Zhipu Wants to Be China's Anthropic, But First It Needs to Answer One Question

04/08 2026

04/08 2026

406

406

By / Liang Tian

Source / Node AI

Zhipu has changed.

A year ago, Zhipu still called itself 'China's OpenAI.' After releasing its first financial report post-IPO, it shifted its narrative to becoming China's Anthropic.

The reason is simple.

The market no longer pays for AGI dreams. Investors care about how you make money. Anthropic sells APIs directly, making it easier to account for profits than OpenAI's consumer-side subscriptions. Zhipu chose this path to find a more credible valuation target.

To make its business model more understandable, Zhipu created two formulas: AGI Commercial Value = Intelligence Ceiling × Token Consumption Scale; TAC (Token Architecture Capability) = Intelligence Call Volume × Intelligence Quality × Economic Conversion Efficiency.

The formulas look good, and the story of China's Anthropic is compelling. But whether the financial data supports it requires a closer look.

Earn One, Lose Five

2025 was a transformative year for Zhipu.

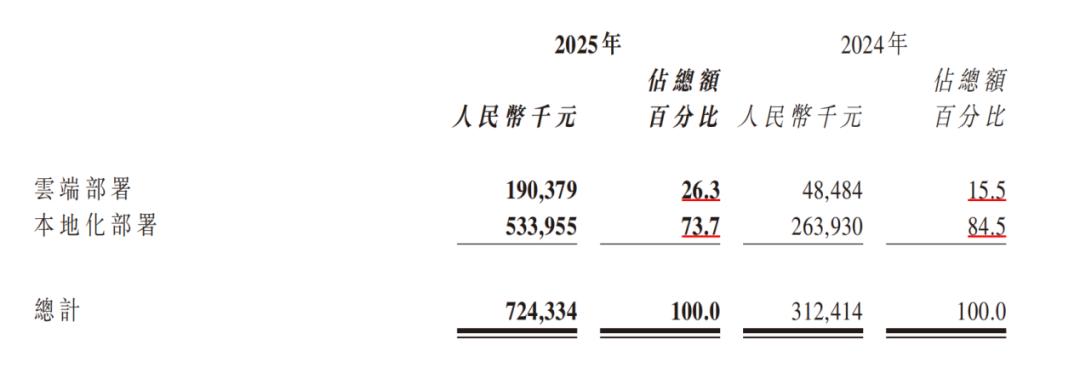

Revenue reached 720 million yuan, more than doubling from 310 million yuan in 2024.

Breaking it down, localized deployment's share dropped to 73.7%; cloud deployment rose from 15.5% to 26.3%. The problem: cloud business gross margin was only 18.9%, far below localized deployment's 48.8%. This dragged the overall gross margin down from 56.3% to 41%.

Zhipu clearly wants to focus on MaaS. A few weeks ago, it established two subsidiaries, 'Beijing Zhiyuan Chengzhang Technology Co., Ltd.' and 'Hangzhou Zhifu Qianhang Technology Co., Ltd.,' retaining model R&D and platform capabilities under the parent company Zhipu. Enterprise solutions, privatized deployments, and project deliveries will gradually be handled by the subsidiaries.

Overall, the financial report sends a clear signal: Zhipu is shifting its growth narrative from heavy localized deployment to lightweight Token sales.

Maintaining model strength has cost Zhipu a lot of money.

