The Bubble Theory Emerges: Will AI Still Have a Future in 2026?

11/25 2025

11/25 2025

508

508

The market was initially declining amid concerns over liquidity drains caused by the US government shutdown and supply chain financing worries surrounding OpenAI. However, with the US government now reopened and Nvidia reporting robust earnings, the market remains unresponsive.

What exactly is wrong with the US stock market? Will the remaining five weeks of 2025 be nothing but wasted time? Will AI still have a future in 2026?

"

I. What Are Trump's Key Demands for 2026?

There is one last opportunity for an interest rate cut this year—the December 10th policy meeting. From a macro perspective, the market's short-term sentiment seems to be dominated once again by expectations of interest rate cuts. Thus, when Federal Reserve officials continuously send mixed signals, the market enters a phase of 'internal conflict.'

However, if we consider next year's US midterm elections and the country's long-term strategic development, two fundamental needs become clear:

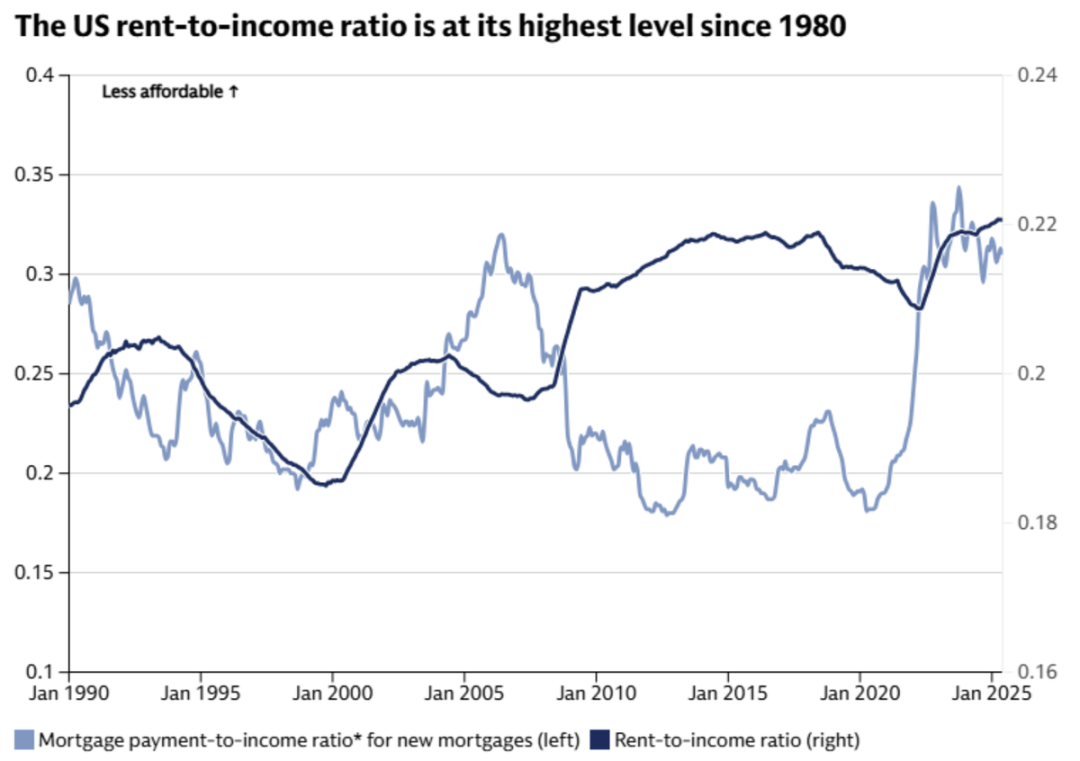

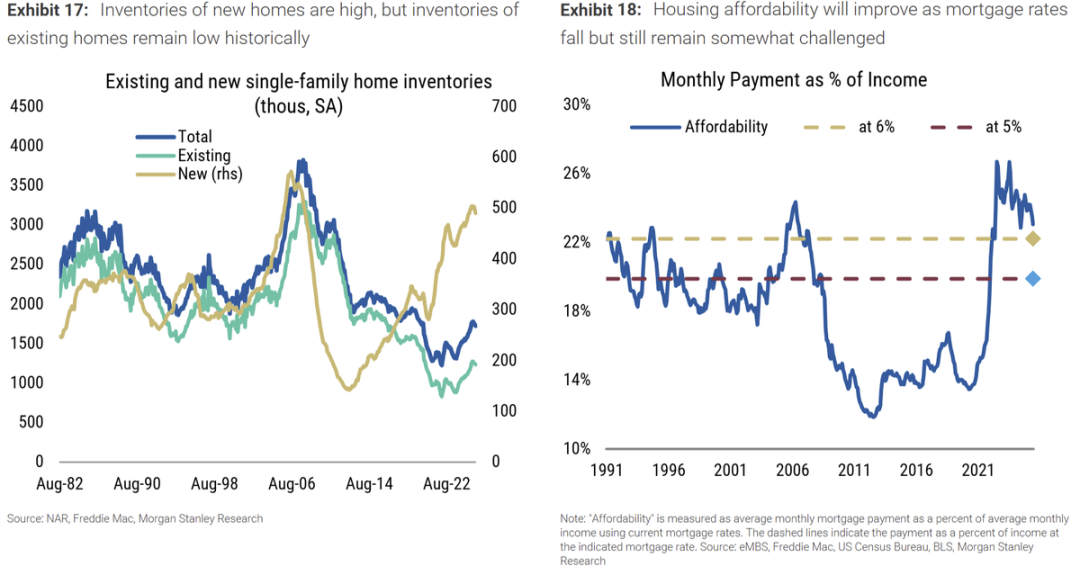

a. Immediate Real-World Issue: Inflation, Specifically, the Need to Reduce Rental Costs Through Interest Rate Cuts

Among various household expenses, rent and mortgages represent the largest share. Currently, monthly rent as a percentage of monthly income has reached a near-record high, accounting for 22% of disposable income. In this context, a slowdown in price growth and households' ability to bear costs are two distinct matters.

"

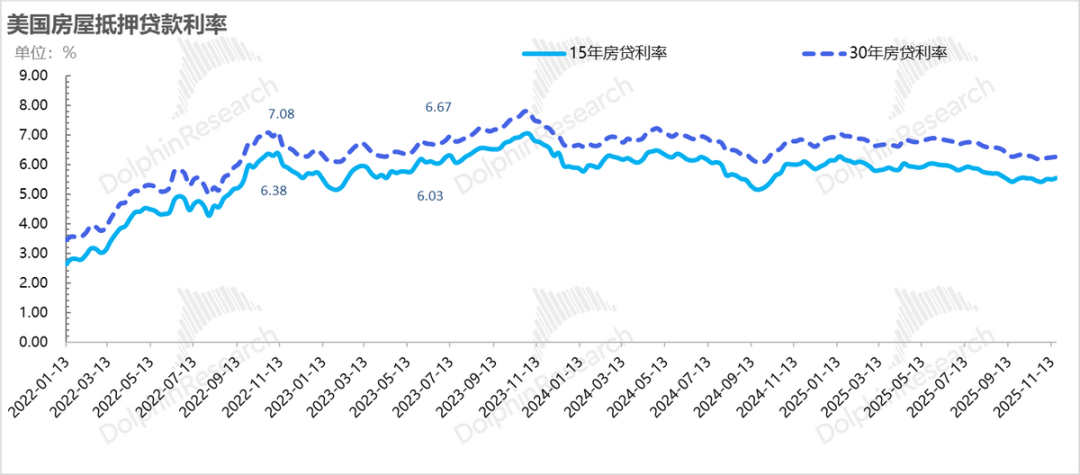

High housing prices and soaring mortgage rates have jointly driven up mortgage and rental costs. In the short term, the key to improving rental affordability lies in lowering mortgage rates through interest rate cuts. Currently, US mortgage interest rates stand above 5.5%, and rate cuts could effectively reduce rental and mortgage costs.

