Tesla Optimus Gen3 Mass Production Imminent: Which Segments Are Most Certain?

04/16 2026

04/16 2026

521

521

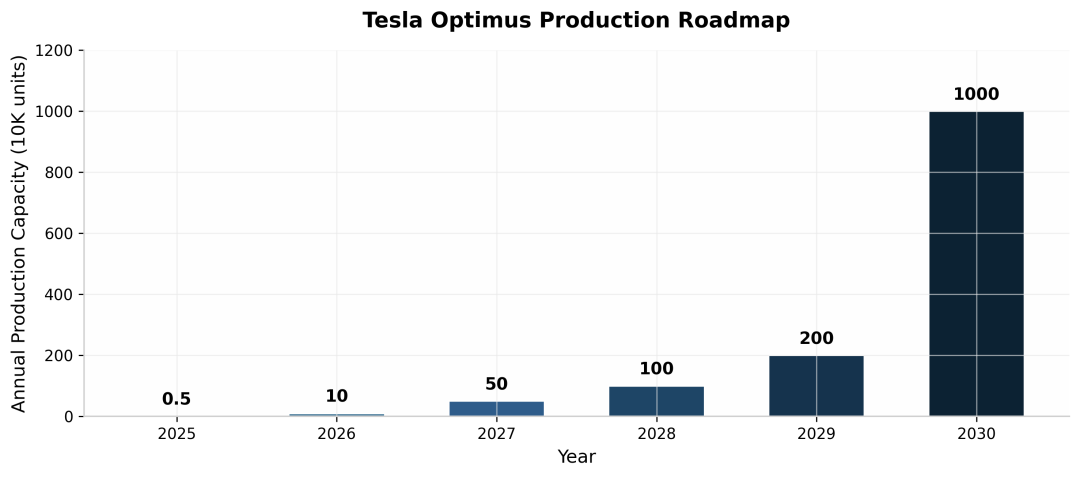

In April 2026, Musk once again set a timeline during an earnings call: Optimus Gen3 production will commence this summer, with large-scale mass production by 2027. At Fremont Factory, the Model S/X production lines are being transformed into a mega-base capable of producing one million robots annually.

If this plan materializes as scheduled, Optimus will become the world's first general-purpose humanoid robot to surpass the one-million-unit production threshold. For capital markets, this marks a pivotal transition—the industry narrative will shift from 'long-term speculation' to 'order validation.'

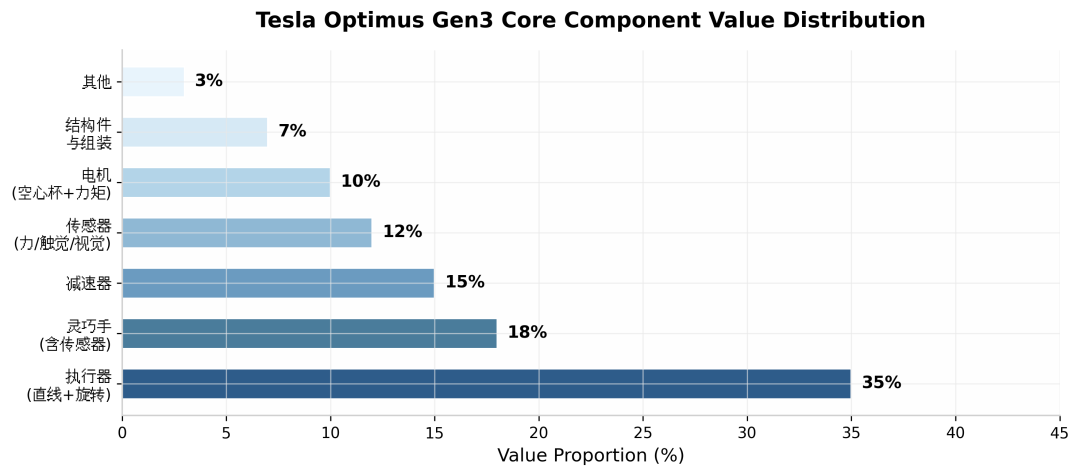

According to IT Home, the Gen3 unit cost is approximately $20,000, with core components accounting for over 70% of the value. Chinese suppliers have secured about 60%-70% of this share. On the eve of mass production, which incremental segments are most certain? Which companies have truly secured their positions? This article dissects these questions using the latest supply chain information and institutional analysis.

