To a Certain Extent, Resembling Anthropic is a Boon for Zhipu—For Now. But What Lies Ahead?

04/02 2026

04/02 2026

585

585

PART 01

"To some degree, being likened to Wanwan is a blessing." In Empresses in the Palace, when the Emperor is confronted by Zhen Huan about being a substitute for Chun Yuan, he remains as obstinate as ever. From that moment on, he loses the 1.0 version of the innocent and pure-hearted Zhen Huan.

For the large model company Zhipu, resembling Wanwan is currently a beneficial and harmless situation—an open secret in the industry.

On March 31, Zhipu released its full-year financial results for 2025, marking its first financial report since going public. Subsequently, CEO Zhang Peng made multiple references to Anthropic during the earnings call, emphasizing that the company's commercialization strategy closely aligns with Anthropic's.

His reasoning is sound: a growing proportion of MaaS (Model-as-a-Service) revenue, a focus on the enterprise-level API market, using coding as an entry point, and emphasizing that the upper limit of intelligence determines pricing power. Essentially, Zhipu is replicating Anthropic's model. The latter's revenue primarily comes from enterprise users, with over 80% achieved through APIs. Claude Code achieved an ARR (Annual Recurring Revenue) of $2.5 billion in just a few months.

The financial report highlights a key trend: Zhipu's transition from "heavy-delivery localized projects" to "asset-light cloud-based MaaS services."

The day after the financial report was released, Zhipu's stock price surged, with gains at one point exceeding 35%, and its market value briefly surpassing HK$400 billion, reaching a new high since its listing.

The impressive growth data in the financial report was undoubtedly a direct driver of the surge: full-year revenue increased by 131.9% year-on-year, MaaS platform ARR increased 60-fold year-on-year, and after an 83% API price hike, usage still grew by 400%—this last set of data was particularly flattering for Zhipu. Rising prices driving performance growth was once a privilege reserved for luxury brands like Chanel, LV, and Moutai during specific cycles. Zhipu has forcibly edged its way into the ranks of luxury brands.

But perhaps a more crucial reason is that capital markets desperately want a "Chinese version of Anthropic" story.

PART 02

Chun Yuan is the white moonlight in the Fourth Elder's heart: of noble birth, stunningly beautiful, exceptionally talented (her Flying Red Phoenix Dance could captivate the world), and utterly pure and kind.

Anthropic, which has yet to go public, is also the white moonlight for many investors.

It boasts over 300,000 enterprise clients, including over 500 major clients paying millions of dollars annually. Eight of the Fortune 10 are its clients. Enterprise client renewal rates exceed 90% (92% for major clients), with average contract terms of 1-3 years, and top clients typically signing 2-3-year deals. Claude Code is a productivity-revolutionizing product with astonishing ARR growth.

Management has already stated that the company will achieve profitability by 2028—in the AI market, where losses are widespread, this statement carries as much weight as the Fourth Elder's exclusive favor.

Although it lags behind OpenAI in scale on the consumer side, Anthropic's robust B-end business has given it a sufficiently deep moat.

As long as it avoids major mistakes, it will thrive.

