The autonomous driving track is quietly changing, with Robobus set to become the next hundred-billion-dollar sector.

12/25 2025

12/25 2025

487

487

In 2024, Pony.ai and WeRide successively went public on the U.S. stock market, marking what was seen as China's L4 autonomous driving commercialization 'breaking the ice.' However, the post-IPO glow faded quickly as financial reports revealed Robotaxi's 'four scars': high vehicle costs, low daily orders per autonomous vehicle, heavy reliance on policy windows, and a failing profitability model. By Q3 2025, Pony.ai's average daily orders per autonomous vehicle in a single city fell below 8, with operating margins still negative. WeRide, though 'quasi-commercialized' in some cities, faced costs exceeding three times those of regular ride-hailing services per kilometer.

As capital markets shift from 'tech euphoria' to rationality, another track is quietly heating up out of public view: autonomous buses (Robobus). From Pingshan, Shenzhen, to the Xiong'an New Area, and from Huangpu, Guangzhou, to the Suzhou Industrial Park, dozens of local governments are intensively promoting pilot programs for the normalized operation of L4 autonomous buses. Mushroom Autonomous, the world's only Robobus enterprise with 'L4 full-stack technology + city-level AI scheduling platform + commercialization on main roads in developed countries,' partnered with BYD in October this year to win Singapore's first L4 Robobus line, exporting China's solution overseas.

Amid the contrasting fortunes, the investment logic for autonomous driving has shifted: post-2026, the truly certain growth lies not in Robotaxi, still 'burning cash for validation,' but in Robobus, backed by policy support, high-frequency scenarios, and a clear business model. For cities, it represents an 'increment' in public services; for enterprises, a 'cash cow' with calculable returns; for capital, the shortest 'path to monetization' in the intelligent transportation dividend.

Robotaxi Dilemma: Advanced Technology ≠ Commercial Viability

Capital markets once viewed Robotaxi as the 'ultimate proving ground' for autonomous driving technology, but the IPO results of Pony.ai and WeRide exposed its commercial fragility. Data and deployment realities reveal at least three insurmountable gaps in Robotaxi's business model.

First is the limitation of 'per-vehicle profitability,' where scaling up triggers cost traps. Pony.ai claims to achieve RMB 299 in average daily revenue per autonomous vehicle in Guangzhou, seemingly covering costs. However, a breakdown reveals vulnerability: hardware depreciation for its seventh-generation Robotaxi relies on six-year amortization, insurance costs are 50% higher due to early safety records, and the 1:20 remote assistance staff-to-vehicle ratio remains unscaled. If the fleet expands from 1,000 to 3,000 vehicles (the 2026 target), hardware procurement, roadside infrastructure, and remote operation costs will grow exponentially—explaining why Pony.ai's net loss reached RMB 381.6 million in Q2 2025, and WeRide's hit RMB 406.4 million in the same period. In contrast, Robobus offers a clearer cost-reduction path: fixed routes reduce sensor calibration and algorithm iteration costs by 30–50% compared to Robotaxi, while automakers like BYD have slashed vehicle production costs by over 20% through economies of scale.

Second is the conflict between scenario complexity and policy adaptation. Robotaxi requires coverage of all urban open roads, facing 'corner cases' like pedestrians crossing, non-motorized vehicles cutting lanes, and extreme weather. Even Waymo, with 450,000 weekly orders in San Francisco, must navigate frequent regulatory adjustments by California's DMV. Chinese Robotaxi firms face policy lag: while Beijing, Shanghai, Guangzhou, and Shenzhen allow unmanned demonstration operations, road rights in core urban areas remain restricted, and accident liability, data security regulations are incomplete. Robobus, however, benefits from proactive policy support: Shenzhen's 2022 'Smart Connected Vehicle Management Regulations' provide end-to-end legislative backing, while Chengdu and Suzhou directly integrate Robobus into public transport plans. As scenarios expand from 'park microcirculation' to 'urban mainlines,' policies act as 'enablers' rather than 'regulators.'

Finally, there is the fundamental difference in demand nature: discretionary consumption versus rigid public services. Robotaxi is essentially a 'premium ride-hailing' service, chosen by users for 'novelty' rather than necessity, leaving it vulnerable in competition with traditional platforms like Didi and Gaode due to price disadvantages (Pony.ai's Robotaxi fares are ~1.5x higher than regular ride-hailing). Robobus, however, targets rigid public transport needs: Singapore views L4 Robobus as critical to alleviating bus driver shortages, while China faces a deficit of over 100,000 bus drivers in 2024. Robobus lines in Shenzhen and Chengdu directly address 'last-mile' commuting pain points, with user willingness to pay backed by governments or enterprises, ensuring far greater cash flow stability than C-end-dependent Robotaxi.

Robobus's Four Certainties: Policy, Scenarios, Business, and Rigid Demand

Compared to Robotaxi, autonomous buses demonstrate stronger commercial certainty across multiple dimensions. A literature review of 46 key studies from 2018–2024 in 'Implications of Autonomous Buses on Public Transit Systems' reveals:

1. Clear policy support and proactive local government promotion

As a vital part of public transport, bus automation aligns with policies like 'Smart Cities' and 'Green Transportation.' Local governments have launched autonomous bus pilot routes with targeted subsidies and road rights support. Germany, Singapore, and China have enacted regulations and road testing norms for autonomous buses, with institutional frameworks becoming increasingly defined.

2. Relatively closed scenarios for easier technology deployment

Buses typically operate on fixed routes, dedicated lanes, or within parks, where road conditions are simpler, reducing system complexity and risk. This enables shorter technology iteration cycles and easier safety redundancy implementation.

3. Clear business model: cost reduction and efficiency gains as value drivers

Public transport systems face long-standing challenges like driver shortages, rising labor costs, and low operational efficiency. Studies show autonomous buses can reduce operating costs by 50–60% (Bösch et al., 2018) while improving vehicle utilization and punctuality through intelligent scheduling. For governments and transit companies, this represents a 'calculable economic proposition.'

4. Strong public service attribute and higher social acceptance

As public service carriers, autonomous buses gain public trust more easily. Surveys show high passenger approval for their safety and environmental benefits, particularly in shuttle and microcirculation bus scenarios.

Data-Driven Future: The 'Calculable' Potential of Autonomous Buses

Projections and pilot data indicate:

Cost structure optimization: Labor costs, accounting for 30–40% of bus operation expenses, can be significantly reduced through automation;

Emission reductions: Electric autonomous buses can cut lifecycle carbon emissions by 47%;

Road capacity improvements: Dedicated lanes and coordinated scheduling can boost road throughput by 10–30%.

Behind these figures lies a quantifiable, replicable, and scalable business model.

Why Now is the Critical Juncture for Robobus Deployment?

Technology maturity: L4 autonomous driving is commercially viable in closed/semi-closed scenarios;

Policy windows open: Multiple regions are developing intelligent transport infrastructure, with buses as priority deployment carriers;

Validated business models: Cost reduction effects are evident, with clear government procurement and operational partnership models;

Significant societal benefits: Aligns with carbon neutrality, transportation equity, and aging-friendly goals.

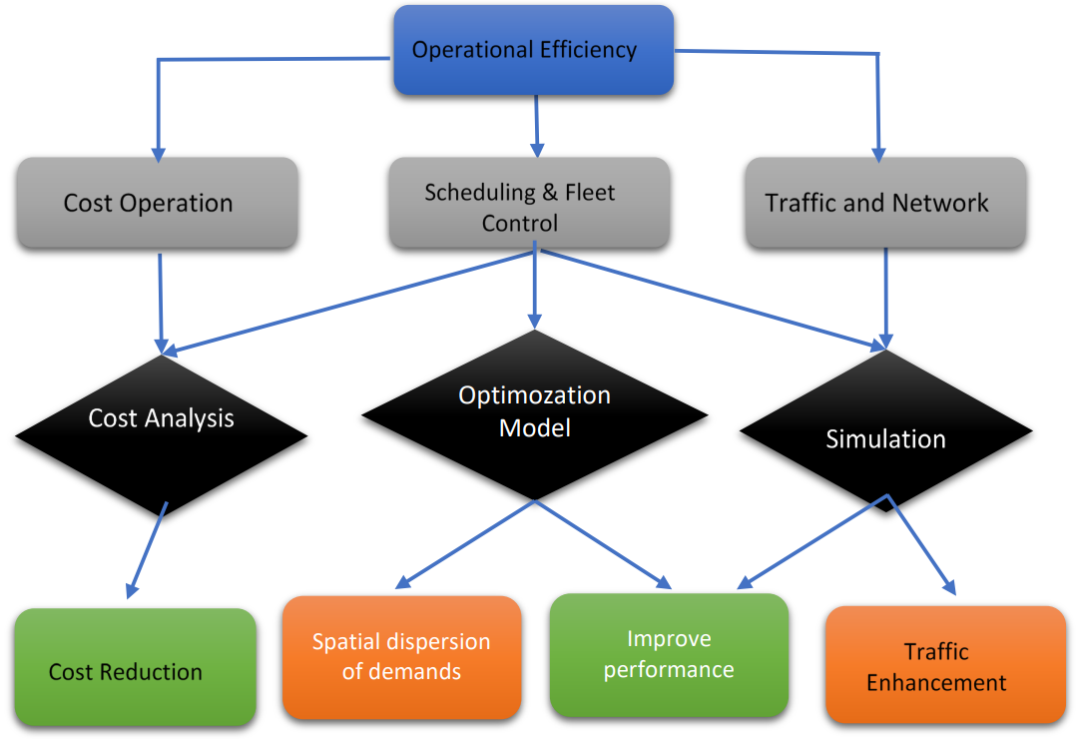

Meanwhile, the operational efficiency of autonomous buses spans multiple dimensions, including cost management, scheduling and fleet control, and traffic and network optimization. Common methods include cost modeling, optimization models, and simulation, with core objectives focused on optimizing fleet management, rational resource allocation, and reducing operational expenses. While economic benefits are anticipated (with potential cost reductions), research conclusions vary. It must be emphasized that the cost competitiveness of autonomous buses is not universal but scenario-dependent: in specific cases, their cost advantages surpass other transport modes like autonomous taxis, though flexible operation models may introduce issues like increased travel time and dispersed demand. Innovations like modular autonomous buses and demand-responsive passenger scheduling aim to drive efficiency revolutions. Achieving seamless integration requires refinement (precise) management of uncertainties and cost dynamics:

The Robotaxi narrative is glamorous, but Robobus offers a more solid business case. As tech hype fades, investors are returning to fundamentals: Who has customers? Who is profitable? Who is irreplaceable? While Pony.ai and WeRide struggle to scale Robotaxi profitability, the Robobus sector quietly achieves a 'quadruple resonance' of policy, scenarios, business models, and rigid demand. For markets, the key to evaluating an autonomous driving enterprise lies in its alignment with 'three matches': technological capability matching scenario complexity, business models matching paying entities, and growth pace matching policy rhythms—criteria Robobus firms meet more effectively.

The future autonomous driving track may belong not to Robotaxi players fixated on open roads, but to Robobus Builders who understand policy, public transport, and operations.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving