Toyota Beats Volkswagen for Six Consecutive Years: Are Fuel Cars the Right Choice?

04/02 2026

04/02 2026

499

499

Lead

Introduction

Defense wins championships.

Once upon a time, Volkswagen Group dominated the global automotive sales rankings with its robust product lineup and global presence, sweeping the market under the banner of "German precision engineering." Particularly in core regions like Europe and China, it consistently held top market shares, becoming the undisputed benchmark of the traditional fuel vehicle era.

However, this landscape was completely upended starting in 2020. Toyota, with its steady performance, defeated Volkswagen for six consecutive years, firmly holding onto the global sales crown in a textbook example of shifting fortunes.

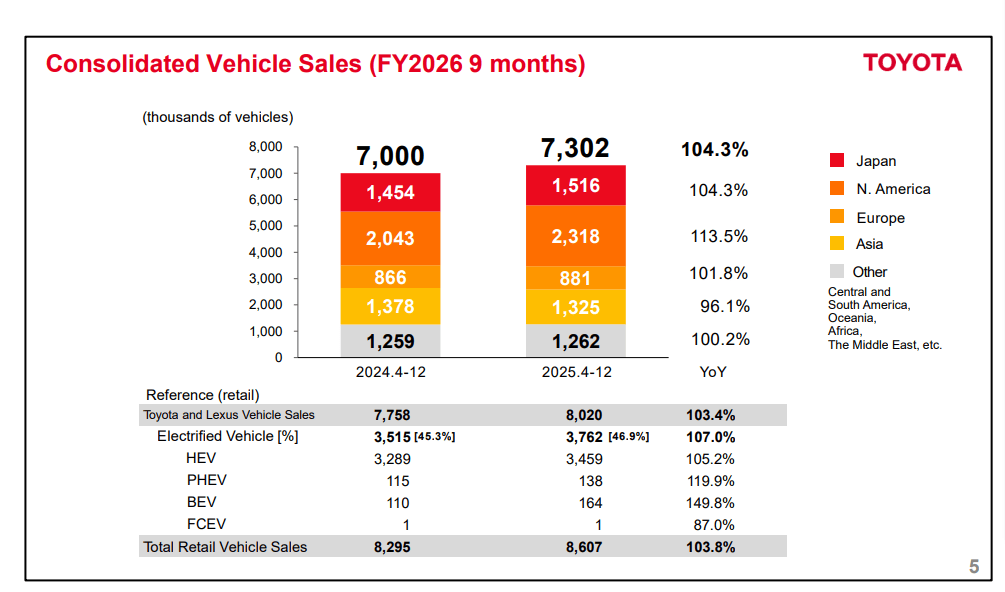

The 2025 global automotive market closing data once again confirmed this new reality. Volkswagen Group sold 8.98 million vehicles globally in 2025, securing second place but trailing Toyota for the sixth straight year. In contrast, Toyota sold 11.32 million units, extending its lead and retaining the championship title.

What is immediately apparent is that this six-year championship battle is no accident but a comprehensive reflection of the strategic choices, market adaptability, and pacing of new energy transitions between the two companies.

Notably, the speed of their new energy transitions appears to be a critical factor influencing their sales trajectories.

As the global automotive industry shifts toward electrification, Volkswagen opted for a more aggressive transition, early on investing heavily in pure electric vehicle (EV) technology and product iterations to seize the initiative in the new energy era. However, this transition came with growing pains. Resources were diverted from Volkswagen's fuel vehicle business, causing some market misalignments. Combined with global supply chain volatility and intensified regional competition, overall sales declined.

In contrast, Toyota adopted a conservative transition strategy, pursuing a multi-pronged approach of "fuel vehicles + hybrid + pure electric." It focused on deepening hybrid technology while slowly expanding its pure EV lineup. This cautious stance allowed Toyota to continue relying on its mature fuel and hybrid vehicle systems to stabilize its global market share, particularly in regions less receptive to electrification, where its products were more adaptable, ensuring sustained sales stability.

Additionally, Toyota's balanced global footprint, reputation for product reliability, and precise cost control have been key pillars supporting its six-year reign as sales champion. Volkswagen, meanwhile, was more affected by regional market fluctuations, such as declines in China and North America, leading to sales volatility.

Of course, this does not mean Volkswagen's aggressive transition was wrong or Toyota's conservative approach was right. Rather, these strategic differences have influenced their current performances to some extent. As for the longer-term future, the outcome remains uncertain.

01 Volkswagen Turns Left, Toyota Turns Right

Volkswagen and Toyota have charted divergent paths in the global and Chinese markets through vastly different transition strategies. Their technological investments, strategic planning, product performance, and market feedback reflect stark contrasts, directly impacting their sales, profits, and industry influence.

From Volkswagen's perspective, the core of its new energy transition is "aggressive investment and comprehensive layout (strategic deployment)." Globally, Volkswagen launched its "Roadmap E" strategy years ago, later upgrading it to the "2030 NEW AUTO" strategy, explicitly aiming to transform into a software-driven mobility services provider and become a global leader in pure EVs.

According to incomplete statistics, Volkswagen invested €150 billion from 2021 to 2025, with €73 billion allocated to electrification and digitization, accounting for 50% of total investment. It plans for pure EVs to comprise 50% of its lineup by 2030, with standard battery cells covering 80% of EV models, targeting a 50% reduction in battery costs.

At the product level, Volkswagen introduced its ID. series of pure EVs, covering compact and mid-size segments. In 2025, it delivered approximately 983,100 pure EVs globally, up 32% year-on-year, accounting for 10.9% of total sales. Nearly 750,000 units were delivered in Europe, becoming a key pillar of its new energy sales.

China, Volkswagen's most critical single market globally, saw an even more aggressive new energy transition. In 2025, Volkswagen implemented a "value-first" strategy, prioritizing localized R&D layout (deployment) despite sacrificing some sales volume. It planned to launch over 20 pure EV, plug-in hybrid, and extended-range models in China by 2026, equipped with L2++ advanced driving assistance to address intelligentization (intelligent) shortcomings.

However, Volkswagen's new energy models in China have yet to enter the top tier in competitiveness. In 2025, its Chinese market sales fell 8% year-on-year to 2.6938 million units, declining for the second consecutive year, primarily due to weak EV performance.

Nevertheless, Volkswagen's fuel vehicle business in China remains robust. In 2025, it delivered over 2.57 million fuel vehicles, capturing 22% of China's fuel vehicle market share, providing stable cash flow to support its new energy transition. Affected by transition investments and market volatility, Volkswagen Group's operating profit plummeted 53.5% year-on-year in 2025. However, growth in its new energy business solidified its global influence in the sector, laying the groundwork for long-term development.

Compared to Volkswagen's aggressiveness, Toyota's new energy transition has been "cautious, restrained, and multi-pronged."

Globally, Toyota adheres to a strategy of "not abandoning fuel vehicles, deepening hybrid technology, and slowly advancing pure EVs." Its new energy layout (deployment) prioritizes hybrid electric vehicles (HEVs), with a lagging pure EV (BEV) lineup.

In 2025, Toyota sold 4.9949 million new energy vehicles globally, up 10.2% year-on-year, with HEVs accounting for 88.8% of the total. Pure EVs sold just 199,100 units, less than 4% of the total, despite a 42.4% growth rate, far below Volkswagen's scale.

Technologically, Toyota focuses on deepening hybrid technology while limiting investments in pure EVs. Its strategic planning does not set aggressive pure EV sales targets but emphasizes multi-powertrain parallelism to suit regional market demands.

For example, in China, Toyota's transition remains slow. In 2025, it launched new pure EV models like the bZ3X and bZ5 while leveraging its hybrid advantages to achieve 1.7804 million units in sales, up 0.2% year-on-year, making it the only growing Japanese brand. However, its pure EV sales remain sluggish, failing to gain competitive traction.

Nevertheless, this cautious transition strategy has allowed Toyota to maintain stable sales and profits. In fiscal 2025, its net profit fell about 25% year-on-year but remained far better than aggressive transitioners like Volkswagen, consolidating its global influence through steady sales.

However, Toyota's lagging pure EV transition has raised market concerns about "missing the new energy opportunity," widening its influence gap with Volkswagen in global new energy markets, particularly in high-penetration regions like China and Europe, where its competitiveness continues to weaken.

02 Short-Term Gains vs. Long-Term Trends

The current global automotive market presents a paradox. In China, Volkswagen's rapid new energy transition has led to sales declines but accumulated new energy influence. Toyota's cautious approach has stabilized sales but left it lagging in new energy.

Globally, most countries and regions still have high acceptance of fuel vehicles, particularly in emerging markets like Southeast Asia, the Middle East, and Latin America, where fuel vehicles remain dominant. This makes it difficult for traditional automotive giants to abandon fuel vehicle dividends, leading to hesitant transition attitudes.

This market reality suggests that the more cautious a company is in electrification, the less sales pressure it faces, and the more stable its global performance becomes.

Toyota has leveraged this cautious strategy, relying on its fuel and hybrid vehicle advantages to sustain global sales leadership. In contrast, Volkswagen's aggressive transition, while securing early advantages in new energy, has led to sales declines and profit pressures due to short-term overinvestment and market misalignments.

In 2025, transnational (multinational) automakers like Stellantis and Ford wrote down massive asset impairments due to overestimating electrification speeds, slipping into losses. This has prompted more automakers to rethink transition pacing, further highlighting Toyota's short-term advantages.

Additionally, partial recoveries in global fuel vehicle markets, EU adjustments to its 2035 internal combustion engine ban, and China's policies stabilizing fuel vehicle consumption have made traditional automakers more hesitant to commit fully to transition. After all, fuel vehicle businesses remain the most stable cash flow and profit sources today, while new energy businesses struggle to achieve profitability in the short term.

However, we must recognize that short-term sales advantages do not equate to long-term development potential.

From industry trends, electrification and intelligence are irreversible global shifts. Environmental policies worldwide are tightening, and consumer preferences are gradually shifting toward new energy models. In core markets, new energy penetration rates continue to rise, steadily compressing fuel vehicle market space.

Volkswagen's aggressive transition, while enduring short-term sales and profit pressures, positions it for long-term competitiveness through investments in new energy R&D, product layout (deployment), and supply chain development. By 2030, full standard battery cell coverage, deepened localized R&D, and completed intelligentization (intelligent) technology upgrades will give Volkswagen an edge in future new energy competition. Its preserved fuel vehicle base will also provide sustained transition support.

Conversely, Toyota's current stability through cautious transition may prove short-lived. As global new energy markets expand, particularly in core regions like China and Europe, where new energy penetration rates rise, Toyota risks significant challenges if it fails to accelerate pure EV R&D and product layout (deployment). Despite launching a chief engineer system in China in 2025 and strengthening collaborations with Chinese tech firms to speed up transition, this passive "defensive counterattack" remains unproven in keeping pace with industry developments.

After six years of shifting fortunes, Volkswagen has ceded the current sales crown to Toyota, which now holds the market share lead. However, for these two traditional automotive giants, the current landscape is not the final outcome.

Future global automotive competition will ultimately hinge on new energy model competitiveness. Whoever achieves breakthroughs in electrification and intelligence will seize the initiative in industry development. The clash between Volkswagen's aggressiveness and Toyota's caution will continue to unfold, and the outcome of this battle will reshape the global automotive industry.

Editor-in-Chief: Cao Jiadong Editor: He Zengrong

THE END

-

![]()

Revenue and Net Profit of 20 Listed Domestic Automakers in Q1 2026

-

![]()

The Fading Frenzy for 'Lobster': OpenClaw Traffic Plummets, QClaw Nearly Vanishes

-

![]()

Three Paths for Computing Power Energy Storage: The Divergent Strategies of Kstar, Shoto, and Sungrow | Xinliu AIDC Column

-

![]()

Tencent Music Embraces Authenticity Amidst AI Surge

-

Hot Topic | The Advent of Computing Power Futures: A Redistribution of Pricing Influence in the AI Sector

-

![]()

China's New 'Rare Earth Moment' Emerges—This Time, It's Fiber Optics

-

![]()

Equal Strength at the Dinner Table: Understanding the New Industrial Landscape Between China and the U.S. Through a Banquet

-

![]()

The Attack of 618: Apple iPhone 17 Sees Price Drop, Why Did Huawei Enjoy 90 Sell Like Hotcakes Before?