Cost Reduction Fails to Secure Real Profitability: The Hard Battle of SenseTime's Transformation Has Just Begun

04/09 2026

04/09 2026

584

584

Shifting from a computer vision leader to a generative AI powerhouse, SenseTime delivered a 2025 financial report showing both revenue growth and loss reduction.

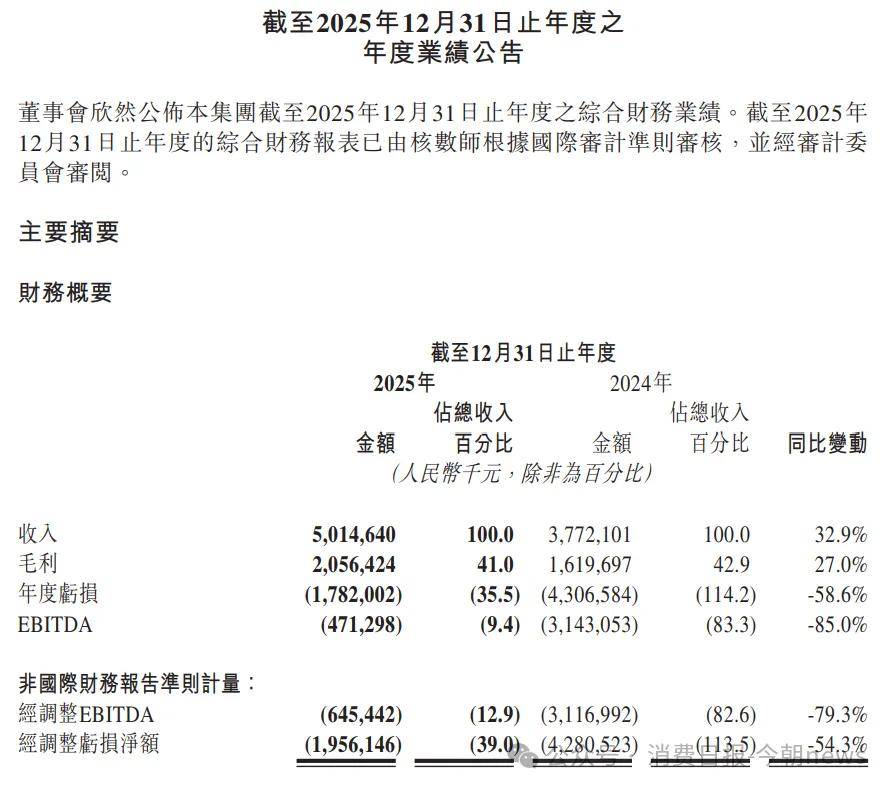

In 2025, SenseTime's revenue surpassed 5 billion yuan, with net losses narrowing by 58.6% to 1.782 billion yuan. Generative AI accounted for over 70% of revenue.

Image source/Company financial report

While overall performance appears positive, a closer look at the financial data reveals that improvements heavily relied on layoffs, cost reductions, business divestitures, and one-time gains.

By the end of 2025, the workforce had shrunk to just 2,472 employees, down significantly from over 6,000 at the time of listing, with all three major expense categories compressed.

Although cost reductions drove performance recovery, generative AI growth slowed sharply.

Against a backdrop of weakening primary business momentum, declining gross margins, and intensifying market competition, a tough transformation battle—shaped by SenseTime's CV heritage, computing costs, and commercialization bottlenecks—has truly begun.

1

Layoffs and Divestitures Prop Up Performance, Raising Concerns Over Profit Quality

In 2025, SenseTime's net loss narrowed by 58.6% year-on-year to 1.782 billion yuan, with adjusted losses down 54.3%, signaling performance improvement.

Image source/Company financial report

However, this was not due to core business strength but rather a combination of strict cost controls, sharp reductions in asset impairments, and one-time gains.

