When Large Model Companies Start Making Smartphones

07/15 2026

07/15 2026

332

332

Author | Wen Yehao

Editor | Wang Pan

Amidst the bustling domestic AI landscape, Jieyue Xingchen has maintained a relatively low profile. However, with the first batch of restricted shares from companies like Zhipu and MiniMax becoming tradable, and Moonshot AI securing successive funding rounds with a valuation nearing $30 billion, this self-proclaimed 'still waters run deep' company seems to be unable to contain its ambitions.

On July 13th, Jieyue Xingchen played three cards at once: the large model-native AI terminal brand STEPX, the intelligent agent-native operating system Step AOS, and the personal intelligent agent Jieyue Amoo.

As the inaugural product under the STEPX brand, the world's first large model-native intelligent agent smartphone, STEPX Neo, equipped with Step AOS and featuring the built-in Amoo agent, made its debut. This move also seemed to steal the spotlight from Nubia.

This launch event also signified Jieyue's shift after exploring B-end commercialization for quite some time, as it personally pushed open another door. On the other side of that door lies the smartphone market, a fiercely competitive arena where Apple, Samsung, Huawei, Xiaomi, OPPO, and Vivo have been battling for over a decade.

Knowingly heading into the lion's den, this move represents another 'leap' for Jieyue and a crucial gamble by a large model startup under narrative pressure, betting heavily on the future.

Retreating to defend its B-end foothold while advancing to compete for the right to define the next generation of terminals, the stakes on both ends of this gamble are vastly different.

A Gentle Disruption

Among domestic large model companies, Jieyue is the first to venture into creating its own branded smartphones.

Why choose smartphones as the intelligent agent terminal? Yin Qi, Chairman of Jieyue Xingchen, outlined three criteria: high-frequency interaction, the presence of a screen, and sufficiently strong on-device computing power. By these standards, smartphones emerge as the only optimal solution at present.

Naming their first product Neo also carries several layers of meaning—on the surface, it signifies 'newborn,' while subtly referencing Neo, the protagonist from 'The Matrix,' and also serving as a reimagined spelling of 'One.' This pragmatic choice, paired with a sufficiently 'sexy' name, reveals Jieyue's clear stance: to enter from the most mature terminal segment but aim far beyond just creating another smartphone.

Although both fall under the broader category of AI smartphones, STEPX Neo and most AI smartphones on the market follow different paths.

The 'intelligence' of most AI smartphones on the market essentially represents the superposition of AI-related functions, such as AI photo editing and AI call summarization. These functional modules are mostly embedded within existing smartphone OSes without altering the underlying interaction logic. In contrast, AI intelligent agent smartphones attempt to reconstruct the phone's interaction paradigm using intelligent agents.

From Jieyue's perspective, the Step series model matrix and the Step AOS intelligent agent-native system essentially form the foundation for this new paradigm—where the large model serves as the agent's 'brain,' Step AOS as its operating environment, and AI-native terminals as the carrier (carrier) for intelligent agents to enter the physical world.

However, when discussing this AI-native terminal, Yin Qi's wording was quite precise and restrained, describing the STEPX Neo as 'making an appearance' rather than 'being released.'

This implies that STEPX Neo is not a product immediately available for purchase.

Judging from the images and videos released during the event, STEPX Neo's appearance has two intuitive features: a nearly square secondary screen on the back and a dual-camera setup. However, specific details such as hardware specifications, pricing range, and release date still await further disclosure.

In response, Yin Qi revealed in a post-event dialogue that STEPX Neo is 'ready' at the hardware level. Furthermore, passing the L3-level test in the 'Classification of Intelligent Terminals for Artificial Intelligence' indirectly confirms that its system and hardware foundations are functional.

If both the hardware and system foundations are in place, why only 'make an appearance' and not officially release it? The answer likely lies in ecological considerations.

During the event, Yin Qi stated that the intelligent agent ecosystem needs to undergo a 'co-creation and nurturing period' and specifically emphasized that the notion 'Apps will disappear in the agent era, and the two are mutually exclusive' is grossly mistaken.

This critique is partly an industry judgment and partly reflects Jieyue's own stance.

After all, from a startup's perspective, now is far from the time to shout 'disruption.' Without an established ecosystem, pushing all super Apps to the opposite side would be self-defeating. In contrast, the stance of 'coexistence' seems more like a proactive call for peace. Whether major players heed this olive branch is another matter.

Judging from the list of initial partners announced at the event, Jieyue's current intelligent agent ecosystem is still in its early stages, with a relatively gentle approach to collaboration that does not follow the more aggressive GUI Agent route. Although Baidu, Meituan, JD.com, Weibo, AutoNavi, and CapCut are all on the list, it is evident that ByteDance and Alibaba Group apps lean more towards utilitarian functions, while national-level super Apps remain to be fully integrated.

Notably, there is the matter of Tencent's attitude.