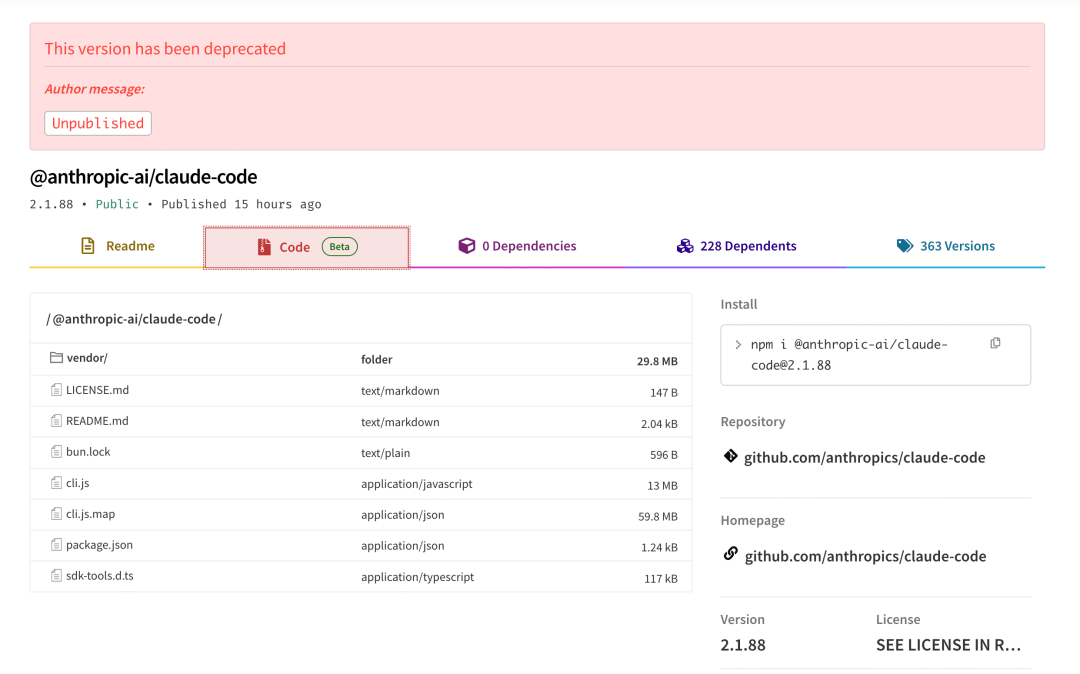

A recent counterexample is the "naked run" incident on March 31. Due to forgetting to exclude Source Map files, 512,000 lines of TypeScript code and over 1,900 source files were packaged into an npm installation package and "open-sourced" globally. This was equivalent to publicly revealing Claude Code's secrets to the world. Two similar leaks occurred within a week. Such rookie mistakes are catastrophic for Anthropic, which built its B-end market on "safety and caution."

Claude Code's recently released version 2.1.88 leaked 510,000 lines of source code.

But at this point in time, OpenAI and Anthropic remain highly coveted.

OpenAI just secured a $122 billion single-round funding, the largest in human history, with a post-money valuation of $852 billion. After completing a new $30 billion funding round in February 2026, Anthropic's valuation reached $380 billion—compared to the collectively plummeting "Magnificent Seven" U.S. stocks, which resemble Consort Jing, counting 326 bricks alone in the palace without favor.

Zhipu and MiniMax have reaped rewards by carrying the banners of "Chinese Anthropic" and "Chinese OpenAI," respectively. With these labels, they can secure valuation premiums and higher client trust far exceeding market averages without excessive explanation of their business logic.

Thus, in just three months from listing to April 1, 2026, Zhipu's and MiniMax's stock prices surged by 6.9x and 5.4x, respectively. Many investors slapped their thighs in regret, especially those who cleared their positions during the dark pool trading.

Xiaoyunzi (a loyal servant) is rare, but Kang Luhai (a fickle servant) is everywhere.

PART 03

After returning from Ganlu Temple, Zhen Huan no longer minded being a "Chun Yuan substitute" and instead used this identity to openly secure benefits for herself—Zhang Peng emphasizing Zhipu's goal of becoming the Chinese Anthropic follows a similar logic.

But Zhen Huan ultimately ascended to the pinnacle of harem power not by copying Chun Yuan's homework. She forged her own path with a tougher core than Chun Yuan's.

For Zhipu, it's clearly too early to talk about surpassing Anthropic. The bigger controversy now is: How similar is it to Anthropic?

Perhaps only 5-6 points out of 10.

First, revenue.

The revenue scales of the two companies are not even in the same league.

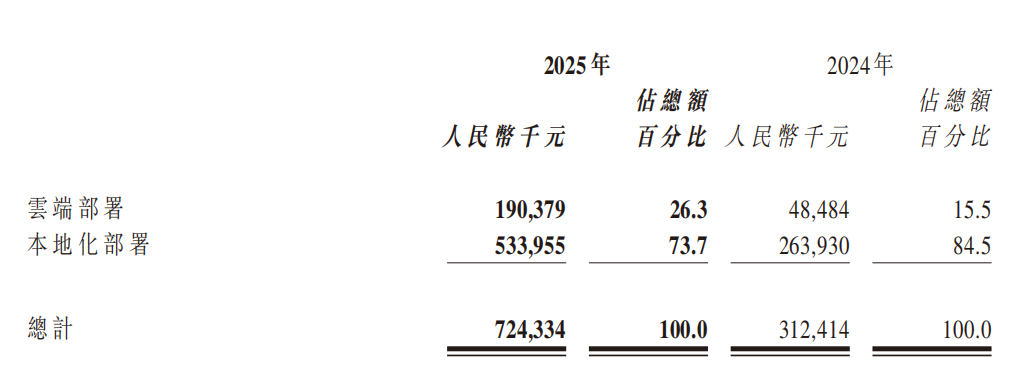

In 2025, Anthropic's full-year revenue was approximately $4.2-4.7 billion, with ARR reaching about $9 billion by year-end and surging to $19 billion by March 2026. Zhipu, on the other hand, reported full-year revenue of RMB 724 million, with MaaS platform ARR reaching about RMB 1.7 billion by March 2026.

This makes Zhipu's stock price more susceptible to bubble suspicions. Based on April 1 data, Zhipu's price-to-sales ratio is about 5-6 times that of Anthropic, meaning its high valuation is detached from company fundamentals and relies more on the "Chinese Anthropic" narrative and AI sentiment—much like how Zhen Huan initially gained favor because the Fourth Elder wanted to relive a romance with "Chun Yuan."