Figure 1: Value Distribution of Core Components in Tesla Optimus Gen3

01. Musk's High-Stakes Bet: When Car Production Lines Make Way for Robots

To grasp the strategic significance of Optimus mass production, one must first recognize a key fact: Tesla is sacrificing Model S and Model X production to prioritize Optimus.

These two models are no ordinary mass-market vehicles—they are the cornerstone of Tesla's brand from its inception. By 'cancelling flagship models,' Musk sends a clear market signal: the company's future core assets lie not in automobiles but in artificial intelligence and robotics. As he stated, 'Ultimately, no one will remember Tesla for making cars.' Optimus's future market value is expected to surpass Tesla's automotive business, with related market valuations projected to reach $25 trillion by 2050, accounting for 80% of Tesla's total value.

However, this is not merely a strategic vision issue. Musk's $1 trillion compensation package is directly tied to the goal of 'producing one million robots,' elevating Optimus's strategic priority to unprecedented heights. In other words, whether viewed from the perspective of corporate transformation or personal wealth incentives, Optimus is not a 'side project' for Tesla—it is becoming the biggest determinant of success for this trillion-dollar company.

More intriguing is Musk's assessment of Chinese competition. During the earnings call, he straightforward ('bluntly stated') that 'Tesla's biggest competitor in humanoid robots will certainly be in China,' acknowledging Chinese companies' strengths in 'scalability, manufacturing, and AI capabilities,' while expecting fierce competition. This is no mere courtesy. In 2025, global humanoid robot shipments reached approximately 18,000 units, with Chinese manufacturers accounting for over 86%. Unitree Robotics and Zhiyuan Robotics alone accounted for over 50% of shipments, establishing Chinese companies' first-mover advantage in commercialization.

While Musk admits China is the top competitor, he also emphasizes that Optimus 'will be more powerful than any known Chinese humanoid robot, particularly in AI, hand design, and electromechanical dexterity.' This mix of apprehension and confidence reflects the essence of current global humanoid robot competition: China leads in hardware manufacturing and scalable delivery, while the U.S. maintains advantages in AI algorithms and high-precision electromechanical design. However, these boundaries are rapidly blurring.

02. Precision Transmission: Localization Logic of Lead Screws Comes to Fruit

Figure 2: Tesla Optimus Mass Production Timeline and Capacity Planning

Among Gen3's hardware iterations, the transmission system's value surge is most notable. Linear actuators transition from traditional ball screws to planetary roller screws, enhancing load capacity and lifespan. Each Gen3 unit is expected to incorporate over 34 planetary roller screws, primarily in high-load joints like legs and waist, with a per-unit value of approximately 8,000-10,000 yuan.

For years, this high-barrier sector was dominated by Germany's INA and Sweden's SKF, but domestic manufacturers are now breaking through.

Wuzhou Xinchun (603667) is currently the A-share stock most closely tied to Tesla's supply chain for lead screws. In March 2025, the company signed a strategic agreement with Tesla Tier 1 supplier Xinjian Transmission to supply core components for planetary roller screws and miniature ball screws. By December 2025, Wuzhou Xinchun passed Tesla's mass production audit, officially joining the Gen3 core supplier ranks.

In terms of capacity, the company's 1 billion yuan private placement project, approved in late 2025, plans to produce 980,000 planetary roller screws and 2.1 million miniature ball screws annually, meeting demand for approximately 70,000 robots upon full capacity. Despite its robotics business not yet scaling, the company achieved 2.661 billion yuan in revenue in the first three quarters of 2025 (up 7.6% YoY), with the market already pricing in a forward P/E ratio exceeding 340x—essentially a premium for the certainty of lead screw localization.