As an existing shareholder of Jieyue, Tencent has collaborated extensively with Jieyue in the automotive sector, integrating music, video, maps, payments, and other sectors to create an AI cockpit intelligent agent. However, on the smartphone front, Tencent's presence is almost negligible.

Jieyue stated that it has had in-depth discussions with Tencent and looks forward to future opportunities for deep cooperation with the Tencent ecosystem.

However, this contrast inevitably leads to speculation about Tencent's current ecological Layout (layout) for WeChat A2A. In the automotive scenario, where Tencent lacks a system-level entry point, cooperation with Jieyue is mutually beneficial. In the smartphone scenario, where WeChat itself is the dominant entry point and is exploring the integration of intelligent agents with terminals and mini-programs, its stance naturally differs.

Ultimately, Jieyue's journey into terminals begins with considerable complexity, including technical risks, ecological barriers, and competitive pressures, none of which can be underestimated. Yet, knowing the immense hardware challenges, why does Jieyue persist? The answer may lie in Jieyue's—and Yin Qi's—past experiences.

Tearing Down Old Walls

Jieyue is no stranger to terminals.

As an early domestic player in multimodal large models, Jieyue's Step models have always excelled in multimodal capabilities. In the early days of AI smartphones, when manufacturers generally lacked such capabilities, Jieyue naturally became a quick solution to fill the gap.

Thus, even before unveiling its own terminal brand, Jieyue had already been quietly operating in the smartphone industry for over a year, serving as an AI supplier hidden behind the AI applications of various smartphone manufacturers.

It is reported that by the end of 2025, Jieyue Xingchen had covered approximately 60% of domestic leading smartphone brands, with its models installed on over 42 million devices and serving nearly 20 million users daily.

However, this path may not be sustainable in the long run.

Take its collaboration with OPPO as an example: functions like 'One-Touch Screen Query' and 'One-Touch Omnisearch' on the OPPO Find X8 series are powered by Jieyue's capabilities.

However, these functions are all accessed through the Xiao Bu Assistant, leaving users perceiving OPPO's AI capabilities while Jieyue's models remain hidden in the background. The division of labor is clear, as are the boundaries—Jieyue acts as the supplier, OPPO as the brand owner, and the core entry point remains firmly in the latter's hands.

After all, no player is willing to let an external large model vendor position itself between their products and users.

The system ecosystems, user data, and brand recognition that smartphone manufacturers have spent over a decade building determine that they cannot hand over a system-level entry point like AI to any third-party vendor. The better third-party models perform, the deeper their AI capabilities penetrate, and the more reliant users become, the greater the sense of crisis among smartphone manufacturers.

Thus, it can be seen that Vivo has Blue Heart, OPPO has Andes, and Xiaomi has MiMo. Among leading smartphone manufacturers, almost none refrain from developing their own large models. No matter how high the parameters or strong the benchmark scores of third-party models, they can only serve as supplements—not that they can't be used, but they dare not rely on them.

In other words, from the outset, the domestic smartphone industry may have had no ecological niche for third-party large model companies.

This is the wall that stands before all large model startups.

Yin Qi has not remained oblivious to this wall.

Those who have experience in B-end businesses often approach subsequent entrepreneurial ventures with caution and a desire to maintain distance. During his time at Megvii, Yin Qi led CV technology from government (G) to business (B) and then to consumer (C) applications, constantly searching for suitable scenarios but never managing to establish a self-sustaining commercial closed loop (loop). He understands better than most the frustration of holding top-tier technology while searching the world for a 'nail' to hammer it in.

This means that the C-end path he did not complete at Megvii must now be revisited at Jieyue.

Thus, Yin Qi, stepping from behind the scenes onto the front stage, has prescribed a solution for Jieyue that reflects his personal style. With the C-end as the ultimate goal, if clients cannot provide sufficiently large scenarios, then create one yourself; if smartphone manufacturers refuse to fully open their systems, then build your own terminal.

At the event, Yin Qi also admitted that he had hesitated for a long time over whether to personally venture into terminal manufacturing. Friends in the hardware industry advised him against it, but he ultimately decided to proceed—not out of ignorance of the challenges but because the alternative, remaining stagnant, was even less acceptable. Rather than waiting for the industry to slowly reach a consensus, he chose to create a sample himself, showing everyone what an AI-native terminal should look like.

Thus, this move resembles less of an offensive and more of a strategic breakthrough. Faced with an impenetrable B-end wall, the alternative is to bypass it by creating products and hardware that they can control. Of course, if this path succeeds, Jieyue is also willing to open its capabilities to other manufacturers.

However, the challenges of the hardware path are even greater than those of B-end cooperation. Stepping from behind the scenes onto the front stage means that former partners may become potential competitors; it requires building an entire set of capabilities, including branding, channels, supply chain, and after-sales service; and it means charging into a fiercely competitive market where battles have raged for over a decade.

These issues seem difficult for Jieyue to resolve alone.

A Gamble on Half the Industry Chain

Large model companies are not the first to push into terminals; ByteDance was the previous player to wade into these waters.

Late last year, ByteDance partnered with Nubia to launch the Doubao smartphone, setting an example for deep cooperation between 'large model vendors + smartphone manufacturers.' However, the fact that even a player of ByteDance's scale chose a collaborative approach and explicitly stated it would not develop its own smartphones also underscores the complexity of the consumer electronics market—technical leadership alone may not suffice.

Royole serves as a cautionary tale. Despite possessing cutting-edge flexible screen technology, rivaling today's large models in scarcity, its decision to manufacture smartphones ultimately led to burning through billions and bankruptcy.

Jieyue, however, remains undeterred. Much of this confidence stems from its allies.

Strictly speaking, ByteDance lacks true allies in the smartphone battleground. Although Nubia had previously expressed full support for the Doubao smartphone, the collaboration was essentially transactional, with both sides keeping their options open—ByteDance engaged with multiple manufacturers simultaneously, while Nubia's parent company, ZTE, hedged its bets between ByteDance and Jieyue.

Royole's investors were almost entirely financial in nature, offering capital but nothing else—supply chain, channels, and clients all had to be built from scratch.

Jieyue's situation is entirely different.

In its Series B+ funding round earlier this year, ODM giant Huaqin appeared as an industrial investor. In a subsequent funding round, Jieyue's roster of industrial allies expanded further, including Longcheer Technology, OmniVision Group, and ZTE Corporation—all players within the smartphone industry chain, upstream and downstream.

Among them, Longcheer and Huaqin are both ODM manufacturers, OmniVision is a major image sensor producer, and ZTE has long been active in the terminal sector, with operator channels and terminal engineering experience.

Thus, this has never been a solo fight for Jieyue. From the moment it ventured into AI terminals, Jieyue has rallied a significant portion of the industry chain behind it. With this 'Avengers Alliance' assembled, building an AI-native smartphone likely faces few supply chain obstacles.

In other words, while the Doubao smartphone represents horizontal collaboration between large model vendors and traditional smartphone brands, Jieyue embodies vertical alignment between large model vendors and the smartphone supply chain.

The collective bet by upstream manufacturers on Jieyue is also a noteworthy development.

Despite their immense scale, in the traditional smartphone food chain, these players are hardly top predators. Huaqin and Longcheer ship vast quantities annually but maintain consistently low net profit margins. OmniVision has a solid business but remains overshadowed by Sony and Samsung. ZTE's terminal business, despite years of cultivation, has seen its Nubia and Red Magic brands remain niche.

In a mature industrial landscape, breaking through to the next level is an uphill battle.

The AI terminal wave, however, has become a fulcrum for leveraging change—if intelligent agents can become the core competitiveness of the next generation of smartphones, then the party controlling the intelligent agent technology closed loop (loop) will hold the discourse power (say) in redistributing industry chain value.

Jieyue holds precisely this card.

In other words, it is not just Jieyue that wants to make smartphones; the entire upstream industry chain seeks to ride the AI terminal wave to reach higher value ground.

The question remains whether these industrial capital investments stem from genuine belief in intelligent agent smartphones becoming the next mainstream terminals or from the need for a fresh narrative.

The answer likely lies in both.

If intelligent agent terminals can truly redefine terminal industry value distribution, the long-term value speaks for itself. Even if the outcome falls short of expectations, at least it provides a compelling story and a fulcrum for value reassessment—crucial for both upstream giants facing market cap pressures and Jieyue, which has dismantled its red chip structure and aspires to an IPO.

Whether Jieyue will become the definer of the 'AI intelligent agent smartphone' era or simply be swept up in the AI terminal tide, ultimately fading into obscurity, depends on its ability to establish new rules of the game alongside its industrial allies.

-

AI's Richest Person Revealed: A Native of Zhanjiang!

-

Standing at a Distance, Behind Xiaomi's Phone Slowdown and Layoffs", "Xiaomi Phone, Declining Sales, Offline Stores, Product Strategy, Comprehensive Ecosystem of People, Vehicles, and Homes", "Accordi

-

![]()

ByteDance Enters Physical AI, Igniting the Second Wave of 'Feast'?

-

![]()

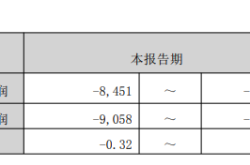

Phoenix Optics Forecasts a Nearly 70% Drop in First-Half Net Profit, Yet Optical Business Profit Shows Growth!

-

![]()

A Staggering 50.16% Reduction in Losses Projected! COST's Interim Report Signals a Pivotal Moment

-

![]()

Nearly 19% of National Total! Guangdong Boasts 164 Registered Large Models as New AI Personification Regulations Take Effect

-

![]()

BYD’s Baosha, Sought After by Australians, Makes a Triumphant Return to China

-

【Focus】Analysis of Downstream Demand Sectors and Key Enterprise Development for Acrylic OCA Optical Adhesives in China by 2026