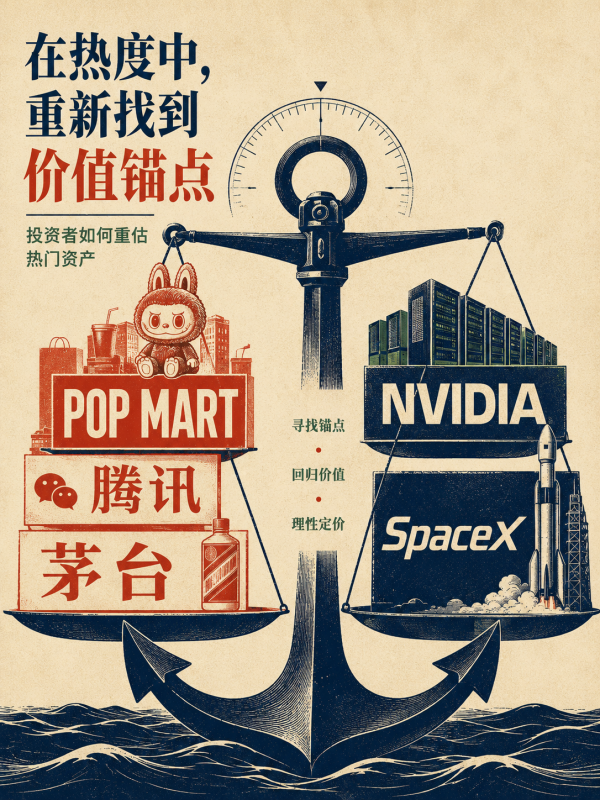

Duan Yongping Offers Insightful Perspectives: New Hurdles for Long-Term AI Investment

06/18 2026

06/18 2026

334

334

Duan Yongping has recently been actively engaging with investors on public platforms, addressing a wide array of queries that span from Pop Mart, Tencent, and Moutai to NVIDIA's bond issuance and SpaceX's valuation.

Individually, each of his responses may seem like a succinct verdict delivered in just a few sentences; however, collectively, they serve as a reliable barometer of the market. Pop Mart's revenue soared beyond 37 billion yuan in 2025, with a rapidly growing share of overseas revenue and Labubu emerging as a sensational intellectual property (IP). NVIDIA re-entered the investment-grade bond market amidst soaring demand for AI chips, planning to raise at least $20 billion. Following its listing, SpaceX's valuation was swiftly reassessed by investors, with debates shifting from concerns of a 'bubble' to questions about 'whether long-term profits can be achieved.' These companies, spanning consumer goods, AI hardware, and space infrastructure, may appear unrelated, but they all point to a common issue: the market is not lacking in stories but rather in new valuation benchmarks.

Duan Yongping refrained from providing specific trading instructions or price predictions. Instead, he repeatedly emphasized the importance of opportunity cost, the circle of competence, cash flow, genuine buyers, and long-term profitability. In the 2026 market environment, these concepts carry even greater significance. Liquidity is still seeking direction, risk appetite is fluctuating, and leaders in AI and consumer sectors are being tested at high valuations. What investors truly need to answer is not 'Can I buy at this price?' but 'What justifies this company's current valuation?'

Even Good Companies Must Navigate Opportunity Cost Constraints Following a Downward Revision of Return Expectations

When questioned about investing in Pop Mart at 179 yuan and Tencent at 466 yuan, Duan Yongping refrained from judging whether these prices were cheap or expensive. Instead, he stated, 'If you have to ask, you shouldn't invest.' This may seem like a dismissive response, but it is actually a cautionary note to investors: without a well-defined circle of competence, there is no pricing power. The most perilous move in the market is not buying the wrong company but substituting others' certainty for your own judgment when you lack understanding.

The 2026 market is not devoid of strong assets. Tencent boasts robust cash flow and shareholder returns, Pop Mart has globalized its IP and demonstrated profit elasticity, NVIDIA benefits from AI computing demand, and SpaceX offers the allure of scarce infrastructure. However, the stronger the asset, the more intricate the pricing. Good companies do not necessarily equate to good prices, high growth does not equate to low risk, and popular sectors do not guarantee long-term returns. Duan Yongping cautioned that many may not achieve annualized returns above 8% in the long run, a judgment that carries more real-world weight than mere 'long-term optimism.'

An 8% annualized return may seem unremarkable in a bull market, but over a decade, it becomes a formidable threshold. It requires investors not only to buy good assets but also to avoid high valuations, profit disconfirmation, liquidity contractions, and emotional sell-offs. Many believe they are investing for the long term but are actually trading on short-term catalysts; they think they are buying certainty but are actually buying when expectations are at their peak.

The metaphor of 'investing is like farming' should not be misconstrued as simply buying and holding. Farming is not about laziness but understanding the interplay between soil, seasons, crops, and harvests. Farmers do not pull seedlings daily to check root growth, and long-term investors should not validate business logic through daily stock price fluctuations. What truly matters is whether the business is improving marginally, whether cash flow quality is deteriorating, whether industry sentiment remains robust, and whether order visibility and profit elasticity have changed.

The first layer of Duan Yongping's responses is to shift the investment focus from price anxiety to return constraints. Prices can be checked daily, but opportunity cost is something no one can calculate for you. When market sentiment is high, capital is willing to pay a premium for long-term potential; when risk appetite falls, the same company is re-evaluated based on profits, cash flow, and growth certainty. Long-term investing is not about rejecting volatility but understanding why you tolerate it.

Valuation Anchors for Consumer Assets Shift from 'Selling Power' to 'Mindshare'

Moutai's stock split and Pop Mart are the two most noteworthy topics in Duan Yongping's recent interactions.

Moutai's lot size exceeding 100,000 yuan indeed poses a challenge for many small investors to participate. Duan Yongping believes Moutai may need to further split its shares to enable more small investors to share in its growth, but he also emphasizes that speculators have no impact on the company, which has only one genuine buyer. This 'buyer' is not a secondary market participant but the end consumer. A stock split can lower trading barriers and increase liquidity but will not alter Moutai's real demand, brand premium, or channel pricing power.

Moutai's capital narrative has shifted from high growth to high cash flow, high dividends, and valuation repair of existing assets. In 2026, Moutai's stock price fluctuates around 1,200 yuan, with a market cap still exceeding 1 trillion yuan and a lot size exceeding 120,000 yuan. For small investors, a stock split is a participation threshold issue; for long-term capital, the core remains the liquor consumption structure, wholesale price stability, channel inventory, and shareholder returns. The real pressure on Moutai comes not from its high absolute stock price but from marginal changes in demand for high-end liquor.

Pop Mart, on the other hand, is at the forefront of a different consumer asset revaluation. In 2025, Pop Mart's revenue exceeded 37.1 billion yuan, net profit exceeded 13 billion yuan, gross margin rose to around 72%, overseas revenue exceeded 16 billion yuan, and the THE MONSTERS series featuring Labubu contributed over 14 billion yuan in revenue. By these metrics, it is no longer a niche trendy toy company but an IP consumption platform with global potential.

Duan Yongping suggested there is a more than 50% chance that Pop Mart's profits will surpass Disney's in 20 years, a controversial judgment but one that offers a fresh valuation perspective: Pop Mart's core is not just blind box sales but whether it can transform Chinese original IPs into global consumption symbols. Its stores are not just retail outlets but venues for emotional experiences and social dissemination. Duan Yongping mentioned that 'store acquisition capability is also a moat,' a statement that underscores the importance of strategic location. Good store locations mean foot traffic, scenarios, conversion rates, and the ability to sustain visible consumption heat.

Pop Mart's greatest potential lies overseas. U.S. stores, European expansion, and markets in the Middle East and South Asia are all testing whether Chinese IPs can gain global pricing power. If overseas revenue continues to grow rapidly, the market will reclassify it from a trendy toy retailer to an IP platform; if Labubu's popularity fades, new IPs fail to emerge, and channel expansion efficiency declines, its valuation will shift from a growth premium back to single-product cycles.

The consumer industry is becoming even more ruthless. Strong product sales are just the first step; what truly matters is whether users are willing to repeatedly pay for emotions, identity, and collectibility. Moutai sells scarcity and business order, while Pop Mart sells happiness, companionship, and social currency for young people. These two companies operate in entirely different consumption cycles but face the same question: Are the genuine buyers still there, and are they willing to keep voting with cash?

AI and Space Assets Enter a Capital-Intensive Phase, Where Narratives Must Be Validated by Cash Flow

NVIDIA's bond issuance is one of the few instances where Duan Yongping used the word 'eerie.' NVIDIA is one of the strongest AI hardware players, with strong profitability, high order visibility, and significant industry influence. The fact that such a company is returning to the bond market in a higher interest rate environment forces investors to re-examine the capital expenditure intensity of the AI cycle.

Public information reveals that NVIDIA plans to issue at least $20 billion in investment-grade bonds with maturities ranging from 2 to 30 years, marking its first entry into the investment-grade bond market in about five years. The bond proceeds will be used for general corporate purposes, repaying, and refinancing existing notes. On the surface, this may seem like capital structure management, but within the AI supply chain, it signals that AI is no longer a light-asset story but is becoming the largest global capital expenditure cycle.

Morgan Stanley estimates that global AI-related debt issuance could reach nearly $570 billion in 2026. Cloud providers, chip companies, data center operators, and power and equipment firms are all raising capital through debt. AI's pricing logic is also evolving. The market previously traded on GPU shortages, profit upgrades, and computing demand; now, funds are questioning whether customers can continue paying, whether data center returns can cover depreciation, and whether supply chain financing will push up risk premiums.

SpaceX's controversy is even more extreme. Duan Yongping initially suspected a bubble but later stated that a $3 trillion valuation would not be unreasonable if annual profits exceeded $150 billion. This shift is not a reversal of sentiment but a change in valuation framework. For an asset like SpaceX, static price-to-earnings (P/E) ratios are meaningless; the market is truly trading on long-term profit potential, launch cost reductions, Starlink cash flow, defense contracts, space data centers, and infrastructure monopoly capabilities.

After SpaceX's listing, its stock rose rapidly, but Morningstar believes its fair value is far below the market price, noting that the market has already priced in difficult scenarios such as 'space data centers' and rapid Starship reuse. Such disagreements indicate that super-tech assets have entered the most intense phase of discounted cash flow valuation. Bullish funds are buying scarcity and future industry control, while bearish funds are focusing on capital expenditures, technological realization, profit paths, and valuation overreach.

NVIDIA and SpaceX represent the most significant investment theme in 2026: hard tech is moving from storytelling to capital-intensive realization. AI requires chips, packaging, servers, liquid cooling, power, and data centers; the space economy requires rocket reuse, satellite networks, ground terminals, defense contracts, and continuous financing. The scarcer the asset, the easier it is to obtain a valuation premium; the heavier the capital expenditure, the more it needs cash flow validation.

Conclusion: The Market Will Reward Companies That Deliver on Their Narratives and Punish Those That Rely Solely on Storytelling

The value of Duan Yongping's latest interactions lies not in which companies he favors or whether he approves of certain prices. More importantly, he places a group of hot assets back within the framework of business fundamentals: long-term returns must account for opportunity cost, consumer brands must focus on genuine buyers, AI leaders must demonstrate cash flow quality after capital expenditures, and space assets must be valued based on long-term profit projections.

The 2026 market will not lack themes. AI debt financing will continue to rise, Pop Mart's overseas expansion will keep generating catalysts, Moutai's valuation repair depends on consumption expectations, and super IPOs like SpaceX, OpenAI, and Anthropic will keep absorbing risk appetite. What capital lacks most is not stories but companies that can turn stories into profits.

Long-term investing is not about slowly accumulating popular assets but finding valuation anchors in popular assets that can withstand cyclical shocks. Narratives that continuously generate cash flow will undergo asset revaluation; those sustained only by emotion will eventually be disproven by logic.

-

![]()

Duan Yongping Offers Insightful Perspectives: New Hurdles for Long-Term AI Investment

-

![]()

Chinese New Energy Vehicle Design: Stepping Out of the Shadows

-

![]()

Li Auto Awards Executives 35 Million Shares Based on Performance Metrics

-

![]()

Rushing Towards AI 2.0: How Confident is Unisound?

-

经过今年上半年各路AI豪强对市场的反复教育,有一个判断,可能决定未来一两年的走向:

-

![]()

Global Tech Sector Sees Collective Panic: Is the AI Hype Finally Deflating?

-

![]()

Three Consecutive Rises in Heavy Truck Sales: Both New and Old Players are Betting on the Same Thing!

-

![]()

Why Can’t Vivo Bridge the High-End Perception Gap Despite Support from Authoritative Media?