"

"

Take the election of New York's new mayor as an example. His core policy platform, in Dolphin Research's view, represents 'administrative intervention' in prices—freezing rents, providing free public transportation, and establishing government-run grocery stores.

Trump's policies have also become noticeably more pragmatic:

1) Patching up the trade war: Eliminating tariffs on certain categories crucial to core prices, such as agricultural products and fertilizers.

2) Applying maximum pressure to resolve the Russia-Ukraine conflict and stabilize energy prices.

These measures, which fundamentally aim to control prices, will likely continue through the 2026 midterm elections.

b. The Long-Term Economic Horizon: AI Requires Cheap Capital for Financing

As of the end of 2025, among the companies observed by Dolphin Research, US AI capital expenditures have largely been supported by equity financing and cash reserves. Only a few new cloud companies or those with unhealthy balance sheets have resorted to debt financing for capital expenditures.

However, by 2026, US tech giants will begin announcing bond financings, and with a series of off-balance-sheet debt arrangements by these companies, the market will increasingly see cases where AI capital expenditures are supported by debt financing.

During this period of high private capital expenditures, if interest costs remain elevated, the return risk of these capital expenditures will also rise. From a strategic development perspective, during the high-density investment phase of AI infrastructure, the US needs cheap capital to support large-scale AI infrastructure advancement.

Combining these two issues, the US government has a strong incentive to push for interest rate cuts in both the short and long term.

II. Is the Decision to Cut or Not Cut Interest Rates in December Truly Critical?

c. Federal Reserve Candidates: Will There Be a More Fiscal-Service-Oriented Fed?

Current Federal Reserve Chair Powell's term expires in May next year, requiring a successor. Trump's two core requirements for candidates—'loyalty + growth'—aim to complement fiscal easing.

The search for alternatives is primarily being led by Treasury Secretary Besent, with the candidate pool narrowed down to five individuals. Notably, the highest probability candidate, Hassett, and the lowest probability candidate, Michelle Bowman, are both seen as more dovish than Powell.

d. Looking Ahead to Next Year: Is It Suitable to Cut Interest Rates?

