In the first quarter, the financing for embodied AI started from tens of millions, with a cluster of billion-level deals. The race for 'implementation' has just begun.

04/08 2026

04/08 2026

713

713

In the first quarter of 2026, the embodied AI sector witnessed a capital frenzy rarely seen in the global tech landscape.

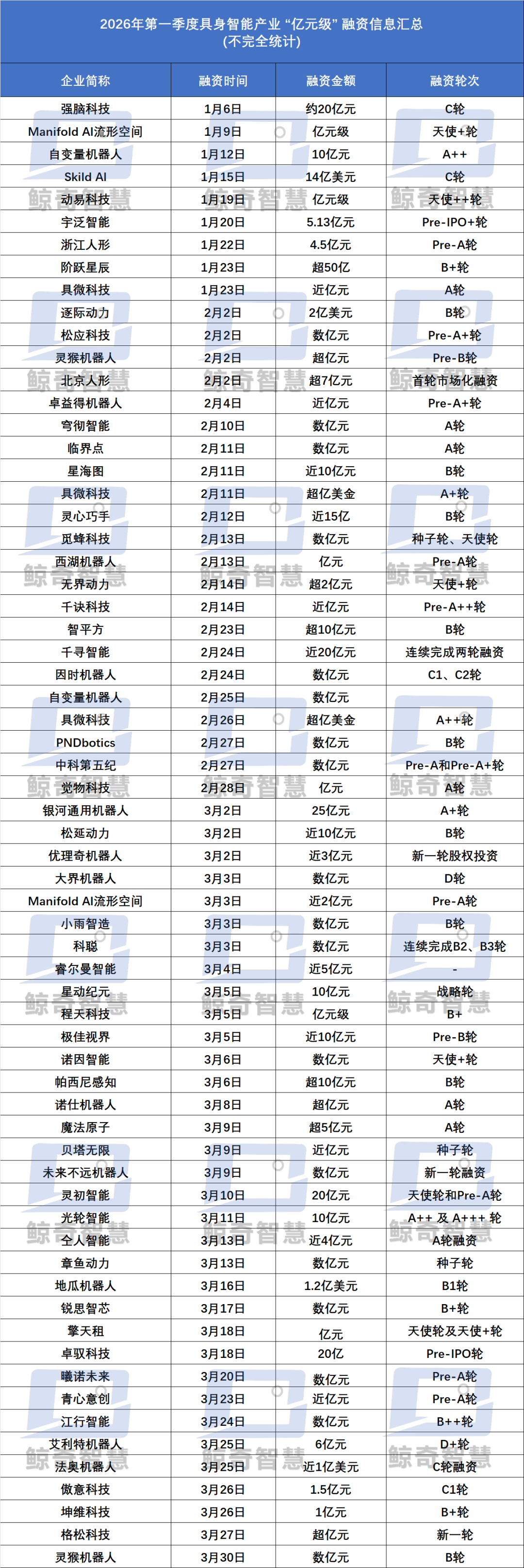

As of March 31, the total financing over 90 days accumulated to over 30 billion yuan, with corporate financing starting at 'tens of millions,' averaging a daily inflow of over 330 million yuan, and multiple billion-yuan deals closing in rapid succession. A group of companies, including Galaxy General, Enchanted Robotics, Unitree Robotics, Stellar Atlas, Stellar Era, Zhipingfang, Qianxun Intelligence, Autovariable Robotics, Paxini Perception Technology, and Songyan Power, have already joined the ranks of unicorns with valuations exceeding 10 billion yuan.

The collective debut of robots on the Spring Festival Gala, the one after another delivery of thousand-unit orders in factories, and the transition of commercial scenarios from demonstrations to normalized operations all signal that 2026 marks the year embodied AI officially steps out of the lab and into large-scale delivery and commercialization.

1 Billion Yuan Becomes the Threshold for Leaders, Investment Logic Reconstructed

This round of financing is not just a hype but a fundamental shift from 'investing in stories' to 'investing in delivery,' completely rewriting the capital rules in the embodied AI sector.

1. Financing Landscape: Head Concentration, Extreme Matthew Effect

The industry exhibits a highly concentrated pyramid structure. In the first three months of 2026, the cumulative financing amount exceeded 30 billion yuan, with nearly 10 deals surpassing 1 billion yuan. After financing, six embodied AI robotics companies broke the 10 billion yuan valuation mark, with 1 billion yuan becoming the hard threshold for entering the first tier. Qianxun Intelligence raised nearly 2 billion yuan in two rounds, while Lingxin Qiaoshou, Zhuji Dynamics, and Zhipingfang secured over 1 billion yuan in their Series B rounds. Autovariable Robotics raised 1 billion yuan in just its Pre-A++ round, with funds highly concentrated in companies possessing full-stack technology, mass production capabilities, and real orders.