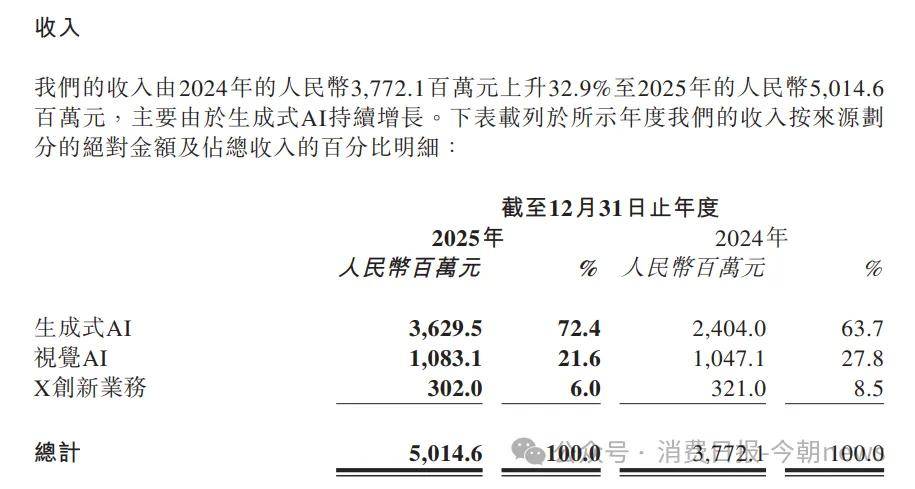

In 2025, SenseTime reclassified its revenue disclosure, shifting from three segments—"generative AI, visual AI, and intelligent vehicles"—to "generative AI, visual AI, and X Innovation Business (intelligent driving, home robots, etc.)."

Generative AI, the primary business, generated 3.63 billion yuan in revenue, up 51.0% year-on-year and accounting for 72.4% of total revenue, becoming the growth engine.

Image source/Company financial report

Traditional visual AI grew just 3.4% to 1.083 billion yuan, while "X Innovation Business" (including intelligent driving) declined 5.9% to 302 million yuan, contributing less than 6% overall.

Driven by strong generative AI revenue growth, SenseTime's annual revenue reached 5.015 billion yuan, up 33% year-on-year. However, this was insufficient to support a 58.6% loss reduction.

Compared to revenue growth, SenseTime's key performance lever was unsustainable cost-cutting measures.

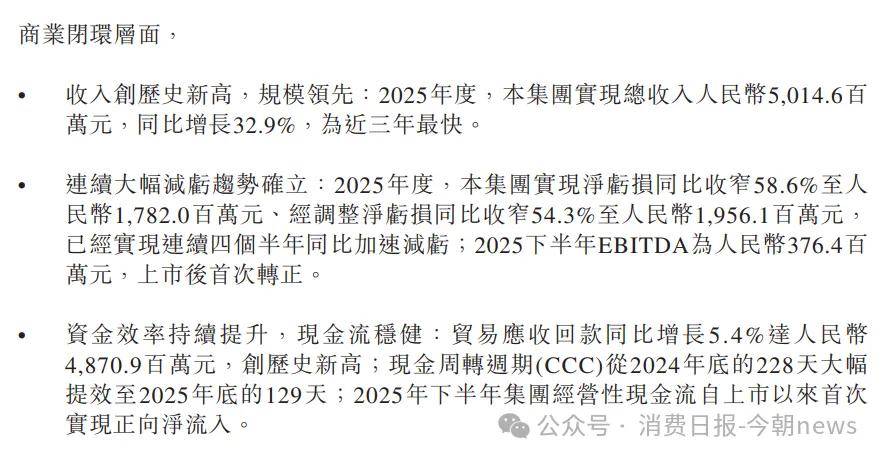

Over the past year, SenseTime laid off 1,284 employees, reducing its workforce from 3,756 in 2024 to 2,472, a 34.2% drop, while also cutting welfare spending.

Staff reductions drove declines across all three major expense categories.

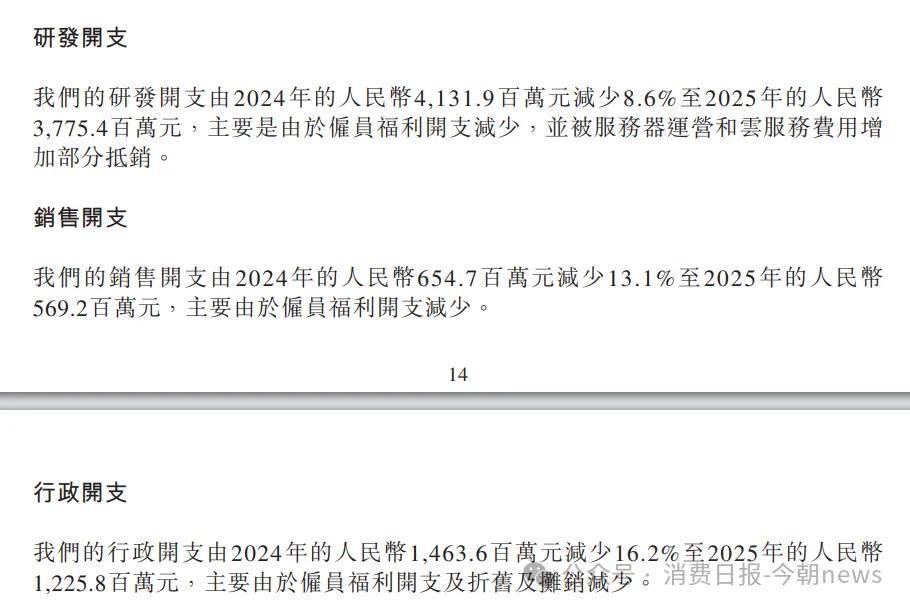

In 2025, R&D spending fell 8.6% to 3.775 billion yuan (its first decline in three years), sales expenses dropped 13.1% to 569 million yuan, and administrative expenses decreased 16.2% to 1.226 billion yuan, a 238 million yuan reduction.

Image source/Company financial report

Annual expenses decreased by approximately 600 million yuan.

Simultaneously, SenseTime adopted a divestiture strategy.

High-R&D, low-profit businesses like intelligent vehicles, smart healthcare, and smart retail were reclassified into "X Innovation Business" and spun off into independent companies for external financing.

At the 2025 results briefing, SenseTime stated that some X businesses had secured external funding and achieved off-balance-sheet status.

This significantly boosted one-time gains.

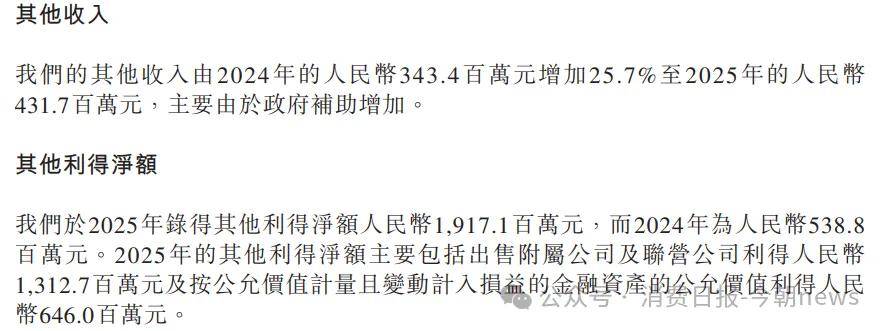

Financial reports showed SenseTime earned 1.313 billion yuan from selling subsidiaries and affiliates, which, combined with fair value changes in financial assets and debt waivers, contributed 1.917 billion yuan in other net gains.

Image source/Company financial report

However, relying on cost-cutting rather than enhancing core operational capabilities risks innovation stagnation and competitive decline, lacking sustainability.

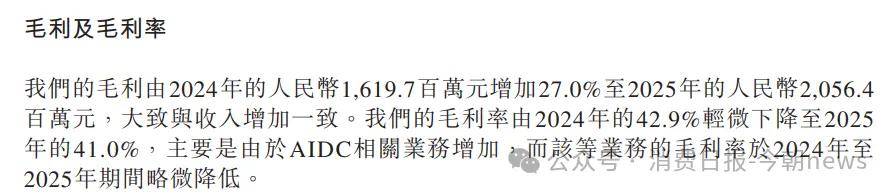

Additionally, profit quality slightly deteriorated, with gross margins falling from 42.9% in 2024 to 41.0% in 2025 due to a rising share of AIDC-related business (lower margins) and sales costs growing 37.4% year-on-year, outpacing revenue growth (32.9%).

2

Over-Reliance on Single Business: Growth Lags Industry

Divestitures and layoffs were SenseTime's ultimate strategies for loss reduction but also highlighted weak core business growth.

From 2021 to 2025, SenseTime incurred losses for five consecutive years. To reverse this, it launched the "1+X" strategy in 2024, splitting off money-losing businesses for off-balance-sheet treatment while implementing large-scale layoffs.

In late 2025, social media reports surfaced about SenseTime's organizational restructuring and layoffs affecting non-core departments like smart cities and intelligent driving.

SenseTime officially downplayed these reports, citing "normal organizational adjustments," "performance-based eliminations," or "business focus."

Yet financial data showed over 1,200 employees were cut that year.

This was not SenseTime's first round of layoffs.

Over five years (2021–2025), its workforce shrank from 6,113 to 2,472, a 3,641-person reduction (nearly 60%), driving compression of the three major expenses.

Image source/Company financial report

While reducing labor costs, SenseTime continued to remove unprofitable businesses from its financial statements.

Under the "1+X" strategy, the "1" (generative and visual AI dual engines) drove growth, while the "X Innovation Business" (ecosystem enterprises like intelligent driving "Jueying," home robot "Yuanluobo," smart healthcare "Shancui," and smart retail "Shanhui") focused on divestitures.

In 2025, intelligent vehicles (Jueying), AI GPU chips, and other "X" businesses were divested less than a year after the strategy's launch.

Although this caused X Innovation Business revenue to drop 5.9% year-on-year to 302 million yuan, SenseTime gained over 1.3 billion yuan in income by shedding these burdens, aiding loss reduction in the reporting period.

However, business adjustments brought new challenges.

Post-divestiture, the group's revenue became more singularly dependent on generative AI performance, while R&D spending declines and core talent loss may impact long-term technical reserves.

Financial data confirmed these concerns.

In 2025, SenseTime's generative AI revenue surged 51.0% year-on-year to 3.63 billion yuan, with its revenue share rising from 63.7% in 2024 to 72.4%.

Yet despite revenue growth, profit quality did not improve, reflecting a "revenue up, profits down" scenario.

Overall gross margins fell from 42.9% in 2024 to 41.0% in 2025, primarily due to a rising share of AIDC-related business with slightly lower margins.

Image source/Company financial report

Meanwhile, resource constraints revealed structural issues, including slowing growth and declining market share.

Generative AI growth decelerated from 199.9% in 2023 to 103.1% in 2024 and further to 51.0% in 2025, a 70+ percentage-point drop in three years, indicating waning momentum.

Alarmingly, this growth rate lagged far behind industry averages.

The "2025–2026 China AI Comic Industry Trends White Paper" showed China's AIGC core market grew 70.8% in 2025, with SenseTime's 51.0% growth falling nearly 20 points short, eroding its prior leadership.

Furthermore, while the "1+X" strategy optimized financial statements by divesting non-core businesses, it also stripped away potential growth scenarios, leaving core businesses to shoulder growth pressures alone and further limiting growth potential.

3

CV Heritage Constraints: Cost and Competition Pressures Mount

SenseTime is accelerating its transformation.

As a domestic computer vision (CV) leader, it shifted from perception intelligence in the AI 1.0 era to generative AI in the AI 2.0 era.

By 2025, generative AI revenue share rose from 34.8% in 2023 to over 70%, transforming SenseTime from a CV leader into one of China's top large model companies.

However, despite initial revenue gains, deep-seated challenges emerged, with technical dependencies, cost structures, commercialization inefficiencies, and market competition forming core barriers to transformation.

SenseTime's transformation faces fundamental conflicts between its technical heritage and R&D paradigms.

As a CV specialist for over a decade, its core technical strengths lie in perception tasks like image recognition, detection, and segmentation, with R&D systems built around CNNs, ViTs, and other CV architectures. Its technical teams, algorithm libraries, and engineering workflows are highly optimized for visual perception.

Generative AI, particularly large language and multimodal models, focuses on content creation and logical reasoning via autoregressive generation and causal attention mechanisms, differing fundamentally from CV in technical foundations, training logic, and optimization goals.

While SenseTime launched the "Intern" multimodal large model and NEO architecture to differentiate through visual-native fusion, the leap from perception to generation requires more than technical layering.

The second major challenge is the crushing burden of computing power and costs.

The generative AI arms race is essentially a computing power race. Despite scaling its "SenseCore" infrastructure to ~40,400 petaFLOPS (FP16) by 2025, maintaining this infrastructure incurred exponential cost growth.

