1.5 Billion Trapped for 6 Years? OFILM's Restructuring Faces Critical Juncture

05/21 2026

05/21 2026

616

616

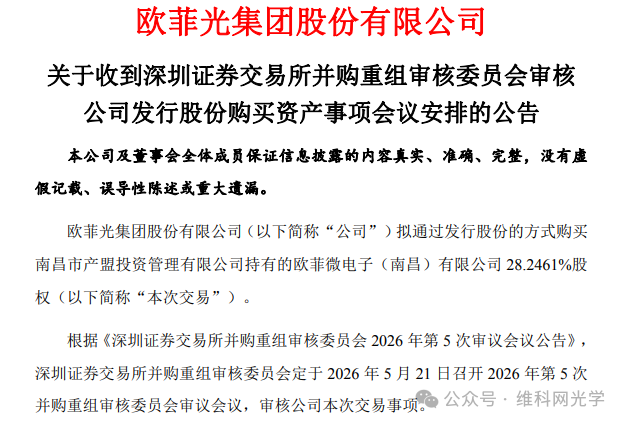

On May 21, the Merger and Acquisition Restructuring Review Committee of the Shenzhen Stock Exchange held its 5th meeting in 2026 to review OFILM's issuance of shares to purchase assets. As of press time, the review results had not yet been announced, but the market had already cast a "no" vote with real money.

On May 19, OFILM closed at RMB 8.91 per share, a 16.18% inversion from the issuance price of RMB 10.63 per share; on May 21, the day of the meeting, its share price fell further to RMB 8.64, widening the discount to approximately 18.7%.

Among A-share cases under review for issuing shares to purchase assets, OFILM and Wuhan Holdings, which just announced the termination of its restructuring, are rare examples of share price inversion. After nearly 15 months, Wuhan Holdings announced the termination of its acquisition on May 19, citing "changes in the external environment and relevant circumstances."

With this recent precedent, whether OFILM's restructuring review can smoothly (Note: ' smoothly ' is kept as pinyin here due to its common usage in financial contexts to imply smooth approval, but for strict translation, it could be 'pass smoothly') pass smoothly remains uncertain. OFILM's current predicament can be glimpsed from the evolution of its restructuring plan.

From the initial plan to acquire minority stakes in two subsidiaries, OFILM Microelectronics and Jiangxi Jinghao Optics, along with RMB 800 million in matching (Note: ' matching ' is translated as 'accompanying' financing for context, but 'supporting' could also fit) accompanying financing, to the cancellation of the Jiangxi Jinghao acquisition and accompanying fundraising in February 2026, and then to the forced submission of an extended evaluation on May 6 due to an expired assessment report—the valuation of 100% of the target company, OFILM Microelectronics, was reduced by 18.3% from RMB 6.34 billion to RMB 5.18 billion, with the transaction price dropping from RMB 1.791 billion to RMB 1.463 billion.

Notably, the counterparty, Nanchang Industrial Alliance, invested RMB 1.5 billion in OFILM Microelectronics in 2019, only to receive a transaction consideration of RMB 1.463 billion six years later, all paid in deeply inverted OFILM shares.

This means that if the restructuring is completed, Nanchang Industrial Alliance will suffer a principal loss (approximately 2.5%) and six years of funding costs, not to mention the current unrealized losses on its shares. Rather than a "state-owned asset exit," this appears to be a stop-loss exit forced by changes in the target asset's fundamentals.

Moreover, OFILM's fundamentals represent the biggest risk exposure in this restructuring. In 2024, the company's net profit attributable to shareholders was RMB 58.3818 million, superficially achieving a "turnaround," but its core net profit remained negative at RMB -12.7211 million. Government subsidies of approximately RMB 63.5 million include, count, enter into (Note: ' include, count, enter into ' is translated as 'recorded' in this context) recorded in current profits, along with value-added tax credits, were the main sources of the "turnaround"—clearly insufficient for sustainable profitability.

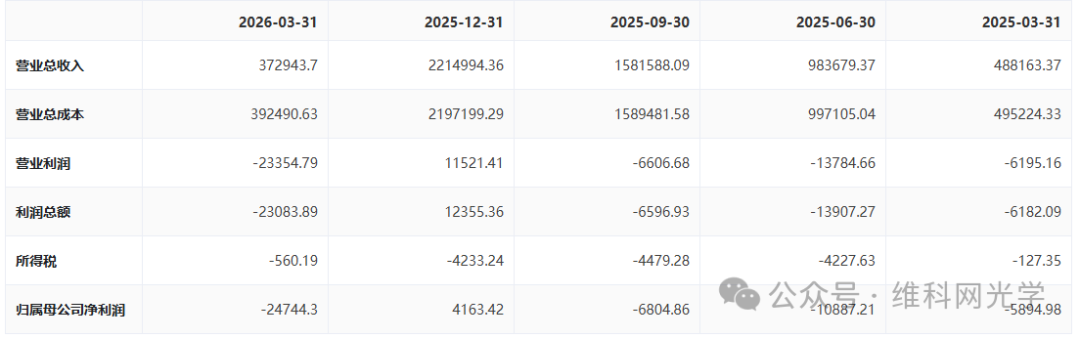

Entering 2026, OFILM's fundamentals deteriorated rapidly: Q1 revenue reached RMB 3.729 billion, a 23.60% year-on-year decline; net profit attributable to shareholders plunged by 319.75% to a loss of RMB 247 million; Q1 gross margin shrank to just 7.37%. The asset-liability ratio climbed to 75.07%, with short-term borrowings and non-current liabilities due within one year totaling approximately RMB 6.269 billion, while cash on hand stood at only RMB 1.985 billion, indicating an extremely fragile financial structure.

Now, let's examine the true quality of the target company, OFILM Microelectronics. According to financial data disclosed in the restructuring report, its net profit attributable to shareholders declined significantly in 2025, forming a stark contrast with previous profit peaks. The evaluation agency proactively reduced the 2026 profit forecast by approximately 43% in the extended evaluation. Even with the target's valuation reduced from RMB 6.34 billion to RMB 5.18 billion, corresponding to the adjusted 2026 forecasted net profit, the price-to-earnings ratio remains as high as approximately 25 times.

Against the backdrop of IDC's forecast that global smartphone shipments will decline by 12.9% year-on-year in 2026, putting pressure on demand for fingerprint recognition and 3D sensing modules, the reasonableness of this valuation is clearly controversial. It should be noted that OFILM Microelectronics holds over 46% of the global market share in ultrasonic fingerprint recognition modules, possessing certain technological moats, which is one reason the evaluation agency still assigned a relatively high valuation.

Even with the valuation significantly reduced, the current share price well below the issuance price still subjects the counterparty to unrealized loss pressure. If forced to proceed, Nanchang Industrial Alliance's book losses will be confirmed, potentially facing pressure on state-owned asset preservation and appreciation; if the restructuring is terminated, its illiquid stake in OFILM Microelectronics will also face disposal risks.

Caught in this dilemma, the path forward is uncertain. The market has already voted with its feet: on May 20, OFILM saw net outflows of principal funds exceeding RMB 110 million, with cumulative net outflows over the past five days exceeding RMB 200 million.

Overall, OFILM's issues extend far beyond capital-layer restructuring, lying instead in the fundamental failure of its core business competitiveness and financial structure. Regardless of whether the May 21 review result is "approval" or "rejection," OFILM will struggle to escape this systemic crisis.

With Wuhan Holdings' restructuring termination still fresh in memory, OFILM's capital predicament may just be unfolding.

-

![]()

Personnel Shuffle: Independent Director Mi Xuming Steps Down from OFILM

-

![]()

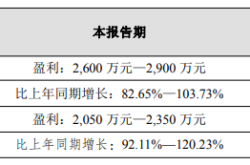

Net Profit Anticipated to Skyrocket by 103%: What Gives This Optical Company a Competitive Edge?

-

In Just One Year, China Unveils Unicorns Valued at 10 Trillion Yuan!

-

![]()

6 Park Companies Shine at WAIC: How Hong Kong Science Park Bridges AI from Research to Industry

-

![]()

Wang Wenjing’s Third Act: Can Yonyou Reinvent Itself in the AI Era?

-

![]()

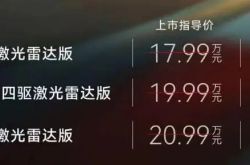

Performance Coupe Entry Threshold Reduced to 170,000 Yuan: Assessing the 2027 Exeed ES's Prospects

-

![]()

Battery "Crisis" for 4 Million New Energy Commercial Vehicles

-

【Focus】Fluorinated Photosensitive Polyimide (FPSPI): A High-End Subdivision of PSPI with Great Potential in High-Tech Industries