Four Seasons Information Technology Makes Another Bid for Hong Kong Stock Exchange Listing: Is the 'Leader' in Hong Kong's Fintech Sector Truly Robust?

07/08 2026

07/08 2026

337

337

Author: Beiduo

Source: Beiduo Business & Beiduo Finance

On July 5, Shenzhen Four Seasons Information Technology Co., Ltd. (hereinafter referred to as 'Four Seasons Information Technology', SZ: 300468) once again filed an application to list on the Main Board of the Hong Kong Stock Exchange. As reported by Beiduo Business & Beiduo Finance, this marks an updated attempt following the previous application's 'lapse' in December 2025.

Data from the Tianyancha App reveals that Four Seasons Information Technology, an A-share listed company, made its debut on the ChiNext board of the Shenzhen Stock Exchange on May 27, 2015. By July 7, 2026, the company's A-share price had closed at RMB 19.67 per share, with a market capitalization of approximately RMB 10.4 billion.

Notably, on July 3, 2026, the China Securities Regulatory Commission issued a notification regarding the overseas issuance and listing filing of Four Seasons Information Technology. According to the notification, the company intends to issue no more than 67.8052 million ordinary shares for overseas listing on the Hong Kong Stock Exchange.

Despite its glamorous title as the 'leader' in the fintech software development service market for the banking sector in Hong Kong, Four Seasons Information Technology faces several challenges, including declining revenue, increasing revenue without corresponding profitability growth, and a staggering 90%+ dependence on major customers.

According to the prospectus, Four Seasons Information Technology is a seasoned fintech service provider based in the Greater Bay Area. It primarily offers fintech software development, consulting, and system integration services to banks, regulatory authorities, and other financial institutions across Mainland China, Hong Kong, and Southeast Asia.

Data from CIC indicates that, by revenue, Four Seasons Information Technology ranked 17th in the fintech software development service market in Mainland China and Hong Kong in 2025. Among all players in the fintech software development service market for the banking sector in Hong Kong, it secured the top spot.

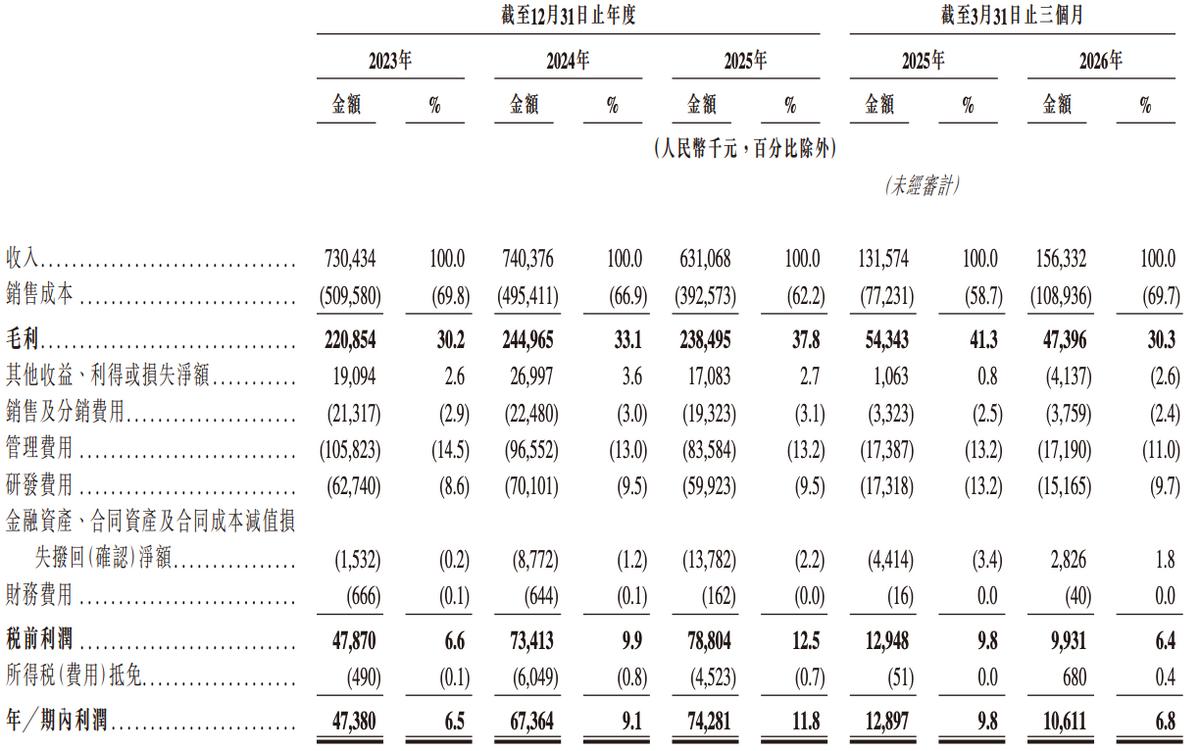

From a financial standpoint, the performance trend of Four Seasons Information Technology is concerning. In 2023, 2024, and 2025, the company reported revenues of RMB 730 million, RMB 740 million, and RMB 631 million, respectively. In 2025, revenue plummeted by approximately 14.8% year-on-year, following two years of hovering around RMB 700 million.