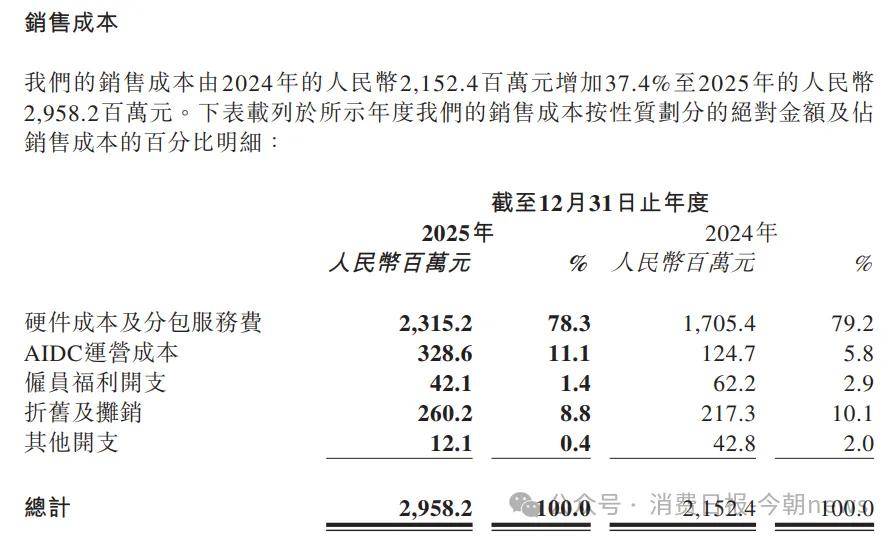

2025 financial data showed sales costs surging 37.4% year-on-year to 2.958 billion yuan, with AIDC computing operation costs skyrocketing 163.5%, directly dragging overall gross margins down to 41%.

Image source/Company financial report

This cost pressure stems from its asset-heavy model—unlike Baidu and Alibaba, which rely on public clouds, SenseTime built its own supercomputing centers, incurring rigid burdens from upfront hardware investments, ongoing power consumption, and equipment depreciation.

Worse, rapid generative AI model iteration demands massive new computing investments for each generation (e.g., NEO), while geopolitical conflicts restricting high-end AI chip supplies further inflate computing acquisition costs.

Additionally, SenseTime faces dual pressures from commercialization challenges and market competition, severely testing its transformation.

In 2025, generative AI revenue reached 3.63 billion yuan (over 70% of total revenue), but growth slowed from 199.9% in 2023 to 51%, lagging China's AIGC core market average of 70.8%, indicating fading momentum.

On one hand, traditional CV businesses (e.g., smart cities, smart commerce) stagnated or contracted, with visual AI revenue dropping 39.5% year-on-year in 2024, unable to sustain new business growth. On the other hand, generative AI commercialization faced "high growth, low margins, weak stickiness" dilemmas.

SenseTime's clients are primarily B-end giants in finance, government, and automotive sectors, with project-based deliveries incurring high customization costs and poor replicability. While C-end products (e.g., Kapi, Raccoon) exceeded 10 million users, monetization efficiency remained low with insufficient paid conversions.

Meanwhile, market competition intensified. Baidu, Alibaba, and Tencent leveraged capital, scenario, and ecosystem advantages to squeeze market share. IDC data showed SenseTime's share of China's AI public cloud services market fell from 16% in 2023 to 13.8% in 2024, dropping to third place.

Emerging players like Zhipu AI and MiniMax captured vertical niches with lighter, more focused models, diluting SenseTime's technical edge. Its refusal to engage in token price wars further limited standardized cloud business expansion.

Overall, SenseTime's generative AI-centric strategy has taken shape, achieving short-term financial improvements through cost compression and burden shedding, completing a business structure shift from visual AI to AIGC.

However, long-term issues like technical path dependencies, asset-heavy computing pressures, "revenue up, profits down" dynamics, and eroding market share remain unresolved. Sustainable profitability cannot rely solely on "cost reduction."

Only by breaking through multimodal technology fusion, enhancing commercialization efficiency, and building stable margin models can SenseTime transition from "financial report loss reduction" to true operational profitability, completing its leap from the CV era to the generative AI era.

-

![]()

Wang Huiwen, Former Meituan Executive, Achieves 20-Fold ROI, Supports 24 AI Startups

-

![]()

Another AI Computing Power Unicorn Launches IPO! Founded by a Changjiang Scholar

-

![]()

OFILM Holdings Secures Zhongke Daojing, Marking a Significant Leap in the Optical Communication Industry!

-

What Will Be the Next Key Battleground for Large Models After AI Coding?

-

![]()

Leapmotor's Sales Soar, Yet Hidden Concerns Loom

-

![]()

China’s Action Camera Market Soars: 3.12 Million Units Sold in Six Months, DJI Secures 74% Dominance

-

![]()

Zhang Yiming: Strategic Retreat as a Path Forward

-

![]()

Exploring Charging for Some Features of QianWen App: Can It Follow the Path of Doubao?