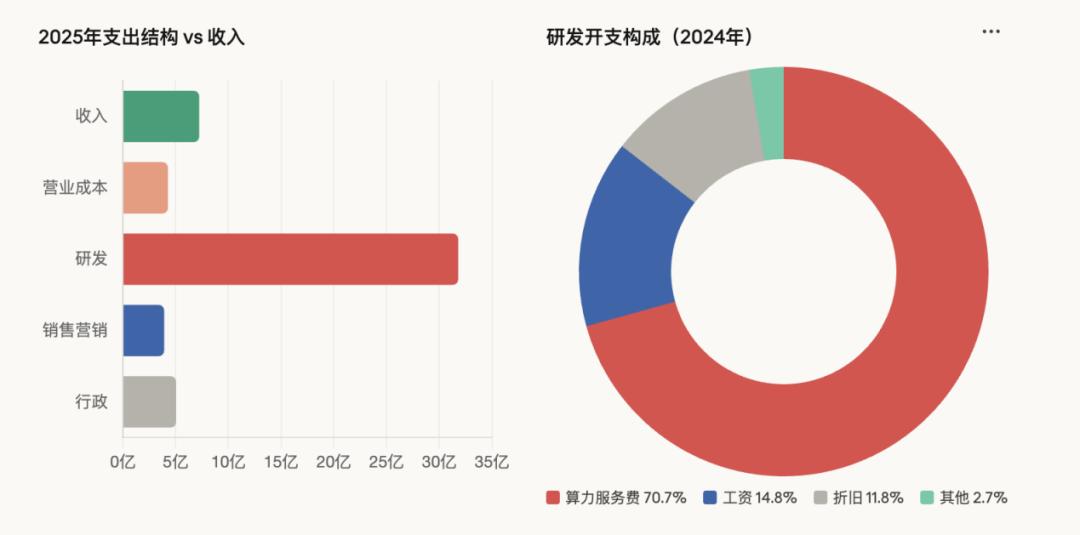

R&D expenses hit 3.18 billion yuan, 4.4 times revenue. The bulk was on computing power, accounting for over 70% of R&D investment. Capital expenditures plummeted from 460 million yuan the previous year to 74.7 million yuan, an over 80% drop. This was mainly due to a shift from leasing GPUs to on-demand computing power purchases. While more flexible, long-term costs may not be lower.

Overall, annual losses reached 4.718 billion yuan. For every yuan earned, five were lost.

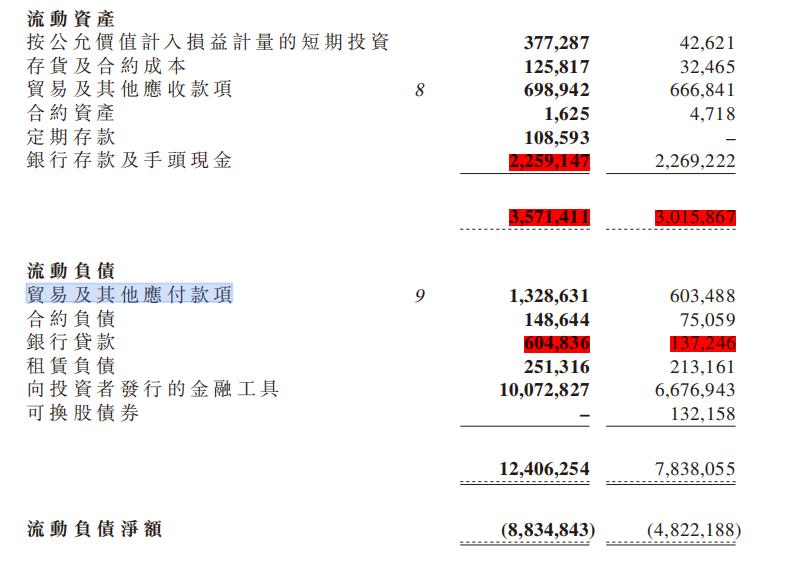

The burn rate is alarming, but Zhipu isn't short on cash.

According to the financial report, it has 2.26 billion yuan in cash on hand, plus 4.5 billion yuan from IPO proceeds and 5.2 billion yuan in unused bank financing. At a monthly burn rate of over 300 million yuan, the runway remains long.

Price Hikes, and People Still Buy

The profit statement may not look ideal, but there's a positive signal: amid supply-demand mismatches, Zhipu is raising prices—and people are still buying.

Let's look at the financials. By March 2026, platform registered users surpassed 4 million. After an 83% API price hike in Q1 2026, call volume surged 400% instead of declining.

According to public pricing adjustments:

In February, Zhipu announced a Coding Plan price adjustment, citing sustained strong demand for GLM Coding Plan, with rapid growth in user scale and call volume. It canceled first-purchase discounts while retaining quarterly and annual subscription discounts, with package prices rising by at least 30%.

On March 16, Zhipu launched GLM-5-Turbo, a base model deeply optimized for OpenClaw scenarios, raising API prices by 20%. For individual and enterprise users, the 'Longxia' package offers a Claw Experience Monthly Card at 39 yuan/month (35 million Tokens) and a Claw Advanced Monthly Card at 99 yuan/month (100 million Tokens).

Against an industry backdrop still dominated by price wars, this marks the first price hike by a Chinese large-scale model—and users didn't leave, indicating Zhipu has pricing power in at least some scenarios.