Another key player is Xinjian Transmission itself. Regarded as a Tesla Tier 1 supplier, the company initiated A-share IPO counseling in January 2026, with core products including planetary roller screws and dexterous hand assemblies. Market sources indicate Xinjian Transmission has secured Tesla orders for thousands of dexterous hand assemblies annually, with a 1 million-unit screw industrialization project underway. Its IPO process will provide clearer valuation benchmarks for the supply chain.

03. Sensing Upgrades: Value Growth in Dexterous Hands and Sensors

Musk has repeatedly emphasized: 'The dexterous hand is Optimus's most complex subsystem, accounting for nearly half the engineering workload.' Gen3 achieves significant advancements here: 22-degree-of-freedom bionic dexterous hands with 0.08mm fingertip precision, and for the first time, tactile sensing expanded from fingertips to the entire palm—laying the hardware foundation for delicate operations and redefining supply chain value distribution.

Core components within dexterous hands—coreless motors, miniature lead screws, reducers, and tactile sensors—all correspond to clear incremental opportunities.

In the coreless motor sector, Mingshi Electric (603728), a global top-three leader, is the core supplier for Optimus's dexterous hand motors. Its robotics business grew over 300% in 2025, with overseas revenue exceeding 60%. Having passed Tesla's Series C certification, the company expects fixed point orders to materialize in 2026.

For tactile sensors, Fulaishiniao (605488) is China's leading player in flexible tactile sensing (electronic skin). Its resistive technology path aligns perfectly with Tesla's approach, and it has already commenced small-batch deliveries. The per-unit Gen3 electronic skin value is approximately 8,000 yuan, with mass production directly driving order growth.

Six-axis force sensors represent another high-barrier segment, providing real-time detection of three-dimensional forces and torques—the 'nerve endings' for robotic force control. Keli Sensing (603662) is the only domestic company to achieve mass production of six-axis force sensors, with ±0.1%FS accuracy at half the price of overseas equivalents. The company has entered Tesla's supply chain validation sequence, with mass production supply expected in 2026.

04. Conclusion: From Theme-Driven to Order-Driven

The progression of Optimus Gen3 mass production signifies the humanoid robot industry's shift from laboratories to production lines. For investors, core components represent the most certain investment direction currently. Actuators (including lead screws), dexterous hands (including sensors), and reducers collectively account for over 60% of the value, forming the 'hardcore' of the supply chain.

Leveraging precision manufacturing capabilities and cost control advantages, China's supply chain has secured critical positions in lead screws, reducers, motors, sensors, and other key nodes. Companies like Wuzhou Xinchun, Tuopu Group, Sanhua Intelligent Control, Leader Harmonic Drive, Mingshi Electric, and Keli Sensing have either locked in orders through factory audits or entered small-batch delivery stages, with 2026 poised to be a turning point for earnings realization.

While supply chain certainty is converging, 'certainty' itself has a price. When all market participants see the same cards, the space for excess returns often narrows. The real opportunities may lie in technological iteration directions that remain underpriced.

- End -

-

![]()

Wang Huiwen, Former Meituan Executive, Achieves 20-Fold ROI, Supports 24 AI Startups

-

![]()

Another AI Computing Power Unicorn Launches IPO! Founded by a Changjiang Scholar

-

![]()

OFILM Holdings Secures Zhongke Daojing, Marking a Significant Leap in the Optical Communication Industry!

-

What Will Be the Next Key Battleground for Large Models After AI Coding?

-

![]()

Leapmotor's Sales Soar, Yet Hidden Concerns Loom

-

![]()

China’s Action Camera Market Soars: 3.12 Million Units Sold in Six Months, DJI Secures 74% Dominance

-

![]()

Zhang Yiming: Strategic Retreat as a Path Forward

-

![]()

Exploring Charging for Some Features of QianWen App: Can It Follow the Path of Doubao?