Is Adobe Facing a Decline or Being Impacted by Figma?

08/14 2025

08/14 2025

592

592

Many US stocks in AI applications have witnessed substantial bull runs, with companies like APP, Palantir, and META significantly benefiting from the AI wave. However, the journey for some AI application giants has not been smooth sailing.

Text-to-image technology has matured significantly, dramatically enhancing the efficiency of visual design. Yet, Adobe, the juggernaut in visual design software, finds itself in a tight spot. Its market value has halved against the backdrop of a 40% surge in the Nasdaq over the past two years. Palantir, with a revenue of $4 billion, now boasts a market value three times that of Adobe, which has a revenue of $20 billion.

Adobe, once the gold standard for SaaS, now sports a PE ratio of just 20. With the listing of Figma, whose acquisition by Adobe previously fell through, and its market value doubling compared to the acquisition valuation, Adobe appears even more beleaguered.

In the realm of image design, Canva is closing the gap with AI-generated images. Although Adobe has introduced its own Firefly, revenues from Midjourney and others are actually comparable. Various large models also offer text-to-image services, making it challenging for Adobe to maintain its leadership in this function.

Moreover, breakthroughs in text-to-video technology are imminent. Following Google's Genie3, more innovations will emerge, significantly enhancing video creation efficiency. While AI-generated videos still require professional software for refinement, like AI-generated paintings, Adobe's functionality has subtly diminished. Since Adobe did not pioneer these text-to-image and text-to-video technologies, it finds itself playing catch-up in the fast-paced technological race of the industry.

Adobe may not necessarily be in freefall, but given its continued performance growth and no significant customer loss so far, there are still opportunities for investors to scoop up shares at the bottom. Assuming text-to-image and text-to-video functions eventually become mainstream, Adobe's lag may not be a critical issue. Based on its niche in professional secondary editing, even if other companies can handle large models, they may not necessarily excel in professional visual design functions. Thus, Adobe can still maintain a prominent position in the industry.

However, beyond this scenario, what other hidden dangers does Adobe face?

1. Compromised Long-Term Valuation Logic

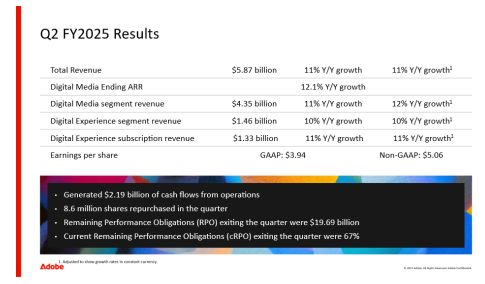

In terms of performance, Adobe is not as impressive as other popular AI companies. However, its growth rate is not a major concern. In Q1 2025, both revenue and remaining performance obligations (RPO) maintained growth of around 11%. Many SaaS companies not closely tied to AI are actually experiencing decelerating growth.

The company has also slightly increased its full-year performance forecast.

In terms of growth, the media design business outperformed the digital business. The media design business includes visual design software such as PS, PR, and PDF reader Acrobat. The digital business refers to the company's web design software Experience.

The company noted that although Firefly, its AI drawing function, does not generate high revenue, it has a high penetration rate, with 78% of users utilizing it. This indicates that generative AI has become a rigid demand for visual design. With Adobe's position, integrating this function into PS does not create a significant gap with external competitors. Since Firefly does not have a high fee, customers do not necessarily need to use two software, such as Midjourney followed by PS.

Companies providing text-to-image services also lack robust secondary graphic design and editing functions. In commercial applications, it is nearly impossible to complete a project solely with text-to-image; detailed adjustments are crucial in the final stages.

The company implies that Firefly is not lagging but is quite popular. With such high user stickiness and potential, if priced similarly to PS in the future, revenue could surge. However, optimism in this regard should not be overstated. After all, everyone is currently offering it for free, and Adobe's products are not sufficiently superior to warrant a significant price increase. Simultaneously, other companies are striving to enhance their secondary editing and fine-tuning capabilities in text-to-image functions to boost usability and product commercialization. Until the technology and final workflow paradigm in the text-to-image industry stabilize, the fear of market share decline will continue to haunt Adobe for an extended period.

Small companies aim to gain market share, thus boosting their valuation. Conversely, Adobe faces the expectation of losing market share, suppressing its valuation. This naturally creates an imbalance in the stock market. However, for large-scale companies that have long dominated an industry, this situation is indeed harsh.

Adobe's PDF reader Acrobat has also been AI-enhanced, significantly improving its functionality. However, this has not translated into revenue growth as other large models can handle PDF tasks without charging a fee.

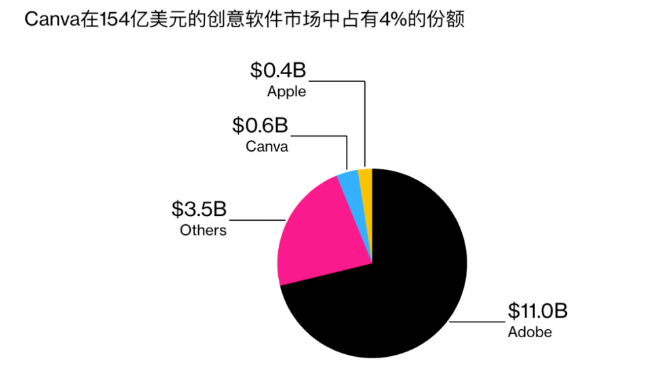

It cannot be overlooked that Canva, a competitor that gained prominence in professional image design rather than text-to-image functionality, continues to maintain a higher growth rate. In 2024, its market share was 1/20 of Adobe's, but in 2025, it continued to maintain a growth rate of 30%, indicating that Canva's market share is still growing rapidly.

Although Canva's professionalism is naturally inferior to Adobe's, the problem is that many commercial visual design needs are also mostly unprofessional. Compared to Adobe, Canva offers a lighter operating environment and is easier to use. Simultaneously, it also boasts quality AI production tools. In the long run, Canva will be Adobe's biggest competitor. Before the convergence of their growth rate differences, this is likely to be a new factor suppressing Adobe's valuation.

Interestingly, after Figma's listing, its share price soared, and Canva may follow suit soon, leading to a bubble contagion phenomenon. For instance, Figma's peak market value reached $60 billion, while Canva's performance is comparable to Figma's, and its indicators are almost three times better. Using the same valuation method, it would not be difficult for Canva's market value to reach $200 billion upon listing. However, the issue is that Adobe's current market value is only $140 billion.

This reflects the current frenzy of the US stock market bull run. However, it also indicates that Adobe has become quite cost-effective in the long run. There are only two factors suppressing its valuation. But as long as its market share does not decline and its growth rate does not lag further behind Canva's, with the disclosure of quarterly results, Adobe's valuation can easily return from 20 to its long-term level of 30 times.

2. The Battle with Figma is Not the Focus

Turning to the popular Figma, claiming that it will comprehensively impact Adobe is somewhat exaggerated due to the huge size disparity. However, Figma did indeed capture Adobe's XD software, dominating the web or program UI design segment.

This segment is a subset of visual design and is not large. Figma's innovation lies in its platform operation that does not require locally installed software but runs on the web and emphasizes collaborative processes among multiple users. In contrast, Adobe's XD is somewhat more complex.

Figma's real competitiveness lies in generating code from graphics, enabling the construction of a webpage by solely designing images and logic, thereby completing tasks without coding. Traditional design still requires coding first and then loading materials. Therefore, Adobe's XD appears somewhat outdated, and now XD has essentially given up competition.

However, losing in this segment is not critical since Adobe has a diverse portfolio of other businesses. Web UI design is essentially light visual design and does not require the extensive functions derived from PS. What is more crucial is for this tool to be user-friendly.

Adobe once hoped to acquire Figma for $20 billion, but obviously, another monopoly would not be approved due to antitrust concerns. Theoretically, Adobe's offer was quite sincere.

Currently, Figma's impact on the UI design segment is complete, and it will be difficult for Figma to further seize other software functions from Adobe. After all, under the competition from Canva and Figma, many non-professional visual design businesses have already been captured.

At the same time, Figma is not without concerns. This lightweight, no-code website development tool has given rise to more innovative companies with the development of large models. For example, Lovable, a no-code website building tool, has seen its ARR growth rate rank among the top in all SaaS companies just one year after its establishment.

Compared to Figma, Lovable may not be as strong in visual design, but its coding capabilities are superior. It emphasizes creating webpages with a single sentence of text, even skipping the visual design step of images, making Figma appear somewhat cumbersome. This logic is similar to when other companies challenge Adobe: for general users who are not very professional, being slightly easier to use can make a significant difference. It seems that the new generation is pushing the old aside, and Figma's future also faces considerable challenges.

3. The Real Issue

For Adobe, the primary issue at present is insufficient growth rate, both in revenue and profit. Unfavorable competition has contributed to this problem, but it is not sudden unfavorable competition. Rather, it stems from Adobe's inability, as a large company, to maintain market share while also charging high fees and profits in those innovative, low-professional segments.

However, the US stock market is not lacking in the performance of large companies this year. Monopoly or excessive size is not a reason for no growth. The key is how to leverage AI to drive revenue and profit growth. If Adobe's growth rate recovers to above 20%, its takeoff is inevitable.

Like other current AI application companies, Adobe spends considerable money on computing power but has not translated this into growth. One reason is that its customer base has not increased. Referring to the development of Figma and Canva, Adobe has been losing mass-market customers. In this regard, the company's long-term growth depends on maintaining a stable number of professional users and increasing ASP through coordinated sales to generate revenue.

This is essentially the company's implied expectation mentioned above for Firefly to increase fees subsequently and for AI video functions to be charged. However, this path will only become narrower, allowing competitors to thrive and have more motivation to explore professional businesses. Therefore, Adobe still needs some changes, such as exploring better pricing models:

In the past, the transition from software licensing to SaaS subscription payment was a major innovation in the software industry. However, in the AI era, subscription is not the only option. With more refined AI monitoring, pricing can be based on the depth and time of operations, precisely differentiating between professional and non-professional users. Large models do not need to be paid by the day but by tokens, which is a form of refined pricing. Refined pricing based on the usage frequency of different software functions can actually rejuvenate Adobe, whose path is becoming narrower.

I once mentioned that successful AI application companies all have their own exclusive and powerful small models. This is true for Palantir, Applovin, and even Meta, which, despite seemingly focusing on large models every day, relies on the optimization of advertising business efficiency to boost revenue and profit, essentially using precise advertising small models, similar to Applovin. For Adobe, since its team cannot lead in AIGC models, it can only win by precisely pricing such models. For functions that everyone has, it should not be expected to maintain high pricing and high market share.

Additionally, it is worth noting that Adobe's profit margin has not improved in this wave. While the gross margin is already high and cannot be changed significantly, the sales and marketing expense ratio remains high. It is crucial to use AI to enhance sales efficiency, as Meta has been able to achieve revenue growth while reducing sales and marketing expenses. This internal control is unrelated to industry technology trends, indicating that Adobe has not deeply integrated AI internally, which may be the company's true future challenge.

Conclusion

For Adobe, with a market value of $140 billion, multiplying its value is not impossible, and there are precedents. However, the problem is that the company's level of AI integration is insufficient, and its AIGC technology is not at the forefront of the industry. But its accumulated expertise in professional secondary editing functions gives it a significant fault tolerance rate. As long as it can identify some exclusive small models, whether in products or internal controls, it can stage a comeback.

For instance, accurate product pricing or enhancing product marketing efficiency could swiftly reverse the trajectory of revenue and profit growth. Nevertheless, the current reality is that this has yet to be achieved, consequently leading to a continued suppression of its valuation until the text-to-image and text-to-video models are firmly established. Adobe remains a company that cannot undergo a significant transformation without implementing change.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?