OpenAI Challenges Anthropic, as Chinese AI Firms Quietly Accumulate Profits

04/16 2026

04/16 2026

660

660

A few days ago, an internal memo authored by Denise Dresser, Chief Revenue Officer at OpenAI, found its way to The Verge and CNBC. In the document, Dresser directly accused Anthropic of inflating its revenues by $8 billion through the gross method. Specifically, Anthropic was counting revenues distributed via AWS and Google Cloud as its total income, including the portions retained by these cloud providers. In contrast, OpenAI only recognized revenues after deducting Microsoft's share. Both methods are in compliance with GAAP and are legally sound. However, this adjustment led to a significant reduction in Anthropic's annualized revenue, dropping from $30 billion to $22 billion, which fell below OpenAI's $25 billion.

The title of 'the first major AI company to go public' is highly coveted worldwide. Yet, such a public spat has not occurred in China.

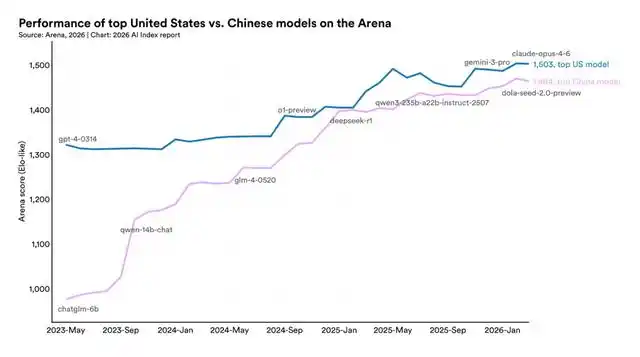

On the same day, Stanford HAI released its 2026 AI Index report, indicating that the performance gap between the leading AI models from China and the US had narrowed to just 2.7%.

On one hand, the two leading AI companies globally are engaged in a fierce rivalry; on the other, their Chinese counterparts, with a diminishing performance gap, remain remarkably composed.

This is unusual.

A Clash Between Titans

Dresser's memo is not merely a discussion of accounting standards; it is a strategic move aimed at undermining the core of the opponent.

To understand this attack, one must first grasp the extent of the animosity between the CEOs of these two companies.

On February 19, 2026, during the group photo session at the New Delhi AI Impact Summit, Altman and Dario Amodei stood on either side of Modi. A Fortune reporter observed a telling detail—the two refused to shake hands throughout the event. This "no-handshake" moment quickly circulated through Silicon Valley, symbolizing the strained relationship between the two AI giants.

The rift between them has deep roots. Prior to founding Anthropic, Amodei served as Vice President of Research at OpenAI. Before his departure, he wrote extensive personal notes, with The New Yorker obtaining over 200 pages earlier this year. One sentence stood out: Altman's statements were "almost certainly bullshit." Altman reciprocated the sentiment, publicly stating this year that Anthropic "sells high-priced products to wealthy clients." Dresser's memo went further, claiming that Anthropic's narrative is "built on fear, restriction, and the belief that a small elite should control AI."

The Pentagon incident a month ago brought this personal feud into the open. Anthropic was listed as a supply chain risk by the Department of Defense for refusing to delete restrictive clauses regarding "large-scale data analysis" in its contracts. Dario wrote a 1,600-word internal letter to employees overnight, calling OpenAI's safety commitments "safety theater," Altman's public statements "straight up lies," and OpenAI employees a "gullible bunch." Altman admitted that signing with the Department of Defense on the day Anthropic was blacklisted "looked opportunistic and hasty," but he proceeded with the contract regardless.

These two individuals view each other as the biggest threats in the industry, and their financial backers share the same perspective.

Anthropic's primary distribution channels are AWS and Google Cloud. An analysis by Seeking Alpha pointed out that cloud partners take gross margins of up to 50% from Anthropic's distribution revenues, with total commissions expected to reach $6.4 billion by 2027. Thus, the $8 billion discrepancy in accounting methods reflects real profit distribution—Anthropic insists on using the gross method because the money does flow through its system; OpenAI argues that you're inflating revenues because the money ultimately doesn't belong to you.

However, what deserves more attention is the intended audience of this memo.

A few weeks ago, Amazon committed $50 billion in investment to OpenAI, with the first $15 billion in cash arriving and the remaining $35 billion subject to conditions. Dresser wrote a telling line in the document—demand on Amazon Bedrock was "shockingly strong," while complaining that Microsoft's partnership "restricts our access to enterprise clients."

