Intelligent Agent Payment Landscape: Navigating Opportunities and Challenges in a Flourishing Market

06/19 2026

06/19 2026

412

412

"A Trillion-Dollar Market Rife with Challenges"

In June 2026, the intelligent agent payment sector experienced a fresh wave of vigor.

On June 16, Alipay unveiled its AI-driven application, "Abao," empowering users to effortlessly access tens of thousands of services with a single voice command by simply "swiping right." This innovation redefined service access points for its one billion users through conversational engagement.

On the same day, WeChat Pay showcased its latest breakthroughs in AI-payment integration at the 2026 China International Financial Exhibition. The debut of the "Smart Business Robot" featured a multilingual "AI Access Toolkit," demonstrated innovative in-car AI payment solutions, and announced collaborations with over 40 automotive firms.

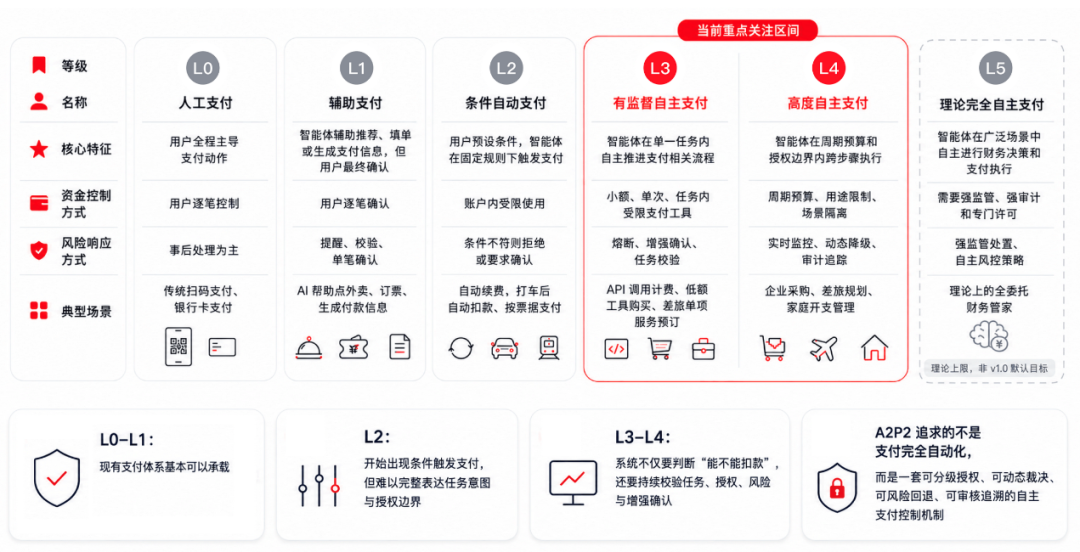

Five days prior, on June 11, JD.com introduced China's pioneering autonomous intelligent agent payment protocol—the Agent Autonomous Payment Protocol (A2P2 for brevity). This protocol systematically classifies the autonomy of intelligent agent payments into six tiers, from L0 to L5, outlining an evolutionary trajectory for autonomy across diverse scenarios.

Adding to this momentum, China UnionPay, in collaboration with 19 domestic and international entities, had previously launched the Agent Payment Open Protocol (APOP) framework... Within mere months, the leading lights of China's payment industry have all entered the fray, engaging in a comprehensive battle to secure their foothold in the intelligent agent payment arena.

This is no mere coincidence but a collective strategic move by major players: the window for intelligent agent payments is ajar, and time is of the essence. The crux of this race lies in the struggle to define the payment rules in the AI era.

Positioning

To comprehend this collective rush, one must first acknowledge a fundamental truth: payment transcends mere financial transactions.

In the mobile internet era, the pioneers who established QR codes as the cornerstone of commercial interactions laid the foundation for the next generation. WeChat Pay and Alipay amassed hundreds of millions of users not by outpacing bank transfers in speed but by seamlessly integrating payment access points into users' daily routines.