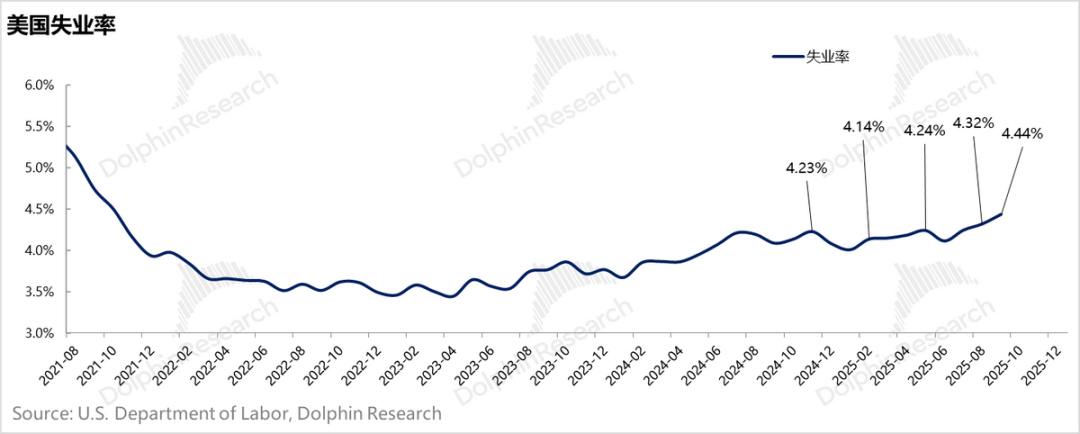

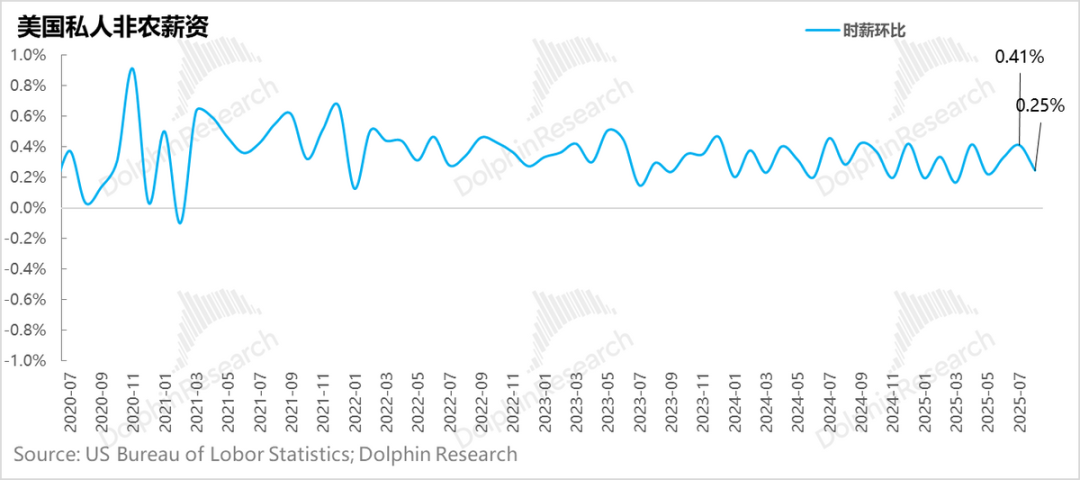

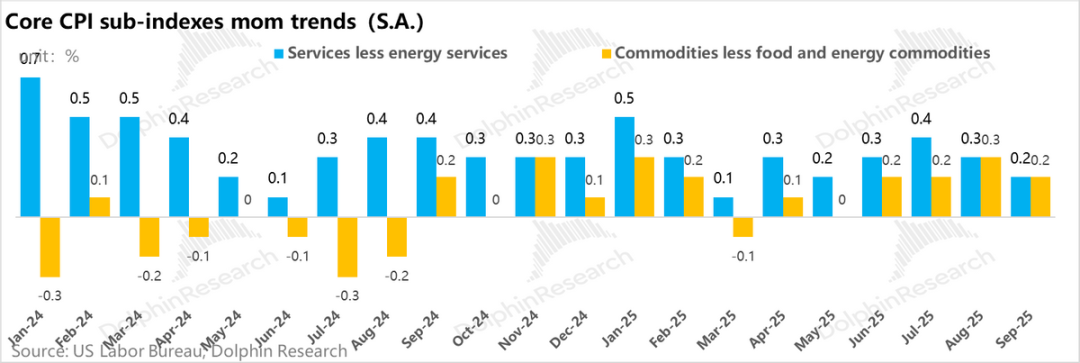

Key macroeconomic data is still missing, but from the released employment and inflation figures, September's 120,000 nonfarm payrolls were not low, but the rise in labor force participation, downward revisions to previous employment figures, and the increase in unemployment (4.44%) indicate a weakening job market. Meanwhile, month-over-month wage growth remained stable at 0.2-0.4%, and core inflation held steady at 0.2%, showing decent performance.

Although these figures are somewhat outdated, they generally reflect a weak job market with diminished inflation risks.

"

"

"

Assuming US inflation (excluding tariff impacts) remains around 0.2% monthly, the annualized inflation rate would hover around 2.5%. The current policy rate stands at 3.75%-4%. From now until the end of 2026, a total reduction of 75 basis points seems feasible, with a maximum likely not exceeding 100 basis points.

The remaining question is the timing of these 75-100 basis point cuts: If a cut occurs in December, only two more cuts would be possible in 2026. If no cut happens in December, a cut is almost certain by late January 2026.