During the earnings call, Zhipu noted that MaaS's ARR (Annual Recurring Revenue) reached approximately 1.7 billion yuan, a 60-fold increase over 12 months.

ARR reflects recent momentum, not full-year averages. If sustained, 2026 revenue figures will look very different.

That's why Zhang Peng dared to announce at the earnings call that when models are strong enough, APIs are the best business model. In 2026, Zhipu will follow Anthropic's commercial path in China.

Ditching OpenAI, Embracing Anthropic

This gives Zhipu the confidence to become China's Anthropic.

Why? Because Anthropic makes money.

Anthropic is AI's most astonishing growth story. In 15 months, its ARR soared from $1 billion to $19 billion. With only 5% of ChatGPT's user base, it generates over 40% of OpenAI's revenue, with per-user monetization efficiency eight times higher. Enterprise APIs drive ~80% of its revenue.

Zhipu wants to follow this path. The logic holds: Chinese consumers expect free services, making B2B a more realistic revenue source. If models are strong, enterprise clients are willing to pay.

But becoming Anthropic is a long road. The gap in scale is significant.

As of April, Anthropic's 2026 ARR reached $30 billion. At current growth rates, markets discuss its potential to turn profitable in coming years. With a $380 billion valuation, its PS multiple is ~12x. Zhipu's market cap is ~HK$350 billion, with 2025 revenue of 724 million yuan. Its PS multiple is ~450x.

Zhipu's valuation premium comes from two sources: scarcity of AI stocks in Hong Kong and market buy-in for the 'China's Anthropic' narrative.

Whether the story holds depends on several key variables:

First, can pricing power be sustained?

An 83% price hike with demand still outstripping supply is a good sign. But Zhipu's 2025 financials don't break down API revenue structure. How much comes from channel distribution, project deliveries, and Zhipu's true platform capabilities remains unclear. With models iterating every three months and Alibaba, ByteDance ramping up efforts, how will Zhipu address clients-as-competitors? Zhang Peng didn't clarify this during the earnings call.

Second, when will economies of scale kick in?

As mentioned, Zhipu's formula is 'Intelligence Ceiling × Token Consumption Scale.' The Intelligence Ceiling relies on costly R&D. The question is whether domestic chip adaptations can approach NVIDIA's efficiency. If Zhipu maintains over 130% compound revenue growth while slowing R&D expense growth, it could theoretically reduce R&D spending to reasonable levels in 2-3 years. At that point, a 41% gross margin means strong operating leverage once scale effects emerge, making the Anthropic narrative more plausible.

Third, how fast can it transition from project-based to platform-based?

Localized deployment still accounts for 70% of revenue. This business has declining margins and heavy delivery requirements, making scalability difficult. Zhipu needs to rapidly increase the share of cloud APIs to truly monetize Tokens like Anthropic.

But the model market isn't like internet platforms—head players can't dominate everyone. Top-tier models serve premium clients and may become oligopolies, but 90-point models can also gain volume through cost-effectiveness.

This volume isn't limited to domestic markets. Zhipu is also popular overseas.

According to public information, Zhipu's MaaS growth also comes from Token ' go overseas ' (going global). Over the past year, it has partnered with multiple Middle Eastern and Southeast Asian countries to export model capabilities, essentially generating revenue through Token calls. Zhipu officially disclosed that its enterprise API services cover over 50 countries and regions, with overseas revenue accounting for 35% of API income in early 2026, up from 5% in early 2024.

Currently, significant growth potential remains at the application and API layers. Given that no Chinese company has yet established dominance in the Agent framework track ( track = track/field), the first to succeed will define the space. Zhipu, DeepSeek, Kimi, and Alibaba are all vying for this. This is the main focus in 2026.

Looking at internet and cloud computing development paths, infrastructure-layer scale effects only emerge after application-layer success drives call frequency and client stickiness.

The same logic applies to today's large-scale model industry.

Neither Zhipu nor other model companies can rely solely on model capabilities for monetization at this stage. They still depend on validating application scenarios. Thus, model companies are now developing Agents and participating in the 'Longxia' trend to actively cultivate future infrastructure revenue demand. But this The premise (premise) is that Zhipu's models remain strong and maintain engineering capabilities. The question of how much money this will burn is one Zhipu must answer.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?