The investor structure has also undergone a qualitative change. Industrial capital, national capital, and local mother funds have become the dominant forces, with the National Integrated Circuit Industry Investment Fund III, CRRC Capital, SAIC Capital, Baidu Strategic Investment, ByteDance, and CATL-affiliated funds entering the fray. Financial investment institutions have taken a backseat, as capital no longer bets on a single technological route but on the entire national strategic industry of the 'Physical AI Era.'

2. Capital's Ironclad Selection Criteria: Four Types of Enterprises Favored by Billion-Yuan Funds

Combining the common characteristics of companies securing large-scale financing in this round, the capital market has formed four core selection criteria, akin to industry 'admission tickets':

Full-stack Technological Autonomy: Self-developed VLA (Vision-Language-Action) large models, with hardware, software, and algorithms under autonomous control, free from external bottlenecks. Autovariable's end-to-end VLA model received joint investments from ByteDance, Alibaba, and Meituan. Stellar Atlas's 'One Brain, Multiple Forms' technology has secured thousands of orders, becoming a benchmark for the commercialization of large models.

Robust Mass Production and Delivery Capabilities: Possessing self-built or partnered production lines, stable yield rates, and planning for ten-thousand-unit capacities, rejecting 'show but can't produce.' Zhipingfang's self-built production line has achieved real deliveries of hundreds of units per month, while Lingxin Qiaoshou has become one of the few companies globally capable of producing a thousand high-degree-of-freedom dexterous hands per month, with its supply chain capabilities highly recognized by capital.

Validated Real Commercial Closed Loop: Holding thousand-unit orders and long-term framework agreements, with a clear payback period. Qianxun Intelligence's humanoid robot 'Xiaomo' has been deployed on CATL's Zhongzhou base battery PACK production line, surpassing human efficiency and matching the pace of skilled workers, having produced nearly a thousand batteries. Zhipingfang signed a 500 million yuan, thousand-unit order with HKC's subsidiary, Shenzhen Huizhi IoT, shortening the payback period in industrial scenarios to 2-3 years.

Top-tier Composite Team DNA: A trifecta of academia, industry, and engineering mass production, with no obvious weaknesses. Teams from Galaxy General, Zhipingfang, Qianxun Intelligence, Paxini Perception Technology, Stellar Era, Autovariable Robotics, and Stellar Atlas span the entire chain of AI large models, intelligent hardware, and mass production delivery. Qianxun Intelligence, Zhipingfang, Galaxy General, and Paxini Perception Technology are composed of industrial robot veterans and top scientists, balancing technological R&D with commercial implementation.

Capital has spoken with its wallet: Only companies capable of entering factories, working, mass-producing, and generating profits possess the foundation for sustained valuation growth.

From Factories to Business Districts, Commercialization Enters Deep Waters

2026 is widely regarded as the 'Year of Embodied AI Implementation.' Robots have completed the crucial leap from 'exhibits' to 'commodities,' with scenario implementation showing a clear gradient penetration pattern.

1. Industrial Scenarios: Main Battleground, Scalable Fulfillment of Thousand-Unit Orders

Manufacturing is the primary implementation arena for embodied AI, with 3C electronics, automotive parts, semiconductors, and new energy production lines as core application scenarios. Companies like Galaxy General, Zhipingfang, and Qianxun Intelligence have successively fulfilled thousand-unit orders, with robots undertaking high-risk, repetitive, and high-precision tasks such as assembly, inspection, and patrol, significantly replacing human labor.

The core business logic is clear, with the average price of industrial humanoid robots dropping below 500,000 yuan and a single-unit payback period of 2-3 years, providing clear economic viability. Domestic humanoid robot shipments are expected to exceed 60,000 units in 2026, a more than threefold increase year-on-year, with industrial scenarios accounting for over 70%, becoming the core engine of industry growth.

2. Commercial Services: New Blue Ocean, Transitioning from Demonstrations to Normalized Operations

Scenarios such as cultural, commercial, and tourism venues, dining, retail, and stadiums have become the second growth curve, with robots transforming from 'festival pop-ups' to full-time on-site employees. Zhipingfang's 'Zhi Mofang' has landed in Beijing and Shenzhen, with robots stably making coffee and desserts for 8 hours daily, producing hundreds of cups per store per day, achieving a real commercial closed loop. Robots for cinema guidance, supermarket services, and energy patrols have been deployed in batches, verifying the dual value of cost reduction, efficiency enhancement, and experience upgrading.

The key breakthrough in commercial scenarios lies in autonomous navigation in open environments, multi-device collaboration, and natural human-machine interaction, with robots shifting from 'check-in demonstrations' to 'standardized operations.' Once the single-store model is validated, it can be rapidly replicated across cities and stores.

3. Cutting-Edge and Household: Technological Preheating, Unlocking Long-Term Market Space

Pilot applications have begun in energy, aerospace, emergency response, and medical fields, with robots undertaking high-risk and extreme environment operations inaccessible to humans, steadily advancing technological verification.

