Enflame Technology Clears IPO Hurdle: A Daring Venture into CUDA-Incompatible Realm

06/22 2026

06/22 2026

500

500

On June 15, 2026, Enflame Technology successfully navigated the review process for its Initial Public Offering (IPO) on the STAR Market, heralding the commencement of another grand spectacle of wealth creation. By this juncture, the top four domestic GPU manufacturers had all made their debut in the capital market.

In December of the preceding year, Moore Threads and MetaX Technologies both went public on the STAR Market, boasting market capitalizations that now exceed 300 billion yuan each. In January of the same year, Biren Technology made its public debut on the Hong Kong Stock Exchange, with a current market capitalization surpassing 120 billion yuan. These soaring valuations are underpinned by accelerating revenue growth, with the three listed companies reporting revenue increases of 243.37%, 121.26%, and 207.12% in 2025, respectively.

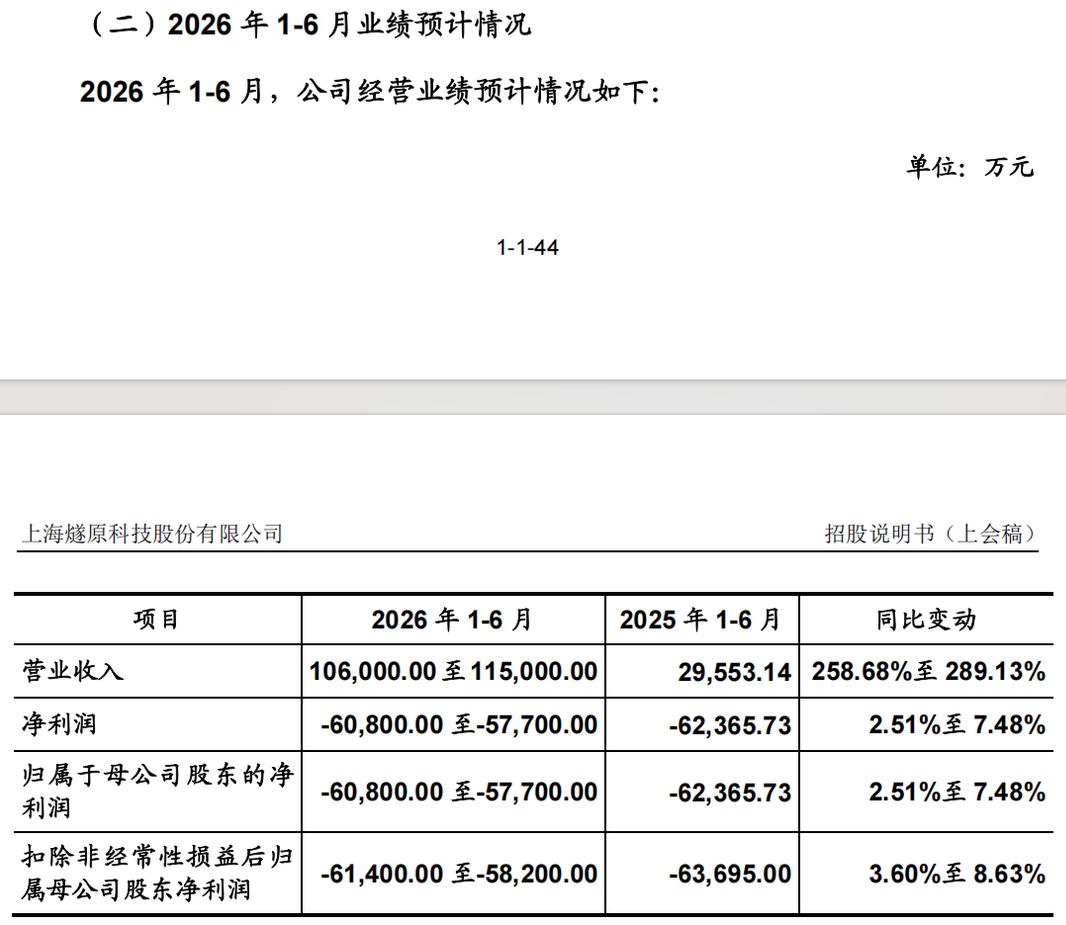

Enflame Technology is also experiencing robust revenue growth, with increases of 140% and 37% in 2024 and 2025, respectively, and an anticipated growth rate of 258.8% to 289.13% in the first half of 2026.

