Behind DeepSeek's Financing Buzz: China's AI Giants Revalued as Strategic Assets

06/16 2026

06/16 2026

475

475

Today, news surfaced from DeepSeek that could redefine the landscape of AI financing in China. According to reports relayed by The Information via Reuters, DeepSeek's initial funding round has surpassed 50 billion yuan (approximately US$7.4 billion), with a valuation exceeding US$50 billion.

Reuters has cautioned that this information remains unverified, and DeepSeek has not yet issued a response. Therefore, it should not be considered a finalized deal. However, capital markets often assess news based on "pricing direction" rather than what has been "completed."

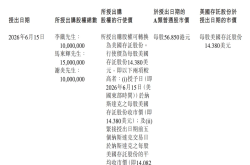

The most striking aspect of this news is not the 50 billion yuan or the US$50 billion valuation, but the control signals embedded in DeepSeek's financing structure. Reports indicate that most investors are not directly investing in DeepSeek but in a limited partnership structure managed by Liang Wenfeng, with a five-year lock-up period and no voting rights. The National Artificial Intelligence Industry Investment Fund stands out as an exception, investing directly and retaining voting rights.

This is no longer a typical large-model financing round; it signals that China's top AI assets are entering a phase of strategic revaluation. Previously, the market viewed DeepSeek through the lens of cost-effective models, open-source influence, engineering efficiency, and China's technological aspirations in AI. Now, an additional layer of value is being considered: national-level AI infrastructure, entry points for industrial intelligence, and the foundational capabilities for China to compete globally in AI.

This valuation logic operates on a different dimension than that of ordinary startups.

The rumors of a US$50 billion valuation are not just a bubble; they signify that China's top AI assets are beginning to command strategic premiums.

If DeepSeek indeed completes its first-round financing at a valuation exceeding US$50 billion, it would mark a unique transaction in the history of Chinese tech entrepreneurship.

Its uniqueness does not lie in its high valuation. The Chinese market has seen highly valued companies and super unicorns before. What sets DeepSeek apart is that it was not previously a typical financing-driven company. It has long relied on the backing of High-Flyer Quant and Liang Wenfeng's capital accumulation to advance R&D, giving the impression of being restrained, low-key, highly efficient in engineering, and not eager to commercialize.

Therefore, amid rumors of this massive financing round, the market's focus should not remain on "DeepSeek is also burning money now." A more accurate understanding is that DeepSeek, once a technological dark horse, is now being repriced by the capital market as a strategic asset.

Over the past year, DeepSeek has achieved more than just an app; it has established a cost narrative. V3 and R1 have prompted the global market to revisit a fundamental question: Does enhancing AI capabilities necessarily rely on unlimited capital expenditure? While U.S. tech giants spend tens of billions of dollars on data centers, GPU purchases, and computing power expansion, DeepSeek has carved out an alternative path through superior engineering efficiency and open-source strategies.

This was its initial source of differentiation, but now, the low-cost route has brought it to a larger capital dilemma. As large models progress, training, inference, data, talent, application ecosystems, and enterprise services all require funding. Low cost does not mean no cost, and efficiency advantages do not equate to bypassing capital cycles.

Especially by 2026, the AI industry has shifted from "model releases" to "agent deployment" and "industrial scenario competition." Companies must compete not only on papers and rankings but also on computing power scheduling, product stability, enterprise delivery, ecosystem partnerships, and long-term financial resources.

This is why DeepSeek's financing rumors hold symbolic significance. They indicate that the valuation anchor for China's large-model industry is shifting from "discounting technical capabilities" to "discounting strategic positioning."

Previously, investors asked whether models were strong, user bases large, or commercialization viable. Now, for top companies like DeepSeek, the questions have become: Is it an irreplaceable part of China's AI industrial chain? Can it serve as the foundational capability for intelligence in manufacturing, automotive, robotics, cloud computing, end-user devices, and energy systems? Is it a critical asset for China in global AI competition?

Once these questions enter valuation models, US$50 billion becomes not just a multiple of revenue but a matter of strategic premium. This will lead to significant industry differentiation. Top large-model companies will be repriced, while bottom-tier large-model companies will face further compression. Capital will not flow evenly to all AI companies but will concentrate more on those with technological acumen, national capital endorsement, industrial capital synergy, and ecosystem entry potential.

The true impact of DeepSeek's financing rumors is not to inflate valuations across all large-model companies but to force the market to make a cruel distinction: Who are strategic assets, and who are merely model suppliers?

Liang Wenfeng did not hand over the company to capital; this structure itself is DeepSeek's bargaining power.

The most noteworthy aspect of this financing round is its structure.

If the reports are accurate, most external investors cannot directly invest in DeepSeek but in a limited partnership structure managed by Liang Wenfeng. Investors face a five-year lock-up period and have no voting rights. The National Artificial Intelligence Industry Investment Fund is an exception, allowed to invest directly and retain voting rights.

This arrangement is rigid. Ordinary startups raising such a large sum would typically compromise on governance rights, board seats, information rights, and exit arrangements. DeepSeek's design clearly reflects not "capital choosing the company" but "the company screening capital." You can enter, but you cannot arbitrarily change the course; you can share future gains, but you cannot pressure the technological rhythm with short-term financial returns.

Behind this lies Liang Wenfeng's firm pricing of control rights. One of DeepSeek's most valuable assets is not just its model but also the organizational culture it has cultivated: prioritizing research, engineering efficiency, and resisting being swayed by commercial KPIs.

This may sound abstract, but for a foundational model company, route stability is crucial. OpenAI's repeated governance controversies over the past few years have proven one thing: The closer an AI company is to foundational capabilities, the stronger the conflicts between capital, teams, technological ideals, commercialization, and regulation.

Liang Wenfeng clearly does not want DeepSeek to enter such complex tensions prematurely.

The five-year lock-up and lack of voting rights suppress both the liquidity and control desires of external capital. Investors willing to accept these conditions are essentially buying not short-term exits but long-term options on DeepSeek becoming China's foundational AI asset. In other words, this funding is not venture capital in the traditional sense but more akin to a strategic ticket.

The exception for the national AI fund is also critical. This shows that DeepSeek's capital structure does not entirely reject external forces but distinguishes between capital attributes. National capital represents strategic endorsement and policy resources, industrial capital represents scenarios and ecosystems, and financial capital provides ammunition without dominating direction. If this structure ultimately materializes, DeepSeek will simultaneously acquire three things: money, endorsement, and control.

This will pressure other large-model startups. Not all companies can secure financing on such terms. Many need capital to survive, so their bargaining power is weak; they need big-tech traffic, so their strategic independence is weak; they need rapid commercialization, so their technological routes are prone to fluctuation. DeepSeek's ability to structure financing this way indicates market recognition of its scarcity.

This is the most pragmatic aspect of capital markets: Ordinary assets sell at discounts; scarce assets sell on terms.

The large-model competition no longer focuses solely on model capabilities; DeepSeek must prove it can convert strategic premiums into operational delivery.

DeepSeek's financing rumors are positive for the industry but not blindly so. They raise the valuation ceiling for China's top large-model companies while increasing market expectations for DeepSeek's delivery.

Previously, DeepSeek could primarily focus on technological differentiation, emphasizing low cost, open-source influence, engineering efficiency, and China's AI capabilities. After securing large-scale financing, it must now answer more practical questions: How will the money be spent? How will revenue be generated? How will commercialization proceed? How will model capabilities remain consistently leading?

This is the pressure all strategic assets face. DeepSeek's opportunities are clear. First, it has established global technological recognition. After V3 and R1, overseas developers, industrial capital, and policymakers view it as a key representative of China's AI capabilities. Second, it possesses open-source ecosystem diffusion capabilities. Compared to closed models, open-source models more easily penetrate developer communities, enterprise privatization deployments, and localization scenarios. Third, it may gain industrial capital synergy. Tencent represents application, cloud, and traffic scenarios; CATL represents manufacturing, energy, and automotive chains. If these capitals ultimately enter, DeepSeek's deployment space will be broader than that of pure internet model companies.

However, uncertainties remain significant. The largest uncertainty is commercialization rhythm. DeepSeek's greatest strength has been technological impact, not revenue proof. Large-model companies cannot ultimately survive on hype alone. API calls, enterprise subscriptions, industry solutions, privatization deployments, and agent ecosystems must all generate real revenue and sustainable gross margins.

The second uncertainty is whether technological leadership can be sustained. AI model iteration is too rapid; today's leadership can easily become tomorrow's version update. DeepSeek must continuously exceed expectations in reasoning, multimodality, coding, agents, and industry models; otherwise, the strategic premium in its valuation will erode.

The third uncertainty is whether capital expenditures will undermine its efficiency label. DeepSeek's brand was built on low cost and high efficiency, but after financing expansion, the market will re-examine its input-output ratio. If investments surge without corresponding model advancements and commercial delivery, the market will begin to question: Has DeepSeek also entered the traditional large-model company's path of burning money?

Thus, I believe that if this financing round materializes, DeepSeek will enter a new phase: transitioning from a technology-focused company to an infrastructure-type company continuously evaluated by the market.

This is not a bad thing. China's AI sector needs such companies. However, it also means DeepSeek can no longer rely solely on "impressiveness" to sustain its narrative; it must now support its valuation with industrial deployment and revenue structure.

Conclusion: DeepSeek raises the ceiling for top companies while lowering the survival space for ordinary model companies.

The most noteworthy aspect of DeepSeek's financing rumors is not that they have rekindled excitement in China's AI sector but that they have redrawn the capital hierarchy within the large-model industry.

Top companies now have the opportunity to secure strategic asset pricing, while ordinary model companies continue to face scrutiny over cash flow. National capital, industrial capital, and long-term funds will be more willing to enter a select few companies with strategic scarcity but will no longer indiscriminately chase all large-model narratives.

This is the most significant shift in the large-model industry in 2026.

Capital remains in AI, and risk appetite has not disappeared, but the market has become more selective. It will grant higher valuations to companies like DeepSeek while posing sharper questions to others: Are you irreplaceable? Do you have industrial entry points? Can you convert models into revenue? If price wars continue, computing costs rise, and client budgets tighten, can you still survive?

DeepSeek has raised the upper limit for China's large models while exposing the industry's lower limits more clearly.

My judgment is that China's AI investment will not recede but will become more concentrated. Financing, policies, industrial resources, and developer ecosystems will converge toward a few top model companies and application companies with genuine scenario delivery capabilities. Those in the middle—lacking both foundational technological advantages and closed-loop commercialization—will find it increasingly difficult to tell their stories.

DeepSeek's rumors are not truly about how much money one company has raised but about China's large-model industry entering a new order: Technological differentiation opens valuations, strategic asset attributes sustain them, and ultimate commercial delivery determines whether they hold.

This is the answer the capital market cares about most.

-

![]()

Duan Yongping Offers Insightful Perspectives: New Hurdles for Long-Term AI Investment

-

![]()

Chinese New Energy Vehicle Design: Stepping Out of the Shadows

-

![]()

Li Auto Awards Executives 35 Million Shares Based on Performance Metrics

-

![]()

Rushing Towards AI 2.0: How Confident is Unisound?

-

经过今年上半年各路AI豪强对市场的反复教育,有一个判断,可能决定未来一两年的走向:

-

![]()

Global Tech Sector Sees Collective Panic: Is the AI Hype Finally Deflating?

-

![]()

Three Consecutive Rises in Heavy Truck Sales: Both New and Old Players are Betting on the Same Thing!

-

![]()

Why Can’t Vivo Bridge the High-End Perception Gap Despite Support from Authoritative Media?