DeepSeek Rushes Towards IPO, Valuations of the 'AI Four Little Titans' to Be Recalculated

07/15 2026

07/15 2026

492

492

Bloomberg reported that DeepSeek has commenced preparations for an IPO, with the aim of submitting its listing application as early as 2026 and targeting the domestic capital market for a listing in 2027. As of now, the company has not officially submitted its application or announced a definitive listing plan.

In May of this year, DeepSeek completed its first external financing since its inception, raising approximately $7 billion with a post-money valuation of about $52 billion.

Just one month later, the market began to circulate news of its negotiations with potential investors for a new round of financing, with the proposed pre-money valuation raised to $71 billion.

This company, once known for 'being backed by High-Flyer Quantitative, having sufficient self-funded capital, and long refusing external financing,' is now reversing course by continuously raising funds and swiftly advancing towards the capital market. This shift also raises three core questions that permeate the industry:

Why does DeepSeek suddenly require massive amounts of capital?

How will its path to capitalization rewrite the competitive fates of the 'AI Four Little Titans'—Zhipu, MiniMax, Kimi, and StepFun?

Will DeepSeek's entry elevate the valuation ceiling for Chinese AI or puncture the current valuation bubble in the large model sector?

This marks the first large-scale opening of financing doors for DeepSeek in its three years of existence.

The initial $7 billion funding round far exceeds the single-round financing volumes of most AI startups.

Notably, founder Liang Wenfeng reportedly invested approximately RMB 20 billion himself, making him the largest single contributor in this round. Industrial capital from Tencent, CATL, JD.com, NetEase, and others participated in the investment, with the National Artificial Intelligence Industry Investment Fund also becoming a minority shareholder.

This implies that this round of financing was not about the founder cashing out but rather about introducing long-term industrial and national capital to build a more stable capital and resource base for the company.

The rapid initiation of the next round of financing before the first has been fully digested reflects a shift in DeepSeek's competitive logic, with capital needs concentrated in four directions:

First, competition in cutting-edge models has shifted towards large-scale Agent operation scenarios, with overall computing power consumption rising instead of falling.

Second, the construction of its own data centers is now on the agenda.

According to the Financial Times, the new round of financing is directly related to DeepSeek's expansion of capital expenditures, focusing on building its own data centers and bulk purchasing AI chips.

Third, the deployment of self-developed inference chips has begun.

The market has repeatedly reported that DeepSeek is developing AI chips tailored for inference scenarios, aiming to reduce reliance on overseas and third-party chips.

This signifies that DeepSeek is evolving from a pure model lab into a systems-level company encompassing 'models + computing power + chips,' but it also implies longer R&D cycles, higher upfront investments, tape-out risks, and supply chain costs.

Fourth, comprehensive expansion of teams and commercialization systems.

DeepSeek has publicly stated its plan to at least double the size of its staff across all departments.

The organizational model previously driven by small teams and research is now expanding towards a more complete R&D, product, commercialization, and listing governance system.

Overall, DeepSeek has entered a new phase of full-stack AI infrastructure competition, facing an altered cost structure and naturally higher demand for large-scale funding.

The most direct impact of DeepSeek's entry into the IPO queue will be a complete rewrite of the capitalization narrative in China's large model industry, with the 'AI Four Little Titans' bearing the brunt.

Previously, Zhipu and MiniMax enjoyed a premium as 'scarce targets among the first large models to go public,' while Kimi and StepFun vied for the position of the 'third large model stock.'

With DeepSeek, a universally recognized technical leader, entering the field, the market's core question will immediately shift to: What justifies the current valuations of other companies besides DeepSeek?

Zhipu: Short-term Momentum, Long-term Valuation Scrutiny

In the short term, DeepSeek's preparation for listing may benefit Zhipu.

Both companies develop general-purpose foundational models, emphasize code, Agents, enterprise APIs, and open-source ecosystems, and are seen as China's core contenders against OpenAI.

With DeepSeek not yet on the secondary market and lacking direct trading targets, Zhipu, which has already listed on the Hong Kong Stock Exchange and has a business structure closest to DeepSeek, may well become a proxy trading entry point.

However, in the long run, Zhipu is also the most vulnerable to DeepSeek's impact.

After Zhipu's listing on the Hong Kong Stock Exchange in January 2026, its share price briefly reached HK$2,980 on June 22, approximately 25.6 times the issue price, with a total market capitalization exceeding HK$1 trillion (about $128 billion).

Based on its audited revenue of RMB 724 million in 2025, the static price-to-sales ratio exceeds 1200 times.

Although private valuations and secondary market valuations are not entirely comparable, DeepSeek's proposed pre-money valuation of only $71 billion in its new round raises a sharp market question:

Why is DeepSeek, with stronger global technical influence and open-source branding, valued lower in private markets than Zhipu's secondary market valuation?

Once DeepSeek officially submits its application and discloses its prospectus, investors will, for the first time, have complete financial and operational data for horizontal comparison.

If DeepSeek demonstrates larger revenue, lower costs, and stronger technical influence but an IPO valuation lower than Zhipu's, Zhipu's scarcity premium may be compressed.

Conversely, if DeepSeek ultimately goes public at a higher valuation, it could raise Zhipu's valuation ceiling.

Therefore, Zhipu is likely to benefit the most from DeepSeek's IPO expectations in the short term but is also the most susceptible to DeepSeek's revaluation in the long term.

MiniMax: Niche Competition Remains, Commercialization Scrutiny Intensifies

MiniMax faces relatively less direct impact because it is not an identical investment target to DeepSeek.

DeepSeek leans more toward foundational models, open-source ecosystems, code capabilities, and developer platforms;

MiniMax, on the other hand, owns consumer products like Talkie, Hailuo AI, and voice and video generation tools. In 2025, over 70% of MiniMax's revenue came from overseas markets.

It can perfectly pitch itself to investors as follows: Investing in DeepSeek means investing in China's leading foundational model company, while investing in MiniMax means investing in a global AI-native application platform.

However, DeepSeek's capitalization moves will still indirectly raise market expectations for MiniMax.

In July of this year, MiniMax announced plans to raise approximately $2.05 billion through a share placement and convertible bond issuance, with funds earmarked for R&D, commercialization, working capital, and general corporate purposes.

Following the announcement, its share price fell about 12%, reflecting market concerns over potential dilution and subsequent capital expenditures.

This indicates that capital market expectations for large model companies have shifted.

In the past, as long as model capabilities improved, user bases grew, and products entered overseas markets, companies could expect valuation rewards.

Now, investors also ask whether revenue can cover model R&D expenses, whether customer acquisition costs can decline, and whether gross margins can continue to improve.

Kimi: Valuation Ceiling and Benchmark

For Kimi, DeepSeek's listing could both expand its valuation space and expose its valuation shortcomings.

According to media reports, Kimi is in the preparatory stages for a Hong Kong Stock Exchange IPO, having completed approximately $2 billion in financing in May 2026 with a post-money valuation exceeding $20 billion. Its annual recurring revenue (ARR) reportedly exceeded $200 million in April of the same year.

On one hand, DeepSeek's high valuation sets a new ceiling for the industry.

If DeepSeek ultimately goes public with a valuation exceeding $100 billion, even if Kimi secures only 30%-40% of DeepSeek's valuation multiple, it could still support a market capitalization of $30 billion-$40 billion, leaving room for growth compared to its current private market valuation.

On the other hand, pressure is equally real.

Investors will not simply apply a proportional discount but will instead ask tougher questions, such as:

Why does Kimi's foundational model capability justify 30%-40% of DeepSeek's valuation? Can user numbers stably convert into subscription revenue? Can Agent products effectively boost average revenue per user (ARPU)? Is the commercial value of consumer entry points truly higher than that of open-source model ecosystems?

For Kimi, the most rational choice is to actively differentiate itself from DeepSeek.

By positioning itself as the strongest consumer AI entry point, Agent, and productivity platform—rather than being viewed as a 'mini DeepSeek' by investors—Kimi is more likely to secure additional application-layer premiums.

StepFun: Most Direct Impact, Dual Pressure on Positioning and Timing

Among the 'AI Four Little Titans,' StepFun may be the unlisted company most severely impacted by DeepSeek's IPO.

Previously, market rumors suggested that StepFun had completed shareholding system reform, dismantled its offshore structure, and was preparing for a Hong Kong Stock Exchange IPO with a target valuation of about $10 billion.

However, its core dilemma lies in its ambiguous identity:

It competes directly with DeepSeek in foundational models and Agents but lacks DeepSeek's technical brand strength; its C-end product recognition lags behind Kimi; its secondary market influence is inferior to Zhipu; and its overseas application revenue trails MiniMax.