In simpler terms: New financial backer, you've invested in the right person. Old patron, you're holding me back.

Google holds a 14% stake (non-voting) in Anthropic, while Amazon is becoming OpenAI's new patron. The competition between the two cloud giants in the AI infrastructure sector has intensified, with AI companies serving as their respective ammunition. Dresser's memo, on the surface, attacks accounting methods but actually accomplishes two tasks: lowering the valuation narrative of competitors and submitting a pledge of allegiance to the new financial backer.

Here's a key structural detail: The underlying logic of AI capital relations in the US is characterized by role separation. Microsoft invests in OpenAI as a cloud infrastructure provider and does not compete in model development.

Amazon invests in Anthropic and then OpenAI, with the core objective that "the more your models are called, the higher my cloud revenues." The interests of financial backers and AI companies are aligned, and the direction is consistent; they only compete over "whose allies are more capable."

Thus, Dresser dares to criticize Anthropic and praise Amazon simultaneously in the memo—she knows this attack will not backfire on her financial backer structure. OpenAI's investors and Anthropic's investors have no cross-shareholdings or hidden connections. Her attack will not accidentally harm teammates.

Coupled with the timing—OpenAI is advancing its transition from a non-profit to a for-profit company, while Anthropic has just completed a new round of soaring valuation—both companies simultaneously need to prove to their respective investors: "I am worth that price." At this juncture, a single memo carries more destructive power than ten product launches.

In the US, mudslinging, once interests are aligned, is a rational choice. Weakening the enemy is the best way to beautify oneself: "Only our model is the best in the world."

Is Mudslinging Necessary?

On January 8, 2026, Zhipu rang the bell at the Hong Kong Stock Exchange under the code 2513. The next day, MiniMax followed suit under the code 00100. In the same week, two Chinese AI companies laid their prospectuses bare for the world to see.

Those numbers are in black and white.

MiniMax generated $79.04 million in revenue in 2025, with 67% of income coming from the consumer side and an overall gross margin of 25.4%; Zhipu generated RMB 724 million in revenue in 2025, with 50.6% of income coming from government and enterprise localization deployments and a gross margin of 56.8%.

One relies on the consumer side, with almost zero gross margin; the other relies on government and enterprise clients, with a completely different business model. If this were Silicon Valley, these numbers would be enough for Dresser to write ten memos—you could say MiniMax is burning money to acquire users, or you could say Zhipu is overly reliant on custom projects and lacks scalability. The ammunition is plentiful, and the target is clear.

But no one fired a shot. At least, no one fired openly.

It has nothing to do with politeness. In this capital network, the cost of open attacks far outweighs that of covert moves.

Everyone's money is interconnected.

The "intricate" capital structure of Chinese AI companies is the result of three overlapping logics.

First, historical trajectory. The investment tradition in China's internet sector has been "investment as ecosystem" since the BAT era—Alibaba and Tencent's strategic investment departments have always been tools for ecosystem expansion, investing in you to lock you into my cloud, my payments, and my distribution channels.

This habit has been almost intactly carried over into the AI era: Alibaba invests in Yuezhiyanmian (Kimi), essentially hoping that Kimi's computing power will run on Alibaba Cloud; Tencent invests in MiniMax, eyeing AI application entry points within the WeChat ecosystem. Between investors and invested companies, the web of "binding-symbiosis" relationships far outweighs the linear relationship of "investment-return."

Second, hedging mentality. Alibaba has its Tongyi Qianwen, Tencent has its Hunyuan large model, and ByteDance has its Doubao—all the major players are developing their own models. At the same time, investing in startups is, to some extent, buying insurance for themselves: if their self-developed models fail to pan out, they at least have a seat on the winner's shareholder list. This has led to an absurd phenomenon—Zhipu's shareholder list includes Meituan, Ant Group, Tencent, and Xiaomi, almost a microcosm of half of China's internet sector. Everyone holds stakes in each other, creating mutual restraint.

Finally, exit mechanisms. The primary exit channel for Chinese AI companies is Hong Kong Stock Exchange IPOs, which have long review cycles and are highly sensitive to industry narratives. Strategic investors need "industry co-prosperity" stories to drive up valuations. The US has more mature secondary market liquidity, allowing startups to enable early investors to partially exit through tender offers without betting everything on IPO day. China's exit paths are narrower, so the motivation to maintain industry narratives is stronger.

We cannot define whether this is a narrative understanding or a capital game, but the result has been surprisingly good: there is ample room for the development of emerging industries, with no scrambling or trampling.

When these three layers overlap, the differences in capital structures between China and the US become clear. The US has a "tree-like" structure—each tree has a single trunk (financial backer) with clear branches and leaves, unentangled with others. China has a "mycelial network"—the underground roots are all connected, and what you think are two independent trees actually share the same nutrient system.

If Kimi publicly attacks MiniMax's gross margin, this punch would not only hit MiniMax but also Tencent. And Tencent is simultaneously a shareholder in Zhipu. Moreover, these financial backers are themselves players in the AI sector—Alibaba Cloud sells computing power, and Tencent Cloud sells model APIs. Infighting among startups is a risk exposure for financial backers.

Vying for the first IPO is fine, but is mudslinging necessary?

Industrial Structures Are Converging

By common sense, after a company goes public, information is forced into the open, and competition should become more transparent, increasing the likelihood of mutual attacks.

The Chinese AI sector is the opposite. Going public adds another lock to silence.

Forty-three days after Zhipu's IPO, its stock price surged by over 500%, and its market cap once exceeded HK$320 billion. MiniMax followed with a correlated rise, and the stock prices of the two companies moved along highly correlated curves. The AI sector in Hong Kong was priced as a whole—institutions were buying the narrative of "Chinese AI" rather than precisely distinguishing between Zhipu and MiniMax.

Mudslinging would be equivalent to smashing one's own plate.

Secondary market institutions simultaneously hold stakes in multiple Chinese AI stocks; what they want is consensus across the entire sector, not zero-sum games. Southbound funds, Stock Connect funds, and global hedge funds—their positions in China's AI sector are diversified, and any negative narrative triggered by one company would spread to adjacent targets.

Although Kimi is not yet listed, Yang Zhilin explicitly stated that ARR surpassed $100 million in March 2026, and its primary valuation continues to climb. Listed companies dare not fire shots, and unlisted ones dare even less—tearing apart the industry narrative prematurely would be self-destructive before the IPO.

Thus, a bizarre equilibrium has emerged: three companies with three completely different business models (Kimi targets consumer-side intelligent agents, MiniMax focuses on global consumer AI, and Zhipu deeply cultivates government and enterprise deployments), serving different clients and earning different money, with far less direct competition than outsiders imagine—but even if competition becomes direct, they will not say so.

Ironically, the US is moving toward China's style of complexity. Amazon simultaneously gave Anthropic $4 billion and OpenAI $50 billion—that's hedging. Google holds a 14% stake in Anthropic while also having its own Gemini, both betting and competing directly. Microsoft's exclusive distribution rights with OpenAI are also loosening, with OpenAI beginning to integrate with other clouds. The "tree-like clarity" of US capital structures is becoming "network-like ambiguity"—just a few years behind China.

But one structural difference will not disappear: Chinese investors are simultaneously competitors, while US investors are primarily infrastructure providers.

The cost of mutual attacks in the former is quadratic—you attack a competitor while harming its investor, who might also be your own investor.

The cost of mutual attacks in the latter is linear—you attack a competitor, and its cloud provider might be unhappy, but it won't cut off your computing power supply as a result.

This structural difference determines that China's pursuit of the US in the AI sector need not be so pessimistic.

Epilogue

The AI sectors in China and the US are still racing ahead. Budgets for government and enterprise intelligence are expanding, C-side users are still growing, and every company feels the pie in front of them is getting bigger. At this stage, silence is the most rational choice—there's no need to grab food from the opponent's bowl when there are still empty seats at the table.

The hands of Chinese AI founders are tied together by the same shareholder table, and the industry's understanding continues.

It may have been unintentionally produced, but isn't this a systemic advantage?

-

![]()

Wang Huiwen, Former Meituan Executive, Achieves 20-Fold ROI, Supports 24 AI Startups

-

![]()

Another AI Computing Power Unicorn Launches IPO! Founded by a Changjiang Scholar

-

![]()

OFILM Holdings Secures Zhongke Daojing, Marking a Significant Leap in the Optical Communication Industry!

-

What Will Be the Next Key Battleground for Large Models After AI Coding?

-

![]()

Leapmotor's Sales Soar, Yet Hidden Concerns Loom

-

![]()

China’s Action Camera Market Soars: 3.12 Million Units Sold in Six Months, DJI Secures 74% Dominance

-

![]()

Zhang Yiming: Strategic Retreat as a Path Forward

-

![]()

Exploring Charging for Some Features of QianWen App: Can It Follow the Path of Doubao?