The household scenario, of greatest concern to the public, is still in the preheating stage. Lightweight companion and educational robots have seen prices drop to the 30,000 yuan range, with small household robots priced at ten thousand yuan opening for pre-sale. However, universal household assistants still require patient capital.

It can be said that the current industrial landscape of embodied robots is gradually clarifying, with industrial scalability, commercial piloting, and household preheating.

Brain Evolution and Body Iteration: The True Awakening of Physical AI

2026 marks the 'awakening of Physical AI' for embodied intelligence. Robots are poised to achieve a leap from 'programmable machinery' to 'autonomous agents,' with technological breakthroughs concentrated in three dimensions.

1. Embodied Large Models: From Perception to Decision-Making, Data Closed-Loop as Core Barrier

VLA large models have become ubiquitous, endowing robots with environmental understanding, intent recognition, and task generalization capabilities, thoroughly breaking free from traditional scripted control. Leading companies have formed a positive flywheel of 'operation-data-model optimization-scenario expansion,' with real-world operational data replacing simulated data, and data hours becoming a core competitive metric.

Autovariable's WALLA series model achieves a complex operation success rate of over 90%, with Leju Robotics producing 20 million real machine data points annually. Qianxun Intelligence has accumulated over 200,000 hours of real interaction data, accelerating model iteration speed from 'monthly updates' to 'weekly iterations.'

2. Hardware Localization: Cost Plummets, Mass Production Foundation Solidified

By 2025, the localization rate of core components for embodied AI robots has risen to 70%-75%, with key parts such as joint modules, reducers, and frameless torque motors dropping from ten thousand yuan to thousand yuan levels, causing the overall machine cost curve to steeply decline. 'Standing firm, walking steadily, and grasping accurately' has shifted from being a highlight to a basic entry threshold.

3. System Engineering: From Single Skills to Multi-Task Collaboration

The new generation of robots pursues stability, reliability, usability, and ease of use, rather than single flashy maneuvers. A single robot can now perform composite tasks such as sorting, assembly, inspection, and interaction, with scenario adaptation cycles compressed from months to within 24 hours. Multi-robot collaboration and human-robot coexistence have become the norm, with robots truly becoming a 'new job category' in production lines and scenarios.

Apart from core technologies like chips reliant on overseas imports, China's embodied AI robotics face no disruptive barriers at the technological level. The real competition has shifted to engineering, stability, cost control, and delivery capabilities, which are core propositions on the eve of mass production.

Prosperity Hides Multiple Industry Contradictions, Development Entails Growing Pains

Beneath the surface of dual prosperity in financing and implementation, the industry still faces unavoidable challenges. These contradictions are inevitable stages in the industry's transition from basic to maturity.

1. Mismatch Between Technological Showmanship and Commercial Needs

Some companies remain obsessed with demonstrating extreme maneuvers while ignoring real-world pain points: Being able to demonstrate ≠ being able to mass-produce, being able to mass-produce ≠ being able to work stably, being able to work ≠ being economically viable. Discussing technology without considering cost, reliability, and payback periods will ultimately lead to market elimination, a primary reason for the accelerated exit of SMEs.

2. Gap Between Capacity Planning and Actual Delivery

The industry is not short of grand plans for 'ten-thousand-unit annual capacity,' but models capable of stable delivery, meeting yield targets, and operating reliably over the long term remain scarce. Supply chain run in , quality control systems, and after-sales maintenance are the biggest obstacles to mass production, with core components such as high-precision sensors and specialized chips still at risk of being bottlenecked.

3. Lack of Standards and Fragmented Ecosystem

The industry lacks unified standards for performance, safety, and interaction, with incompatible technological routes among different companies and high scenario adaptation costs. Ecosystem fragmentation directly slows down overall scalable expansion, with leading companies beginning to promote ecosystem integration through open-source models and participation in standard-setting. In the long run, embodied AI will follow the industrial path of smartphones: technological maturity → cost reduction → scenario explosion → ecosystem monopoly, at which point the global embodied AI market size is expected to reach the trillion-dollar level.

WhaleQi Commentary

The 2026 embodied AI competition has just begun. The billion-yuan financing frenzy is not a bubble but a coming-of-age ceremony for the embodied AI industry.

Capital has shifted from frenzy to rationality, technology from concept to practicality, and implementation from demonstration to commercialization, marking the industry's official departure from the 'storytelling stage' into the deep waters of 'quantifying mass production, determining success by delivery, and differentiating by profitability.' Chinese companies have already gained an early advantage in mass production, scenarios, and supply chains. The next three years will not only decide the survival of individual companies but also determine China's global industrial voice in the Physical AI Era.

*Editor's Disclaimer: Original content is hard-earned; please respect the author. For reprints, please contact us.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?