The crux of the difference lies in their technological approaches. Moore Threads, MetaX, and Biren all embrace a general-purpose GPU strategy, emphasizing compatibility and adaptation with the CUDA ecosystem. In contrast, Enflame insists on a Domain-Specific Architecture (DSA) paired with a self-developed software stack, rendering it incompatible with CUDA.

This technological divergence may well be the pivotal factor influencing the outcome of this wealth creation phenomenon.

The masterminds behind Enflame Technology are two seasoned veterans from AMD: Zhao Lidong and Zhang Yalin.

Zhao Lidong, a graduate of the EE85 class at Tsinghua University—often referred to as the "Whampoa Military Academy" of China's semiconductor industry—counts among his classmates the founders or leaders of companies such as GigaDevice, Maxscend, Will Semiconductor, and Yangtze Memory Storage, spanning fields like chips, sensors, and AI chips. Zhao spent over two decades in Silicon Valley, rising to the position of Senior Director of the Computing Division at AMD, where he oversaw the planning and execution of GPUs and AI acceleration chips.

Zhang Yalin, a graduate of the Department of Electronic Engineering at Fudan University, held positions as Senior Chip Manager and Technical Director of the China R&D Center at AMD. As one of the primary leaders in AMD's global chip R&D efforts, he successfully spearheaded the development and mass production of several key products.

When this former duo reunited to establish their venture in Shanghai in 2018, they were faced with three options: CPU, GPU, and AI. They ultimately chose AI. "The primary reason is that CPU and GPU technologies have been evolving for decades, with strong integration between their technical and industrial ecosystems and customers and original manufacturers, making it exceedingly difficult to disrupt this synergy," Zhao explained.

AI chips, however, presented a different landscape, with immense market potential and opportunities for cloud-based chips built on innovative architectures. Enflame chose AI and directly targeted the most challenging area: cloud-based AI training chips.

Enflame's product development has consistently progressed in this direction. Just 18 months after its inception, Enflame unveiled its first-generation cloud-based training chip, the Suisi 1.0, along with the Yunhui T10 training acceleration card, achieving successful first-pass silicon. In 2020, it launched its first-generation inference products, followed by second-generation training products in July 2021 and second-generation inference products in December of the same year.

By the end of 2025, Enflame had independently developed and iterated four generations of architectures and five cloud-based AI chips, establishing a comprehensive product ecosystem encompassing chips, acceleration cards, intelligent computing clusters, and software platforms.

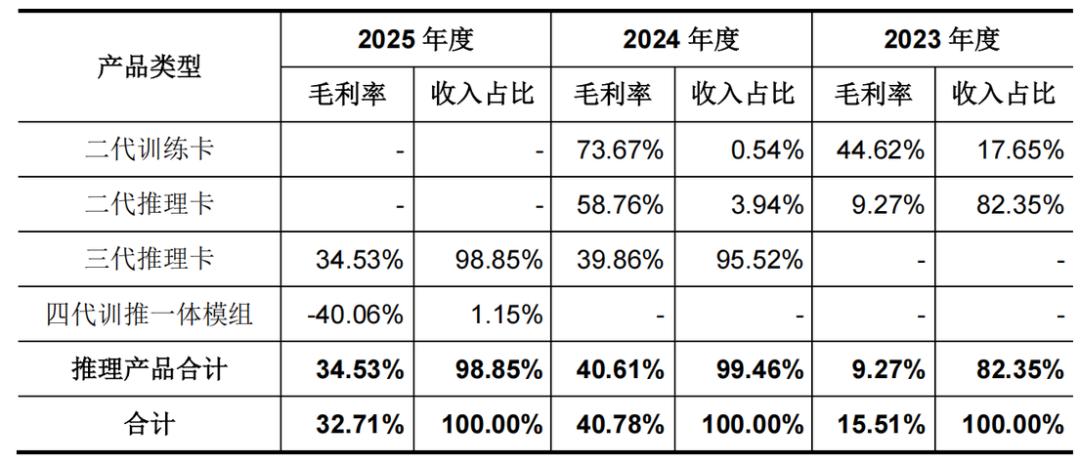

Enflame's revenue streams are derived from three main sources: AI acceleration cards and modules, intelligent computing systems and clusters, and IP licensing and other services.

Selling cards constitutes the primary revenue driver, with AI acceleration cards and modules contributing 856 million yuan in 2025, accounting for 86.83% of total revenue. While intelligent computing systems and clusters contributed 56% of revenue in 2024, their scale diminished by approximately two-thirds in 2025, with revenue accounting for only 13%. System-level solutions are still in their nascent stages.

The commercialization of AI acceleration cards and modules has not showcased Enflame's first-mover advantage in training but instead relies heavily on inference products.

The low proportion of training products is directly attributable to Enflame's chosen technological path.

Enflame employs a DSA architecture, which optimizes hardware for specific operations in AI computing, such as matrix multiplication and convolution. Unlike general-purpose GPUs that are compatible with the CUDA ecosystem and allow for seamless migration for customers, DSA architectures sacrifice versatility for higher energy efficiency and lower unit computing power costs.

This approach offers limited advantages in the training market but significant benefits in the inference market.

Training necessitates processing vast amounts of data, large-scale parallel computing, and extremely high cluster communication efficiency, demanding high versatility and ecological maturity—areas where NVIDIA's CUDA holds formidable barriers. Inference, however, involves single computations for specific business scenarios, with more fixed and fragmented tasks, prioritizing specialization and cost sensitivity over versatility.

As large models transition from training to large-scale deployment, demand for inference computing power continues to surge.

From 2023 to 2025, Enflame's revenue from AI acceleration cards and modules was 186 million yuan, 308 million yuan, and 856 million yuan, respectively, with growth rates of 65.6% and 178.5% in 2024 and 2025.

However, the drivers of growth differed. In 2024, Enflame released its third-generation inference chip, the Suisi S60, achieving a breakthrough in domestic 10,000-card inference clusters, with growth primarily driven by price increases. The average unit price of AI acceleration cards and modules rose by 60.8%, while in 2025, growth was driven by volume, with sales increasing by 197.8%.

In the first quarter of 2026, Enflame's growth momentum persisted, with revenue reaching 287 million yuan, a staggering 14.87-fold increase year-on-year.

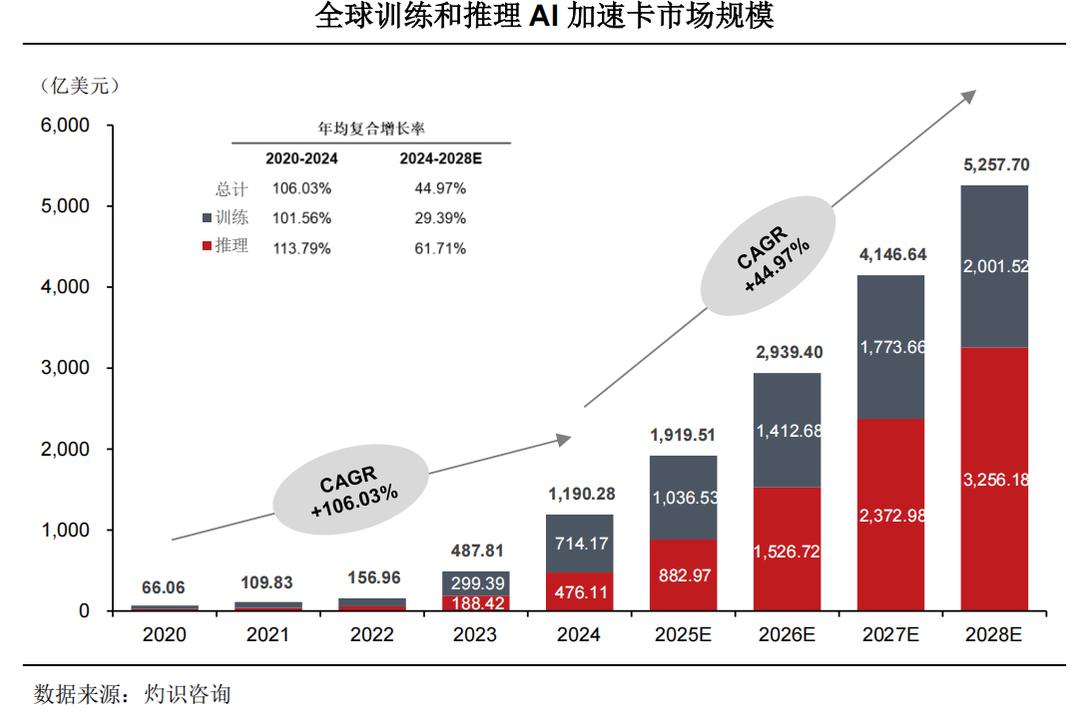

Looking ahead, China Insights Consultancy predicts that the global market size for inference demand in AI acceleration cards will grow from $47.611 billion in 2024 to $325.618 billion in 2028, with a compound annual growth rate of 61.71%. The domestic market is expected to reach 808.5 billion yuan, accounting for over 70% of the total market.

This suggests that the commercialization window for the DSA route remains wide open.

While the commercialization window is still ajar, Enflame faces the challenge of finding customers willing to pay, with Tencent undoubtedly being the most crucial one.

Data reveals that under the AVAP pricing model (where the company sells AI acceleration cards or modules to designated server manufacturers at prices agreed upon with internet clients), Enflame's revenue from sales to Tencent increased from 100 million yuan in 2023 to 270 million yuan in 2024 and further to 830 million yuan in 2025, accounting for 33.34%, 37.77%, and 83.8% of total revenue in the respective periods.

Tencent is not only Enflame's largest customer but also its major shareholder, with Tencent and its affiliates holding a combined 20.26% stake in Enflame.

It is evident that Enflame's transactions with Tencent have evolved from strategic cooperation to survival dependency.

In response, Enflame self-assesses: "The increasing proportion of sales to Tencent and its affiliates reflects the company's strategy of 'prioritizing single-point breakthroughs, subsequently expanding from point to line, and gradually from line to surface,' based on its development stage and limited resources. This approach is commercially reasonable."

The high revenue concentration on Tencent underscores the commercial realities of this technological path.

The DSA architecture paired with a self-developed software stack means Enflame's customer acquisition costs are higher than those of general-purpose GPU vendors. Even if the latter have not achieved customer diversification, Enflame's disadvantage in customer acquisition is more pronounced, making the rational commercial choice to concentrate resources on penetrating core customers.

Tencent has massive AI computing power demands, with products like Yuanbao, Hunyuan, WeChat AI, Tencent Meeting, and Enterprise WeChat all requiring significant token consumption, which in turn necessitates computing power and cost-per-token calculations. Tencent has the patience and resources to support a domestic chip supplier and the incentive to build a second computing power supply chain outside of NVIDIA.

This deep binding is a double-edged sword for Enflame.

On the positive side, it creates a moat through migration costs.

In its first-round inquiry response, Enflame mentioned that Tencent lacks the motivation and practical conditions to replace Enflame's products on a large scale with those from other suppliers at this stage. In other words, Enflame's software and hardware ecosystem is already deeply embedded in Tencent's AI infrastructure.

The "sunk costs" associated with this technological architecture and software adaptation make Tencent's continued procurement highly certain.

On the negative side, it erodes pricing power and introduces financial vulnerability.

The prospectus notes that, considering long-term strategic cooperation, Enflame supplies Tencent at unit prices lower than those offered to unrelated third parties.

Additional data from the second-round response provides context: In 2025, the gross margin for third-generation AI acceleration cards sold to Tencent was 33.95%, compared to 43.05% for third-generation AI acceleration cards sold to non-internet customer B (under a similar AVAP model) and 39.46% for third-generation acceleration cards sold to internet customer A (under the AVAP model, with Tencent as the end customer).

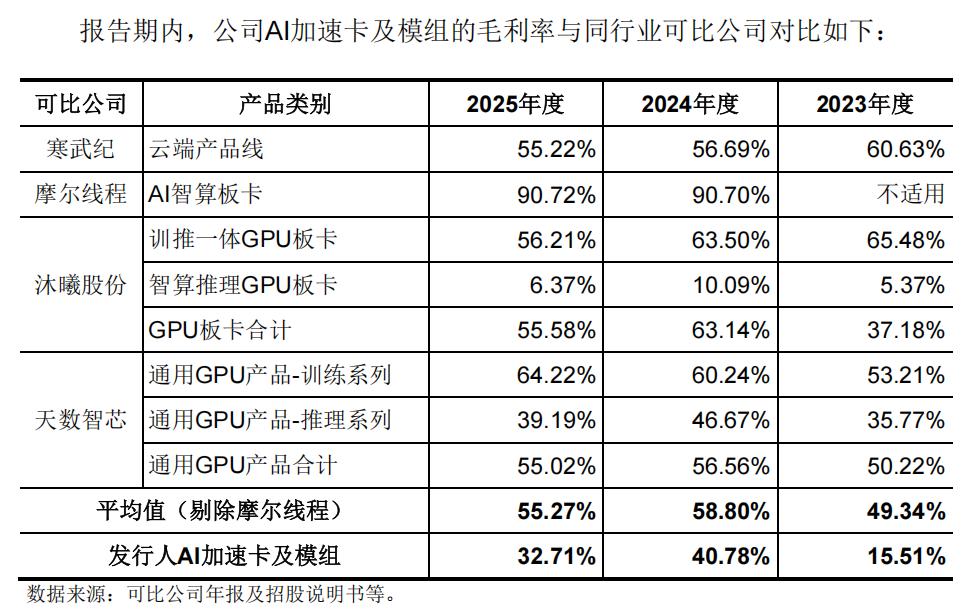

Coupled with the fact that inference cards have lower gross margins than training cards, and inference dominates Enflame's revenue, this results in Enflame's gross margin being significantly lower than the industry average.

Enflame expects to achieve profitability in 2026 or 2027, contingent upon both revenue attainment and gross margin improvements.

In terms of revenue, according to a Bernstein report, Tencent's demand for AI computing power continues to rise, with AI-related capital expenditures expected to reach $11 billion, $13 billion, and $14 billion in 2026-2028, respectively. Under demand pressure, Tencent's procurement from Enflame is unlikely to cease in the short term.

However, Enflame's top four customers outside of Tencent change frequently each year.

In 2026, the reality of expanding non-affiliated customers is that three potential internet customers "are expected to make small-scale deliveries by the end of 2026," and one non-internet customer "is expected to generate revenue within 2026." This indicates that Enflame has not yet established a stable customer base with repeat purchases, and the effect of expanding from point to line needs further enhancement.

In May 2026, at Tencent's shareholder meeting, Pony Ma commented that while the AI business has "boarded the ship," there is not enough seating, and the ship is not fast enough. This sentiment also applies to Enflame, which is "on the same ship" as Tencent but does not control its speed.

Binding with Tencent is the fulcrum for Enflame's survival. However, its true gamble extends far beyond a single customer's orders.

Enflame's choice of the DSA architecture is based on two considerations.

On the one hand, if it always remains compatible with CUDA, even with access to advanced manufacturing processes, it cannot catch up with NVIDIA in engineering implementation and system optimization capabilities within a short timeframe. Moreover, compatibility with CUDA would further strengthen the CUDA ecosystem, consigning Enflame to being forever in NVIDIA's shadow.

On the other hand, currently, Google, Microsoft, and Amazon all insist on developing AI chips with self-developed DSA architectures. In China, the major domestic manufacturers with high shipment volumes in 2025 all adopt DSA architectures.

This means that to achieve autonomous and controllable computing power, a fresh start is necessary. Enflame is betting that only through complete self-development can it gain a say in defining the next generation of AI computing power.

Thus, from chip and hardware technology to computing software and programming platform technology, and then to AI computing power cluster solutions, Enflame independently develops everything.

From 2023 to 2025, Enflame's cumulative R&D investment reached 3.676 billion yuan, 1.8 times its total revenue during the same period. With 643 R&D personnel accounting for 76.73% of its total workforce, the four generations of architectures and five chip models are all fruits of its R&D efforts.

Next, Enflame plans to invest the proceeds from its IPO in the R&D of fifth- and sixth-generation chips and software-hardware collaborative innovation projects, continuing to iterate its products and ecosystem.

Of course, starting anew comes with a cost: ecological isolation.

When you choose not to speak the industry's common language, you must have sufficient influence to make the market learn your language.

Within Tencent, Enflame's software and hardware are deeply embedded in core business lines like Yuanbao, forming a closed but active internal ecosystem. At this stage, the cost of ecological isolation is temporarily absorbed by the scale of the major customer. However, when Enflame attempts to promote its solutions to other manufacturers, they may not have Tencent's strategic patience, making each customer acquisition a tough battle.

A deeper risk comes from strategic changes at Tencent.

As previously noted, from the perspective of commercial rationality, Tencent lacks both the incentive and the circumstances to replace Enflame. Yet, commercial rationality and strategic rationality are not synonymous. Google developed its Tensor Processing Unit (TPU), and Meta ventured into custom Application-Specific Integrated Circuits (ASICs) — major tech platforms are increasingly eager to shape their own computing power futures. The possibility that Tencent might embark on a similar journey cannot be ruled out.

Even in the absence of a direct replacement, any shifts in the depth or priority of their cooperation could significantly alter Enflame's business landscape. Crucially, Enflame has no say in such strategic decisions.

Confronted with this structural vulnerability, Enflame finds itself with limited room for maneuver.

Between 2023 and 2025, Enflame incurred cumulative losses surpassing 4.3 billion yuan. For the first half of 2026, losses are projected to narrow slightly, falling within the range of 577 million yuan to 608 million yuan. The attainment of profitability hinges heavily on revenue growth and gross margin enhancements, as previously discussed.

Enflame also faces a market positioning conundrum. If perceived as a cornerstone of Tencent's computing power ecosystem, its valuation will be closely linked to Tencent's AI investment patterns, potentially appreciating in tandem with Tencent's AI capital expenditures. Conversely, if viewed as a high-risk entity with extreme customer concentration, its valuation may be marred by this single-point dependency.

-

![]()

Insta360’s Post-Lockup Period Begins: Employees Suspected of Selling Shares, Institutions Biding Their Time—Is a Major Storm on the Horizon?

-

![]()

Are Houses Getting 'ID Cards' Now? In the Future, House Decorating, Renting, and Buying Will All Be Possible with a Simple Scan!

-

![]()

Where Should the Senior Citizens in County Towns Go?

-

![]()

【OFweek Weike Cup】Santec Officially Enters for the 2026 Optical Industry Annual Innovation Product Award

-

![]()

Anhui’s Taihu County Establishes a Project with an Impressive Annual Production Capacity of 850 Million Square Meters of Optical Film, Along with Supporting Rollers!

-

![]()

The AI Unicorn Valued at 960 Billion is Raising Funds Again

-

![]()

Unveiling the Strategy: The RMB 11.5 Million Deal of MLOptics

-

![]()

Qingtian Lease Hits 7 Billion Valuation in Six Months, Coexistence of Robot Leasing Bubble and Reality