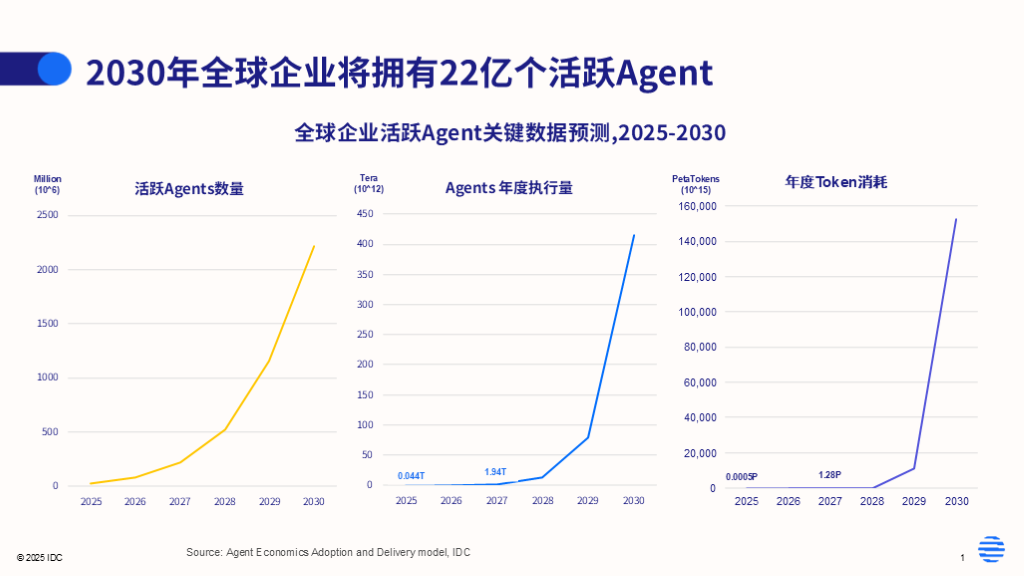

The logic of the intelligent agent era follows a similar vein but on a much grander scale. According to IDC, the global count of active agents is projected to surge from approximately 28.6 million in 2025 to 2.216 billion by 2030—an 80-fold increase in just five years. Huawei's "Intelligent World 2035" report envisions a world with 900 billion AI agents by 2035.

Juniper Research predicts that global agent-based commerce transaction volumes will skyrocket from $8 billion in 2026 to $1.5 trillion by 2030. Furthermore, Gartner, a business and technology insights firm, boldly predicted as early as 2024 that by 2028, at least 15% of daily work decisions will be autonomously executed by AI agents.

These agents, in fulfilling their tasks, will inevitably generate payment demands: booking tickets, making purchases, topping up tokens, cross-platform settlements... Every task chain culminates in a financial transaction. Payment becomes an indispensable link in the commercial closed loop of intelligent agents. Every agent has the potential to become a payment entity. No industry giant would willingly forgo a market of this magnitude.

From this vantage point, the current intensive positioning by major players is essentially a struggle to secure the "payment access point in the intelligent agent era." They all recognize the urgency; failing to position now could mean being left out of the game entirely later.

Because if, in the future, users can complete all transactions simply by issuing instructions to a system-level intelligent agent, payment institutions might be relegated to mere background fund channels, losing their user touchpoints and data value, and facing the risk of being "pipelined." For instance, if a user simply tells their phone, "Transfer money for me," and the system-level agent automatically invokes the underlying payment interface, who would bother to open WeChat or Alipay? This risk of "access point displacement" compels all players to act proactively.

More crucially, intelligent agent payments are reshaping the value boundaries of the payment industry. The core value of traditional payment institutions lies in fund clearing, earning revenue from transaction fees, with a singular business model and a clear growth ceiling. However, in the intelligent agent era, payment institutions must transcend mere fund transfers. They must verify the legitimacy of the agent initiating the payment, ensure the transaction aligns with the user's original intent, retain evidence of the entire decision-making process for dispute resolution, and construct a new risk control system tailored to intelligent agent scenarios.

In essence, payment institutions are evolving from mere fund channels to the underlying infrastructure of the entire intelligent agent commercial era, significantly raising their value ceiling. This explains why protocol standards have become a core battleground in the current positioning war.

JD.com introduced China's first autonomous intelligent agent payment protocol, A2P2; Alipay upgraded China's first open protocol framework for intelligent agent commercial trust, ACT 2.0; China UnionPay also led the release of the Agent Payment Open Protocol (APOP) framework... Each company positions its solution as the "first" of its kind, attempting to establish its technological path as the industry standard. After all, once a company's protocol becomes the industry consensus, it gains the right to shape the rules for the next generation of payments and even commercial interactions—far more significant than the success or failure of a single product.

Opportunities

The convergence of technological advancements and genuine industry demand has provided these players with the ideal timing to invest in intelligent agent payments.

Two years ago, mainstream large models were confined to simple Q&A, with low success rates in tool invocation and incapable of independently completing transaction chains. However, rapid iterations in multimodal large models and multi-agent collaboration frameworks over the past two years have enabled intelligent agents to independently handle the entire process of intent understanding, information retrieval, price comparison, and order submission.

As collaborative pathways for information flow are fully opened, the payment link, as the core of the commercial closed loop, has shifted from a desirable feature to a critical gap that must be filled. A JD.com executive explicitly stated at the Agent Autonomous Payment Protocol Framework seminar that in the era of the intelligent agent internet, the interconnectivity of information flow is taking shape, but the infrastructure for fund flow remains a blank canvas. Failing to fill this gap would prevent the commercial value of agent-to-agent (A2A) interactions from being fully realized.

Genuine industry demand is also scaling up from sporadic penetration to widespread adoption. On the consumer side, the proliferation of intelligent hardware is reshaping payment interaction scenarios. The growing shipments of smart glasses, AI phones, and intelligent cockpits naturally lend themselves to voice interactions. Traditional payment methods requiring manual clicks or QR code scanning are cumbersome and pose safety risks while driving, making them entirely incompatible with the interaction rhythms of intelligent terminals.

For example, if a user says, "Order me a coffee," while in the car, expecting a payment page to pop up for manual password entry is impractical—the market urgently needs payment forms better suited to intelligent terminals. Alipay's AI payment has already been integrated into intelligent devices such as Qianwen AI glasses, Rokid, and Future Intelligence AI earphones, as well as intelligent cockpits from Li Auto, Chery, Geely, and Dongfeng. WeChat Pay has also partnered with over 40 automotive companies, including SAIC, GAC, and Leapmotor, directly responding to this demand.

On the business side, the explosion in demand for digital services has fueled rapid growth in virtual transactions such as digital content licensing, computing services, and API calls, leading to an increase in micropayment scenarios like pay-per-use and volume-based billing. These scenarios are largely infeasible under traditional payment models—the settlement costs for transactions worth fractions of a cent can exceed the transaction value itself. In contrast, intelligent agent autonomous payments combined with micropayment infrastructure perfectly meet these high-frequency, low-value payment needs.

Alipay recognized the immense potential of B2B micropayments and was the first to launch Token Pay, a comprehensive token payment solution designed specifically for scenarios like token top-ups, membership subscriptions, and marketing for large model companies. It helps these companies address global user subscription needs and one-click in-app token top-ups, among other requirements. Alipay has already established deep collaborations with companies like MiniMax and StepFun.

Additionally, the current relatively accommodating regulatory environment provides a window of opportunity for companies to expand rapidly. China's version of a "regulatory sandbox"—the Financial Technology Innovation Regulatory Pilot—offers a trial-and-error space for innovative businesses like intelligent agent payments, allowing companies to explore scenarios and refine technologies within controlled boundaries. For these leading payment players, being the first to implement scenarios, accumulate data, and improve risk control means gaining a market head start by the time regulatory details are finalized. This "develop first, regulate later" industry path has already been validated during the mobile payment era and is now being replayed in the intelligent agent sector. However, it's worth noting that the prolonged absence of rules also introduces compliance uncertainties and other challenges that the industry must collectively address.

Obstacles

Behind the intensive positioning by major players, the entire payment system is grappling with structural challenges. A JD Technology executive pointed out at the seminar: "True agent autonomous payment is not just an upgraded version of fast payment but a fundamental shift in payment logic—from humans actively making payments to agents, as authorized entities, executing payments. This means moving from trusting the payee to constraining and trusting the payment behavior." This implies that many existing infrastructures are no longer suitable and that the barriers to implementing intelligent agent payments are far greater than imagined.

The most critical issue is trust. Zhu Lin, General Manager of AI Payments at Ant Group, bluntly stated, "The real contradiction today is not a lack of traffic or insufficient technology but the unsolved issue of transaction trust." Ant Group CEO Han Xinyi emphasized, "In the agent era, the logic of traffic will fade, and the logic of trust will rise. Whoever solves trust could dominate the agent ecosystem."

Specifically, trust issues manifest at three levels. The first is the failure of traditional identity authentication systems. The security logic of traditional payments relies on passwords, facial recognition, SMS verification codes, etc., to confirm "whether it's the user." The problem is that intelligent agents lack physical identities; they are merely strings of code running on servers or local devices, which can be updated, replaced, or even maliciously hijacked without the user's knowledge. Therefore, when an agent initiates a payment, the system must not only confirm "whether the money belongs to the user" but also "whether this agent is the one authorized by the user." Has it overstepped its authority? Has it been compromised?

The second challenge is the ambiguity of liability attribution, as evident from several recent risk incidents. In April, a construction company executive in Guangzhou asked an AI to purchase group accident insurance for workers, but the AI pushed a private payment code as the "official payment portal," resulting in the loss of 1,618 yuan. Similarly, a Washington Post journalist testing OpenAI's agent found that the agent completed a checkout without user verification. These cases highlight a common issue: when AI bypasses confirmation and executes actions directly, liability boundaries become blurred.

The third challenge is the lag in security and regulatory frameworks. Intelligent agents are vulnerable to novel attacks such as prompt injection, context pollution, and model poisoning. In such cases, attackers don't need to breach user accounts; obtaining restricted tokens or poisoning input chains could enable agents to transfer funds while appearing compliant at the credential level. Zhu Min, former Vice Governor of the People's Bank of China, pointed out at the 2026 Tsinghua PBCSF Global Finance Forum that the past three months have seen the biggest shift in the global financial industry: the integration of payment services and financial intelligent agents. While this enhances efficiency, it also accelerates the speed, scale, and cross-border contagion of financial risks. As Zhu warned, "If speed risk and scale risk occur, it will be a tsunami."

Given this, trust is becoming the linchpin of industry standard-building: only by reconstructing the trust logic in the intelligent agent era and resolving trust issues between humans and agents and among agents themselves can intelligent agent payments truly take off. This is precisely what major platforms are working on, albeit with different approaches.

JD.com’s A2P2 framework introduces the ARI (Agent Runtime Identity) mechanism, which dynamically binds three critical elements during payment processing: the actual user, the agent’s identity, and the agent’s runtime environment. A product manager for JD.com’s A2P2 protocol compared this to "issuing each agent an ID card with an embedded chip. Payment authorization now requires not only facial recognition but also verification of the physical environment and the specific action commands—only when all three elements align is the transaction approved."

Meanwhile, the A2P2 protocol systematically dissects the ambiguous notion of "trust" in intelligent agent payments into a four-tier, engineering-oriented architecture that is verifiable and auditable. Each tier addresses a core challenge: the intent layer ensures "whether the AI comprehends the task," the identity layer confirms "who is initiating the payment," the decision layer evaluates "whether the payment should proceed," and the payment settlement layer, combined with an evidence chain, tracks "how payments can be audited post-transaction." Together, these layers form a complete trust closed loop.

Alipay, in contrast, places ultimate control in the user’s hands. It emphasizes that "Abao" serves solely as a user assistance tool without direct access to funds. The AI executes only actions explicitly approved by the user, and any fund transfers or payment steps require explicit user confirmation. Fund management permissions remain exclusively with the user at all times. The newly launched AI wallet not only manages funds but also oversees agent authorizations and permissions. Users can monitor and adjust "agent tasks" in real-time before, during, and after payment, with post-transaction queries available to ensure full transparency in intelligent consumption. Additionally, Alipay maintains its "you dare pay, I dare compensate" guarantee, further protecting users’ AI payment experiences.

However, while this user-centric approach ensures fund security, it limits the agent’s autonomy. Essentially, it remains at the stage of "AI-assisted order placement with final human approval," failing to achieve true autonomous agent payment.

A deeper challenge lies in protocol fragmentation. Today, major industry players are aggressively deploying agent payment solutions, but each operates in isolation. JD’s A2P2, UnionPay’s APOP, Alipay’s ACT 2.0, and WeChat Pay all have their own skill integration frameworks—each with distinct design philosophies, technical standards, and focal points, rendering them mutually incompatible. This results in agents on different platforms being unable to interconnect or interoperate, leading to redundant development of authorization, verification, and evidence storage mechanisms. This represents a significant efficiency loss for the entire industry, imposes high integration costs on developers, and hinders the achievement of economies of scale. A relevant executive from JD Technology acknowledged, "Agent payment is not a competition among individual enterprises but a collaborative ecological effort across the entire industry."

However, behind protocol standards lies the competition for commercial influence and industry discourse power. Reaching consensus among all stakeholders is no small feat.

Summary

In the mobile payment era, QR codes reshaped the structure of payment participants. Now, a new transformation is underway, but the emerging participants are no longer humans—they are vast numbers of autonomously operating agents.

The intense deployment by leading players at this juncture is not merely about capturing market share but also about vying for future rule-making and discourse power. Whoever can establish their protocol as the ecological standard will secure a structural position in the long-term future of hundreds of billions of agent-based transactions. This logic mirrors the past, where "whoever first built QR code infrastructure won the mobile payment era."

Of course, agent payments will not immediately replace QR code payments, but there is no doubt that they are carving out an entirely new track. And the battle over the rules governing "how agents spend money" has only just begun.

-

From Product-Driven to Tech-Empowered: The Second Growth Phase of Li Auto

-

![]()

Li Auto's Further Evolution: 'Full-Stack' as the Only Path to Surpass Tesla

-

![]()

Huawei and Cambricon Take the Lead as Chinese Chip Companies Step Up Efforts to Capture NVIDIA’s Market Share

-

![]()

Intelligent Agent Payment Landscape: Navigating Opportunities and Challenges in a Flourishing Market

-

![]()

Xiaomi and Others Boost Old Smartphone Battery Capacities, Power Banks Face Uncertain Future

-

![]()

Zhipu Soars to New Heights, MiniMax Faces Pressure: The Diverging Trajectories of the 'Dual Titans in Large Models'

-

AI Asset Spin-offs at Major Companies: Is Kling Paving the Way for ByteDance and Alibaba?

-

![]()

AI Agent Security Firm NewCore Raises $66 Million in Seed Funding, Achieves $300 Million Post-Money Valuation