Next, revenue structure.

Zhipu's localized deployment accounted for about 74% in 2025, with cloud APIs at 26%. Anthropic, in contrast, is almost entirely cloud-based API services.

The biggest difference between the two models is that localized deployment often involves one-time project delivery—like begging for food, where you get a bowl when you ask and must ask again after eating. Cloud API services, however, rely on usage-based charging, akin to a long-term meal ticket.

Nevertheless, Zhipu is actively adjusting its structure. From 2022 to 2025, localized deployment's share dropped from 95% annually to 74%, while cloud API's share rose from 4.5% to 26.3%.

For Zhipu, this means it must maintain continuous leadership in model performance. Since cloud API services have low switching costs, clients can change providers anytime. Multiple AI entrepreneurs have noted that GLM5's performance still lags noticeably behind Claude's.

Finally, financial pressure.

The gap between Zhipu and Anthropic is even wider than the disparity between An Lingrong and Zhen Huan's family backgrounds.

In 2025, Zhipu's adjusted net loss was RMB 3.182 billion, up 29% year-on-year. R&D spending was RMB 3.18 billion, with an R&D expense ratio of 440%. Gross margin fell from 56.3% in 2024 to 41%. Profitability remains elusive.

In terms of cash, Zhipu held RMB 2.259 billion in cash and equivalents by the end of 2025—little changed from RMB 2.269 billion at the end of 2024, suggesting prudent financial management.

However, it raised about RMB 3 billion in funding in 2025, and total bank loans in current liabilities grew from RMB 137 million to RMB 605 million. Without external support, Zhipu would have faced significant financial pressure in 2025.

Of course, considering its IPO in January 2026, which raised about RMB 4.516 billion, and available bank financing of RMB 5.236 billion, Zhipu faces little short-term liquidity pressure.

But based on signals from Zhang Peng during the earnings call and intense industry competition around Agents and Tokens, burn rates in 2026 are likely to accelerate, leaving Zhipu in a tight financial position.

As one of the world's most cash-rich AI companies, money is the least of Anthropic's concerns.

It has raised over $46.5 billion in cumulative funding, with current cash reserves likely exceeding $30 billion. Public data shows that in 2025, Anthropic's full-year net cash burn was about $2.8-3 billion, but same-period revenue was about $4.2-4.7 billion—relatively healthy.

Entering 2026, with rapid growth in enterprise APIs and Claude Code, Anthropic's total spending is expected to surge to $18-22 billion, but revenue is projected to grow synchronously to $14-18 billion, with net cash burn of about $4-6 billion. According to official plans, it aims to achieve positive cash flow by 2027.

This is perhaps Zhipu's greatest pressure. It has chosen Anthropic's path and secured "favor" in the capital markets in advance, but in the money-burning game of large models, even Anthropic must prove to the market: This is a viable business, and I can make money.

Jinxi and Xiaoyunzi were willing to follow Zhen Huan not because she resembled Chun Yuan. First, it was their loyal nature; second, they saw promise in this consort's future in the palace. The same goes for Zhipu's investors.

Although unable to provide investors with a specific profitability timeline, Zhang Peng mentioned a formula during the earnings call: AGI commercial value = upper limit of intelligence * Token consumption scale.

In plain terms: The better your technology/experience, the more indispensable users find you, the larger the usage scale, and the higher the revenue.

This is also industry consensus. Amid the OpenClaw craze, Token consumption has surged, and the industry just experienced a collective price hike in March, with the highest increase reaching 463%. Zhipu's API prices rose 83%, yet usage grew 400%. This appears to validate the importance of the "upper limit of intelligence" in the formula.

However, the formula seems to overlook the complexity of Tokens, namely the cost per Token. Each Token consumed burns corresponding computing power. Whether Zhipu's price hikes can cover cost increases remains unconfirmed by official sources. More importantly, as Token economics become industry consensus, competition around them will intensify.

When pricing power is built on technological advantage, the latter's shelf life may shorten. The performance GLM5 sells today might be freely offered by DeepSeek or Qwen next week. How Zhipu can sustain its technological edge and ultimately turn it into a profitable business will determine its future imagination.

With inferior funding and revenue structure compared to Anthropic, Zhipu may also need to follow Zhen Huan's example and forge a unique, untrodden path for itself.

Of course, some core survival skills remain universal. For instance, always seize opportunities—or create them if none exist. Zhen Huan relied on this belief to leave Ganlu Temple, securing a future for herself, her unborn child, and her exiled family, ultimately delivering generous returns to her "shareholders."

We wish Zhipu well in moving beyond the "Chinese Anthropic" phase.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?