. NVIDIA's success stems not just from chip performance but from its CUDA ecosystem, which supports millions of developers and has created a powerful network effect over a decade. New entrants face an uphill battle.

Cambrian is building its NeuWare software stack but lags far behind CUDA. A weak developer ecosystem could undermine market adoption and customer loyalty.

Cambrian faces two paths: emulate NVIDIA by accelerating its software ecosystem to create hardware-software synergy, or follow Huawei's model of full-stack technical capabilities and a complete industrial chain—even redefining semiconductor industry rules through sheer strength.

Neither path is easy. Building an ecosystem requires massive investment and time, while full-stack expertise demands long-term technical accumulation and talent.

During the mobile internet era, hundreds of smartphone makers emerged, but only Huawei, Xiaomi, OPPO, and Vivo survived. The AI chip industry will follow suit.

Lu Jiu Business Review predicts that over the next 3–5 years, China's AI chip market will undergo a brutal shakeout, potentially eliminating many firms. Companies without core technologies or reliant on hype will fall first, followed by those with flawed technical roadmaps or broken capital chains. Ultimately, only 2–3 truly capable firms may remain.

Of course, a rational capital market correction isn't necessarily bad for the industry. It will burst bubbles and direct funds to companies with genuine technology, products, and profitability. As a pioneer in domestic AI chips, Cambrian boasts deep technical expertise and first-mover advantages, but its challenges and doubts remain significant.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle