Zhipu’s Revenue Soars: MaaS Flywheel Fuels Growth in Scale and Pricing, Reinforcing the ‘Upper Bound of Intelligence’ Hypothesis

04/02 2026

04/02 2026

521

521

Author|Ren Tianqin

Editor|Chen Xiaoran

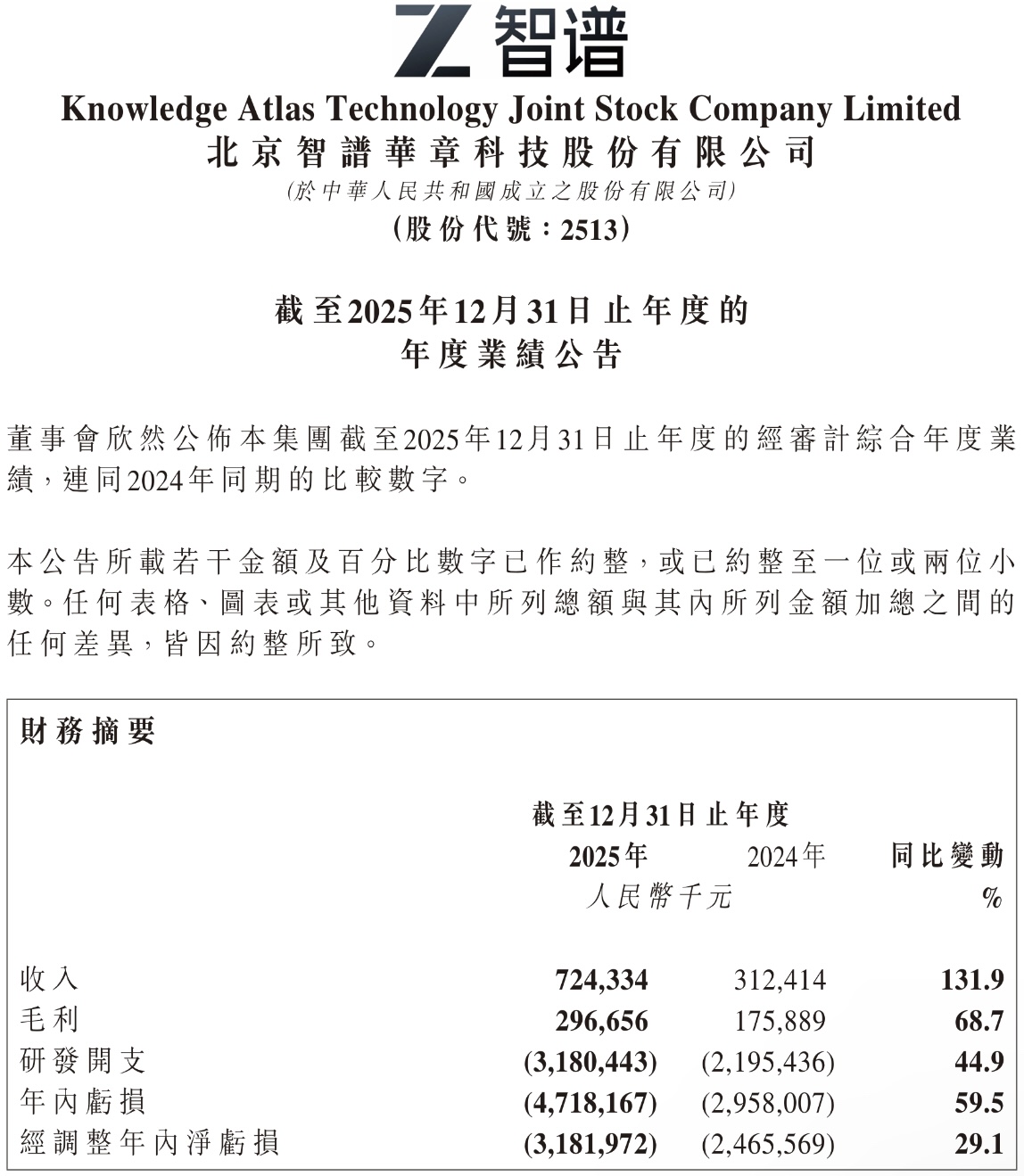

On March 31, Zhipu (2513.HK), hailed as the "world’s first large-model IPO," unveiled its inaugural full-year 2025 financial results post-listing, shattering the industry stereotype of "revenue growth without profitability" with a series of counterintuitive metrics.

Image Source: Zhipu Announcement

Revenue Soars

In 2025, Zhipu’s revenue surged to RMB 724 million, marking a 131.85% year-on-year increase and cementing its position as China’s top large-model revenue generator. Its gross margin stood at 40.96%, with the MaaS (Model-as-a-Service) platform’s margin skyrocketing nearly fivefold to 18.9%, becoming the cornerstone of profitability improvement.

The qualitative transformation in revenue structure was the standout feature of the financial report.

Cloud API revenue soared 292.6% year-on-year to RMB 190 million, with its share of total revenue jumping from 15.5% to 26.3%. Localized deployment revenue reached RMB 534 million, up 102.3%. The MaaS platform’s annualized recurring revenue (ARR) surged to approximately RMB 1.7 billion, a 60-fold increase over the past 12 months, fully replacing traditional businesses as the primary growth driver.

Customer diversification also improved. In 2025, revenue from the top client accounted for less than 10%, down sharply from 19% in 2024, enhancing risk resilience. By March 2026, platform registrations exceeded 4 million, spanning 218 countries and regions, signaling early success in global expansion.

Despite R&D investment reaching RMB 3.18 billion and a full-year net loss of RMB 4.718 billion, the R&D-to-revenue ratio narrowed from 7.0x to 4.4x, with R&D growth lagging behind revenue—a clear indicator of a profitability inflection point. Combined with IPO proceeds of HKD 4.516 billion, the company maintains robust short-term liquidity to fuel future expansion.

Growth in Scale and Pricing

Zhipu’s counter-cyclical growth stems from its strategic tenet: "The upper bound of intelligence determines pricing power, while Token scale determines value." As China’s closest equivalent to Anthropic, Zhipu adheres to a "foundation model + API services" approach, with over 80% of revenue derived from standardized API calls, aligning closely with the growth logic of global leaders.

Its product and technological prowess underpin this confidence.

In 2025, Zhipu rapidly iterated from GLM-4.5 to GLM-5-Turbo. GLM-5 scored 50 on the Artificial Analysis leaderboard, ranking fourth globally and first among open-source models, trailing only GPT, Claude, and Gemini. Its innovative Slime framework revolutionized reinforcement learning efficiency, while GLM-5 achieved full-stack compatibility with domestic chips, cutting inference costs by 50% and establishing dual barriers in "technology + computing power."

Commercially, Zhipu broke free from price wars. In Q1 2026, API prices rose 83% cumulatively, yet call volumes surged 400% against the trend, reflecting overwhelming market demand.

Core products saw explosive popularity: The GLM Coding Plan attracted 242,000 paying developers, with Token calls increasing 15-fold in six months. The Claw Plan gained 400,000 subscribers within 20 days of launch, validating the commercial potential of long-chain agent tasks.

On the client side, GLM-5 secured adoption from nine top internet firms—including ByteDance, Alibaba, and Tencent—within 24 hours of release. Nine of China’s top ten internet companies deeply integrated the model, showcasing high client retention and recognition.

TAC Reshapes Industry Standards

Zhipu’s ascent marks China’s large-model industry transitioning from "parameter races and price wars" to "value competition and productivity realization."

The company introduced Token Architecture Competence (TAC), defining AI productivity value as "intelligence call volume × intelligence quality × economic conversion efficiency," reshaping industry valuation logic. Future competition will hinge not on parameter scale but on transforming intelligence into economic growth.

The industry is undergoing profound change, with competition logic shifting. Enterprise clients increasingly pay for high-reliability, low-hallucination AI services, as evidenced by Zhipu’s ability to raise prices amid soaring demand—confirming value competition as the mainstream trend.

Technologically, continuous iteration drives the industry from lightweight ambient programming to industrial-grade agent engineering, with models’ long-task execution capabilities forming core competitive barriers.

Business models are also evolving, with standardized API services replacing traditional custom projects. Anthropic achieved 10x ARR growth annually, while Zhipu surged 60x, both validating the MaaS open model’s massive scaling potential and commercial value.

Market opportunities remain vast. Under import substitution policies, GLM-5’s deep compatibility with domestic chips grants it unique advantages in the trusted IT market.

Agent scenarios are exploding, with products like Claw Plan driving exponential Token consumption growth.

Globally, GLM models integrated into Google Vertex AI, AWS Bedrock, and other cloud services, topping OpenRouter’s paid model rankings and offering immense overseas growth potential.

In the 6G and AGI eras, foundation models will serve as infrastructure, unlocking sustained long-term value.

High R&D Pressure

Despite promising prospects, Zhipu faces multiple challenges. Financially, RMB 3.18 billion in annual R&D investment sustained losses, with the R&D-to-revenue ratio at 4.4x and a prolonged profitability timeline.

Gross margin declined from 56.3% in 2024 to 41.0% in 2025, primarily due to a shrinking share of high-margin localized businesses and a shift in computing procurement to service models, potentially suppressing margin recovery long-term.

The large-model tech race accelerates, with AGI paths still diverging. International giants like OpenAI and Anthropic maintain leads, while domestic players like ByteDance, Alibaba, and Tencent ramp up investments, intensifying competition.

If Zhipu fails to sustain technological leadership, its existing barriers may erode. Industry-wide challenges like model hallucinations and computing bottlenecks could also delay commercialization.

Moreover, agent scenarios remain nascent, requiring sustained cultivation of payment habits and business models. Whether the Claw Plan’s popularity translates into sustained Token consumption remains unproven.

The company acknowledges a "computing power gap," with supply constraints potentially limiting revenue growth and client retention.

Overall, Zhipu’s inaugural annual report proves that the large-model industry’s future lies not in price wars but in building intelligence boundaries through technology and securing pricing power through value. Its MaaS flywheel has launched—whether it can continuously push intelligence boundaries and navigate industry cycles will determine not just its fate but also the global competitiveness of China’s AI firms.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?