From the perspective of driving year-end consumer spending and economic growth, a December rate cut followed by no cut in January seems like a reasonable choice. However, even if no cut occurs in December, a rate cut is highly likely within a month or so after December 10th.

From the US government's policy standpoint, if no December rate cut occurs, dovish expectations for the 2026 rate cut pace could still be shaped by signaling potential Federal Reserve Chair candidates.

Given the current market correction, subsequent release of US fiscal funds, and gradual increase in fiscal stimulus in 2026, even if no December rate cut occurs, the situation appears more like a macro scenario where bad news has already been fully priced in.

III. Industrial Investment: Is the AI Bubble Still the Core Contradiction in Trading?

After addressing macro concerns, the pressing question from an industrial perspective remains whether current AI capital investment plans can match the potential value created by scenario penetration. In other words, is there an AI investment bubble? Are current AI valuations overly extrapolated?

Dolphin Research believes this question is difficult to answer definitively in the short term. Its value lies more in the discussion itself, as reflecting on this issue represents a return to rational investment thinking.

Despite the correction in AI valuations, the process of AI capital expenditures, in terms of current economic input, essentially represents a 'major reconstruction' of industrial infrastructure in the AI era—a process of re-industrialization of infrastructure.

Compared to concerns over job displacement during the mid-to-late stages of AI terminal scenario implementation, 2026 resembles the early stage of AI capital expenditure implementation and re-industrialization. Before AI replaces human labor, AI investments will first create a wave of infrastructure job demands. 2026 will likely be a year where AI infrastructure drives domestic demand and job creation.

Coupled with 2026 rate cuts and fiscal stimulus, US domestic demand should not face significant issues. During this process, it may instead represent a period of AI correction combined with valuation recovery in traditional industries.

In other words, for US stock investments in 2026, during the era of AI infrastructure investment, the AI supply chain requires valuation corrections to await the realization of terminal scenario value. However, the industrial reconstruction driven by AI will stimulate demand in traditional industries, boosting domestic demand and creating excess return opportunities for traditional companies outside the AI supply chain.

IV. Portfolio Returns

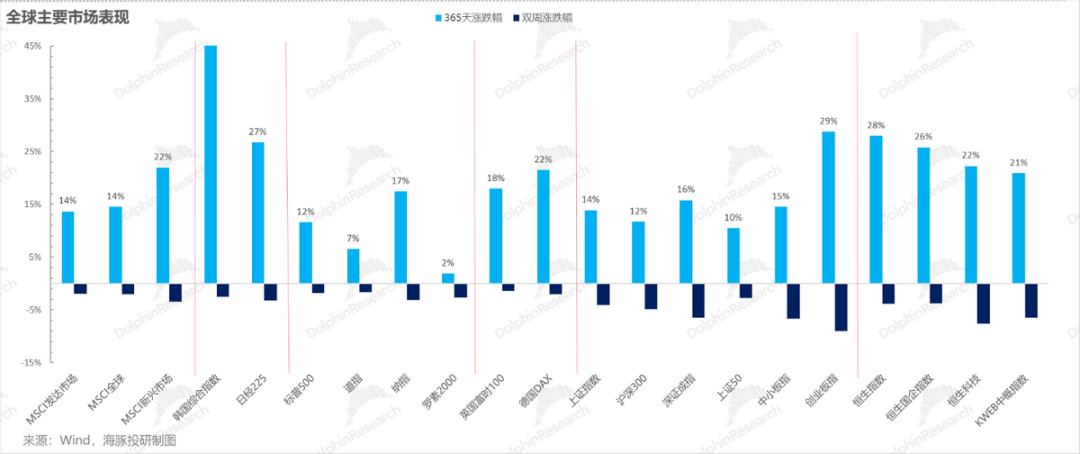

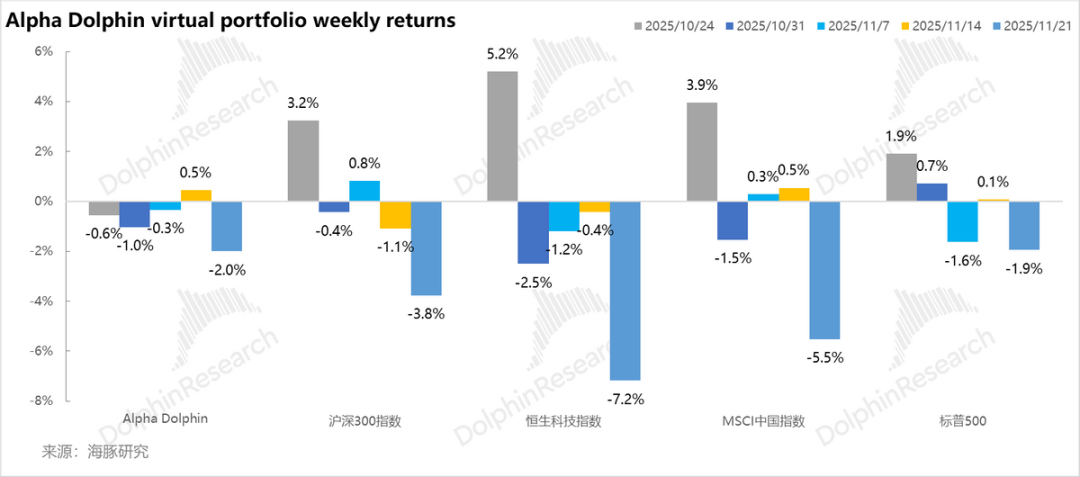

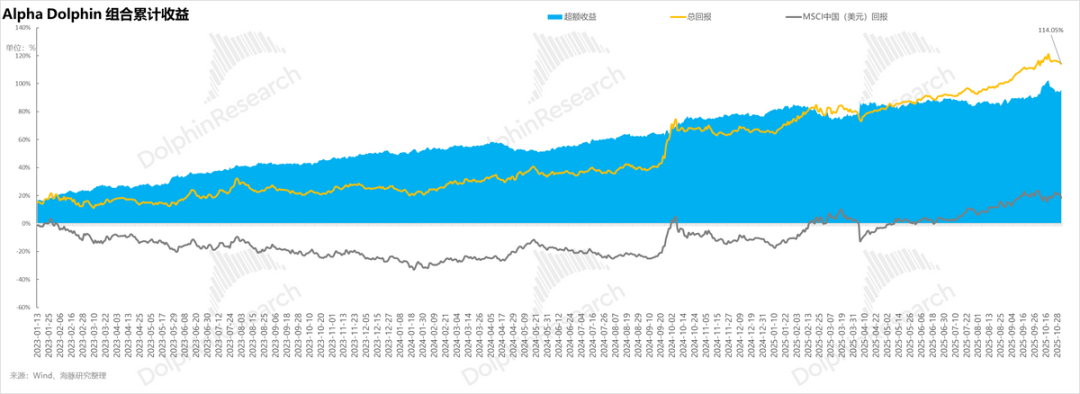

Last week, Dolphin Research's virtual portfolio, Alpha Dolphin, made no adjustments. It declined by 2% for the week, outperforming the CSI 300 (-3.8%), MSCI China Index (-5.5%), and Hang Seng Tech Index (-7.2%), but slightly underperforming the S&P 500 (-1.9%).

This was primarily due to the relatively risk-resistant nature of the portfolio's significant cash, gold, and US Treasury holdings during the market decline. However, Pinduoduo's earnings report, given its high weighting in the portfolio, somewhat dragged down performance.

"

Since the portfolio's inception for testing (March 25, 2022) through last weekend, the absolute return stands at 109%, with an excess return of 94% compared to the MSCI China Index. From a net asset value perspective, starting with an initial virtual asset base of $100 million, the portfolio exceeded $213 million by last weekend.

"

V. Individual Stock Gains and Losses Contributions

Last week, Alpha Dolphin declined alongside the broader market, with Pinduoduo experiencing a notable drop. Key explanations for individual stock performance are as follows:

"

VI. Portfolio Asset Allocation

The Alpha Dolphin virtual portfolio holds 18 individual stocks and equity ETFs, with 7 at standard weighting and the rest underweight. Assets outside equities are primarily distributed among gold, US Treasuries, and USD cash. Currently, the ratio between equity assets and defensive assets (gold/US Treasuries/cash) stands at approximately 55:45.

As of last weekend, the asset allocation and equity holding weights for Alpha Dolphin have been published in the Longbridge App under the 'Dynamic—Research' section in an article with the same title. Additionally, Dolphin Research's factual hot topic commentary and updates on major company events are prioritized for release on the Longbridge App rather than on public channels.

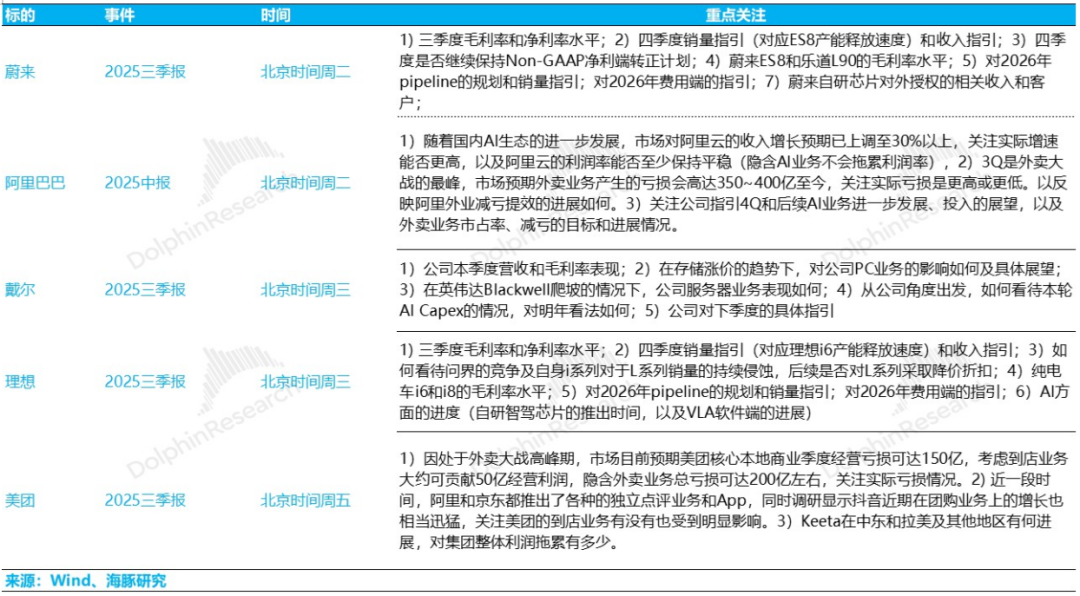

VII. Key Events Next Week

This week, the earnings season for Chinese concept stocks continues, with Alibaba, Meituan, and new energy vehicle companies releasing reports. The AI investment logic for Chinese concept stocks and outlook for new energy vehicles in 2026 warrant close attention:

"

- END -

// Reproduction Whitelisting

This article is an original piece by Dolphin Research. Authorization is required for reproduction.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, aimed at users of Dolphin Research and its affiliated institutions for general reading and data reference. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving the report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person using or referring to the content or information in this report for investment decisions assumes full risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from using the data in this report. The information and data in this report are based on publicly available sources and are intended for reference only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be regarded as or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to, nor are they intended for use in, jurisdictions where such distribution, publication, provision, or use would contravene applicable laws or regulations or result in Dolphin Research and/or its affiliates or associated companies being subject to any registration or licensing requirements in such jurisdictions, nor are they intended for citizens or residents of such jurisdictions.

This report merely reflects the personal viewpoints, insights, and analytical methods of the relevant authors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving