Director Cashes Out 232 Million, Why Is the Stock Price of This Optical Enterprise 'Unbreakable'?

03/02 2026

03/02 2026

749

749

On March 2, Lante Optics announced that the share reduction plan by director Mr. Wang Fangli had expired, with a cumulative reduction of 6.031 million shares, cashing out approximately 232 million yuan. As of the market close that day, the company's stock price closed at 53.35 yuan, down 0.73%.

From a traditional market perspective, significant share reductions by major shareholders are often seen as a bearish signal. However, today, Lante Optics' stock saw nearly 500 million yuan in trading volume throughout the day, with a turnover rate exceeding 2%, a cumulative increase of 10.16% over the past five trading days, and a year-to-date surge of 38.61%.

On one hand, the director is 'securing profits,' while on the other, there is sustained capital attention and mid-term strength. This seemingly contradictory phenomenon precisely reflects the shift in industrial logic.

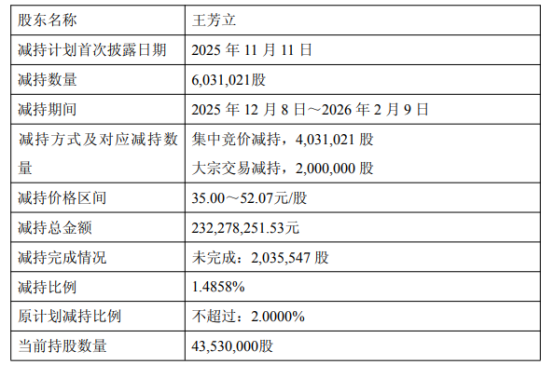

The announcement revealed that the share reduction was carried out by director Mr. Wang Fangli, who held 12.2880% of the company's shares before the reduction, making him a significant shareholder. The reduction period spanned from December 8, 2025, to February 9, 2026, with a total of 6,031,021 shares reduced through centralized bidding and block trades, accounting for 1.4858% of the company's total share capital, cashing out approximately 232 million yuan. The reduction price range was 35.00 yuan to 52.07 yuan per share. After the reduction, Mr. Wang Fangli still holds 43,530,000 shares, representing 10.7244% of the company's total share capital.

The announcement clearly stated the reason for the reduction as 'personal financial needs,' and the entire reduction process complied with laws and regulations, consistent with the previously disclosed plan. Based on the data, this was a compliant, transparent, and pre-announced reduction. However, what truly interests industry insiders is the timing of the reduction—from December 2025 to February 2026, which coincides with a critical period of qualitative change in Lante Optics' fundamentals and industry landscape.

Why did the market not react strongly to this reduction, and why did the stock price generally trend upward during the reduction period? The answer first lies in the company's performance. Just last week, Lante Optics released its 2025 preliminary performance report, showing a total operating revenue of 1.536 billion yuan, up 48.52% year-on-year; net profit attributable to shareholders of 388 million yuan, up 76.09% year-on-year; and core net profit of 379 million yuan, up 75.93% year-on-year.

More notably, the growth drivers were dissected, revealing rapid growth across all three major business lines. Lante Optics is no longer just a consumer electronics supplier but is deeply involved in four high-growth sectors: consumer electronics, automotive electronics, optical communications, and AR. This 'multi-pronged' business structure provides the company with strong performance resilience. (For details, please refer to 'First Preliminary Performance Report! Lante Optics' 2025 Net Profit Surges 76%')

Beyond strong performance, ongoing industry transformations are also supporting the long-term trend of the stock price. 2026 is widely recognized as the first year of CPO's large-scale deployment. Technologically, TSMC's COUPE platform has officially entered the CoWoS packaging mass production stage, integrating optical engines with switching chips, reducing signal transmission distance by 70%, and cutting power consumption by 30%.

Among industry giants, NVIDIA's Rubin platform and Broadcom's high-end switches have fully embraced CPO. NVIDIA has explicitly stated its plan to launch the second-generation Spectrum-X platform in 2026, adopting a 'deep co-packaging' form where optical engines are directly soldered onto the substrate.

Today, CPO concepts rallied against the market trend, with T&S Electronics rising over 10%, Kaige Precision Machinery hitting a 20cm daily limit, and Robotech reaching a historic high. On the news front, research firm LightCounting raised its forecasts for 800G and 1.6T optical module shipments—800G module shipments are expected to more than double in 2026, while 1.6T module shipments will grow from a small base in 2025 to tens of millions of ports. For optical industry practitioners, this means the demand ceiling for upstream optical components has been thoroughly (completely) opened.

Additionally, silicon photonics technology is transitioning from an 'optional' to a 'standard' feature in 2026, with the silicon photonics industry scale expected to exceed 3.5 billion US dollars, growing at a compound annual rate of over 27%. More importantly, silicon photonics technology is breaking beyond the data communication sector and massively diffusing into FMCW LiDAR, optical computing chips, and consumer-grade sensors.

In the silicon photonics foundry sector, a fierce battle for capacity has erupted. Tower plans to increase its silicon photonics wafer monthly capacity by more than fivefold by Q4 2026 compared to the same period in 2025, with over 70% of its capacity through 2028 already booked by customers. After acquiring AMF, GlobalFoundries has become the world's largest pure silicon photonics chip foundry by revenue.

Returning to Lante Optics' share reduction, the market is not ignoring the reduction but is trading on industrial trends. Lante Optics is not just a consumer electronics supplier but also one of the 'shovel sellers' for AI computing infrastructure. CITIC Securities recently pointed out in a report that the explosion in AI computing demand is driving upgrades in the optical communications industry, with overseas cloud providers continuously expanding their capital expenditures, confirming strong demand for AI infrastructure and driving robust demand for high-speed optical modules. For optical component manufacturers upstream in the supply chain, this represents a golden window of rising volumes and prices.

Today's slight decline in the stock price is more influenced by overall market adjustments and short-term sector rotations, representing a normal technical correction. The stock has risen over 10% in the past five days and nearly 40% year-to-date, with today's trading volume still approaching 500 million yuan, indicating that market attention has not diminished due to the share reduction.

Lante Optics' case actually raises a thought-provoking question for the entire optical industry: As industrial logic shifts from the consumer electronics cycle to the AI computing cycle, how should the value coordinates of optical enterprises be reassessed?

In the CPO era, industry chain value is shifting from traditional module assembly to upstream silicon photonics chips, advanced packaging, and core optical components. Companies with manufacturing capabilities in core optical components such as glass aspherical lenses and glass wafers are seeing their strategic value reassessed.

For optical devices in the 1.6T era, success no longer hinges solely on 'higher bandwidth' but on repeatable manufacturing, predictable yields, and large-scale supply capabilities. For companies like Lante Optics with deep accumulation in optical cold processing and precision molding, this represents a core competitive advantage.

As 'optical replacing copper' transitions from a slogan to an inevitable physical law, optical components are no longer supporting actors in electronic devices but the foundation determining the interconnection efficiency of AI computing clusters. The depth of optoelectronic integration is becoming a key indicator of industrial competitiveness.

Overall, Lante Optics' director cashing out 232 million yuan while the stock price reached a phased (phased) high during the reduction period, and although it experienced a slight callback (pullback) with the market today, its mid-term upward trend remains intact. This seemingly anomalous phenomenon is driven by the resonance (resonance) between the company's performance release and industry cycle.

In the face of the massive wave of industrial cycles, the short-term impact of a single event is being diluted. What determines corporate value is no longer the entry or exit of a particular shareholder but the company's position in the new coordinate system of the industry chain. The share reduction plan has expired, but the upward cycle of the optical industry has just begun.

-

On the Eve of Its IPO, Avatr Finds Itself Embroiled in a 'Farce of Controversy and Belittlement'

-

![]()

Yutong Optics' Japanese Subsidiary Unveiled in Tokyo, Shifting Strategic Focus to Technology-Driven Growth

-

![]()

Half-Year Revenue Outstrips Last Year’s Total! Zhongrun Optics Forecasts 80.2% H1 Revenue Growth

-

![]()

Why Does AI Competition Start with Computing Power?

-

![]()

Apple AI Finally Makes Its Debut in China, Yet iPhone's 'AI Autonomy' Faces Uncertainty

-

![]()

Apple AI and QianWen Make Up Lessons: Alibaba Has Its Own 'Doubao Phone'

-

![]()

QianWen Joins Apple, Signal for Large Models to ‘Fade into the Background’

-

![]()

The ‘Anchor’ Strategy of Google Hidden Behind the Bleeding Financial Report