With DeepSeek joining the IPO race, investors' questions will be exceptionally direct:

Where exactly is StepFun's model leadership advantage? If it cannot achieve first-place model capability, why maintain full-scale R&D investments in foundational models? Are its collaborations with OPPO, Geely, and other firms definitive revenue orders, or do they remain at the ecosystem cooperation level?

DeepSeek has also disrupted StepFun's original listing timeline.

StepFun could have go with the flow gone public as the 'third large model stock' after Zhipu and MiniMax, but this narrative has now lost its appeal.

StepFun faces a dilemma:

Rushing to list before DeepSeek may expose immature financial data and business models;

Waiting to list after DeepSeek may see its valuation fully anchored by DeepSeek's prospectus, severely narrowing its bargaining space.

After DeepSeek enters the capital market, its most profound impact may be that China's large model industry, for the first time, gains a domestic valuation benchmark.

Previously, investors priced Chinese large model companies by referencing overseas firms like OpenAI and Anthropic, then applying varying discounts based on China's market environment, regulatory constraints, internationalization level, and user payment capacity.

This valuation method was highly narrative- and sentiment-driven, with significant volatility.

After DeepSeek's listing, the situation will change.

DeepSeek operates in a similar market environment to Zhipu, MiniMax, Kimi, and StepFun, facing comparable chip restrictions, talent costs, regulatory frameworks, and user payment levels while possessing internationally recognized technical influence.

Once financial data becomes public, investors can directly calculate: How many DeepSeeks is Zhipu worth? What fraction of DeepSeek is Kimi worth? Can MiniMax's application business secure additional premiums beyond model value?

China's large model valuation system will officially shift from discounting relative to OpenAI to discounting relative to DeepSeek.

In the long run, this differentiation will become even harsher.

Companies with weaker technical capabilities than DeepSeek, slower revenue growth than expected, lower gross margins, faster cash burn, and valuations approaching or exceeding DeepSeek's will all face valuation compression.

This is not a simple across-the-board rise or fall but rather an initial lifting of the industry's valuation ceiling followed by a squeezing out of scarcity premiums lacking fundamental support.

Currently, market rumors widely suggest that DeepSeek is targeting the domestic capital market. If it ultimately chooses to list on the A-share market, DeepSeek will become the purest foundational model target on the A-shares.

It will not only price model companies but may also gradually become a key entry point for public funds and index funds to allocate to China's AI sector. It could even serve as a valuation anchor for the entire AI industry chain, including domestic computing power, self-developed chips, and data centers.

However, it is worth noting that the total market capital is not infinite. DeepSeek's large-scale fundraising may siphon capital from other AI companies, increasing IPO pricing and issuance difficulties for smaller AI firms.

Thus, DeepSeek's IPO will fundamentally alter not just its own equity structure but the entire evaluation system of China's AI industry.

All companies must now prove their technical strength, revenue quality, cost control, and capital efficiency.

From this point onward, the competition among China's large models has officially entered the balance sheet of each company.

-

AI's Richest Person Revealed: A Native of Zhanjiang!

-

Standing at a Distance, Behind Xiaomi's Phone Slowdown and Layoffs", "Xiaomi Phone, Declining Sales, Offline Stores, Product Strategy, Comprehensive Ecosystem of People, Vehicles, and Homes", "Accordi

-

![]()

ByteDance Enters Physical AI, Igniting the Second Wave of 'Feast'?

-

![]()

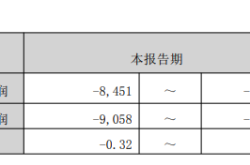

Phoenix Optics Forecasts a Nearly 70% Drop in First-Half Net Profit, Yet Optical Business Profit Shows Growth!

-

![]()

A Staggering 50.16% Reduction in Losses Projected! COST's Interim Report Signals a Pivotal Moment

-

![]()

Nearly 19% of National Total! Guangdong Boasts 164 Registered Large Models as New AI Personification Regulations Take Effect

-

![]()

BYD’s Baosha, Sought After by Australians, Makes a Triumphant Return to China

-

【Focus】Analysis of Downstream Demand Sectors and Key Enterprise Development for Acrylic OCA Optical Adhesives in China by 2026