Contrary to the revenue decline, Four Seasons Information Technology's net profit has exhibited a consistent upward trend. During the same period, the company's net profit reached approximately RMB 47.38 million, RMB 67.364 million, and RMB 74.281 million, respectively, boasting a compound annual growth rate exceeding 20% over the three-year span.

In the first quarter of 2026, Four Seasons Information Technology's revenue surged to approximately RMB 156 million, marking an 18.82% year-on-year increase. However, its net profit dwindled to only RMB 10.606 million, a 17.76% year-on-year decrease, signaling a trend of 'increasing revenue without increased profitability'.

Another pressing concern for Four Seasons Information Technology is its extreme reliance on major customers.

In 2023, 2024, 2025, and the first quarter of 2026, revenue from the top five customers accounted for a staggering 90.1%, 93.7%, 89.1%, and 86.5%, respectively. Among them, revenue from the largest single customer constituted 41.1%, 42.4%, 52.7%, and 51.8%, respectively.

This implies that in 2025 and the first quarter of 2026, over 50% of Four Seasons Information Technology's revenue hinged on the same 'major sponsor', with the contribution ratio of a single customer far surpassing the industry average. The loss of major customers or a reduction in their demand would directly impact the company's performance.

Four Seasons Information Technology acknowledged in the prospectus, 'We rely on a limited number of customers, and a significant portion of our revenue comes from a few customers. If these major customers significantly reduce their demand for our services, our business and operating results may be materially and adversely affected.'

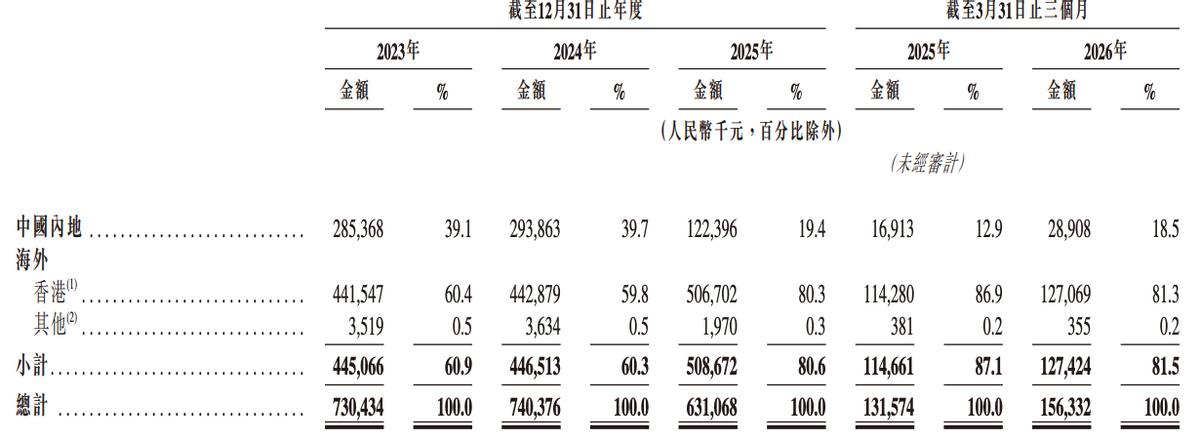

Simultaneously, over 80% of Four Seasons Information Technology's overseas revenue originates almost exclusively from Hong Kong, China. This highly concentrated revenue stream means the company's performance is susceptible to external factors such as exchange rate fluctuations and changes in Hong Kong's regulatory policies. Amidst ongoing geopolitical tensions, this risk exposure cannot be overlooked.

Furthermore, Four Seasons Information Technology has distributed cash dividends multiple times. According to the prospectus, the company declared dividends of RMB 31.8 million, RMB 31.8 million, and RMB 53.1 million in 2023, 2024, and 2025, respectively, effectively 'devouring' the profits of the past few years.

At the corporate governance level, Four Seasons Information Technology has also crossed red lines. In September 2024, due to illegal share reductions, the Shenzhen Stock Exchange took regulatory action against the relevant parties. The company's net cash flow from operating activities in the first three quarters of 2024 was -RMB 50.5195 million, a year-on-year decrease exceeding 80%, indicating a troubling cash flow situation.

Currently, Four Seasons Information Technology's second attempt to list on the Hong Kong Stock Exchange is driven by both financing needs and strategic considerations amid A-share valuation pressures. The allure of being the 'leader' in Hong Kong's fintech sector, coupled with its technological布局 (layout) in AI + blockchain, renders the company somewhat appealing in the capital market.

However, multiple concerns, such as three consecutive years of declining revenue, over 90% of revenue tied to major customers, high accounts receivable, and deteriorating cash flow, pose a 'ceiling' on the company's growth potential. Especially under the pricing system dominated by institutional investors in the Hong Kong stock market, whether Four Seasons Information Technology can maintain its high valuation logic from the A-share market remains a significant question mark.

Whether this Hong Kong listing attempt represents a breakthrough move or a 'last resort' will unfold over time.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry