Hangzhou’s ‘Six Little Dragons’ Yield IPO Contender: Monetizing SaaS, Spinning AI Narratives

04/16 2026

04/16 2026

501

501

In the competitive race for IPOs among Hangzhou’s ‘Six Little Dragons,’ Qunhe Technology is emerging as a frontrunner in the Hong Kong market.

From its failed 2021 U.S. IPO attempt—which once peaked at a $2 billion valuation—to its strategic pivot to Hong Kong in 2025, Qunhe’s journey to listing has spanned four years.

During this period, the company reached a pivotal turning point. Financial disclosures from its February 2024 prospectus revealed years of losses, but fresh data indicated an adjusted net profit of RMB 57.1 million for 2025.

However, discussions around Qunhe extend beyond mere profitability: Is it a SaaS enterprise or a spatial intelligence innovator banking on embodied AI training and spatial AI models?

Qunhe’s co-founder and chairman, Huang Xiaohuang, shared on WeChat Moments: ‘People joke whether selling NVIDIA stock to start the business was wiser than Qunhe’s returns. From GPU computing to embodied AI training, Nvidia and Jensen Huang’s influence has been invaluable. But money isn’t the point.’

Yet, money remains crucial—IPOs are about pricing the future. After 14 years, a team of tech visionaries has built an RMB 800 million revenue business with a 23% market share. Now, they need a compelling spatial intelligence narrative to justify higher valuations.

I. Selling NVIDIA Stock to Launch a Business

Qunhe’s inception followed a classic ‘technology seeks application’ entrepreneurial trajectory.

In 2007, Huang Xiaohuang, Chen Hang, and Zhu Hao met while studying abroad in the U.S., all pursuing computer graphics at the University of Illinois Urbana-Champaign.

After graduating, Huang worked as a software engineer at NVIDIA on CUDA platform development. In 2011, he sold his NVIDIA shares to return to China, initially aiming to ‘simulate physics with computers’ by transforming GPU computing power into real-world applications.

Technical ideals soon collided with reality. The team explored multiple directions—applying rendering technology to film visual effects, exhibition design, and human-computer interfaces—but failed due to unclear commercialization paths or weak demand.

Their 2012 ‘Home Renovation Treasure,’ a tool for designers, flopped due to poor PC compatibility and mobile experience. A subsequent focus on online cabinet design tools also failed due to a narrow user base.

The turning point came in 2013.

The team identified a clear pain point in home renovation: designers took hours or days to render images, while homeowners wanted instant feedback.

Qunhe’s GPU cluster technology could compress rendering times to seconds. In 2013, they launched Kujiale, offering ‘10-second renderings and 5-minute renovation plans’—a revolutionary improvement when industry averages stood at hours per image.

This choice reflected sound commercial logic. The home design industry had paying customers willing to pay for efficiency—decoration firms, furniture brands, and independent designers—where faster rendering meant quicker client conversions and higher deal rates.

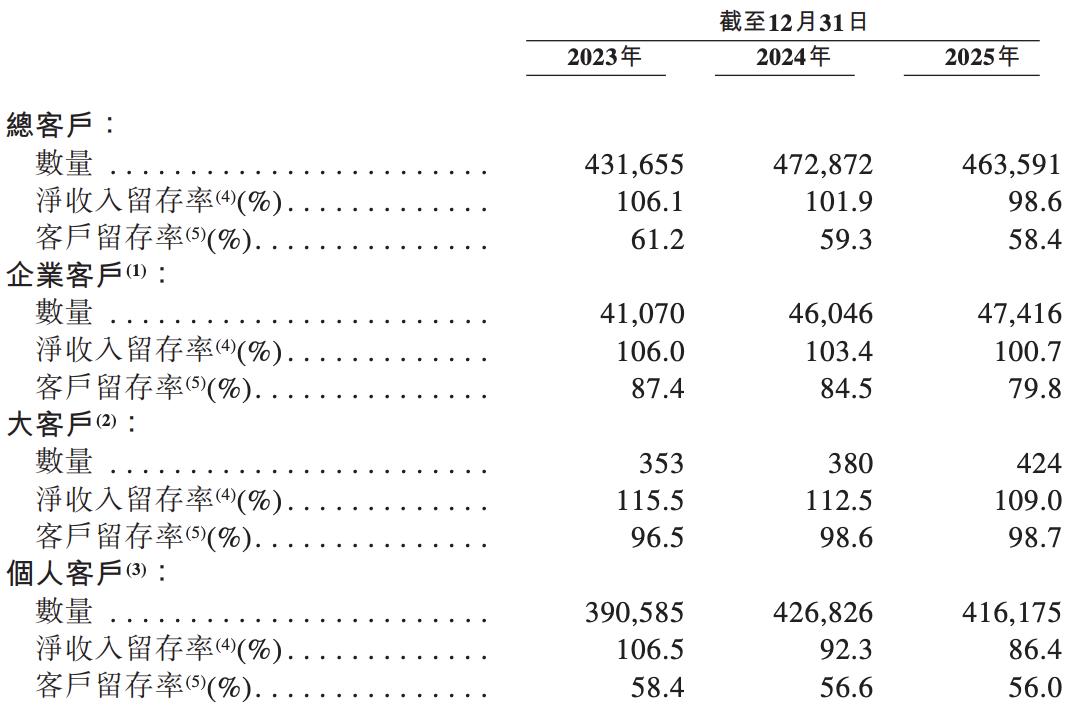

According to the prospectus, Kujiale’s paying enterprise clients grew from under 1,000 in 2014 to 47,416 in 2025, validating sustained demand.

In December 2013, IDG Capital led a $2 million Series A funding round; in 2014, GGV Capital led a $10 million Series B. Later, Shunwei Capital, Hillhouse, Coatue, and others joined across 11 rounds totaling approximately $295 million.

Investors bet on ‘cloud-native + GPU computing’ disrupting traditional on-premise design software. Moving design work to the cloud promised transformative efficiency gains in distribution, collaboration, and iteration.

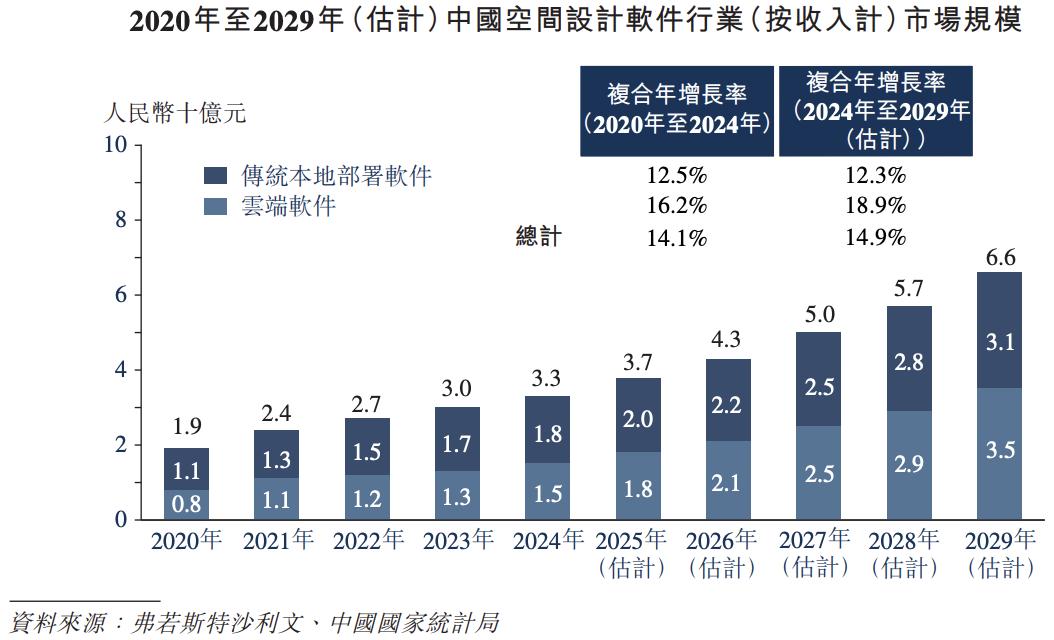

However, this track limited growth. Qunhe leads China’s spatial design software market with a 23.2% share, but the overall market was just RMB 3.3 billion in 2024, projected to reach only RMB 6.6 billion by 2029.

This ceiling explains Qunhe’s IPO repositioning from ‘cloud design software’ to ‘global spatial intelligence leader.’

II. Behind the Turnaround

The capital markets’ most-watched narrative in Qunhe’s prospectus is its ‘adjusted net profit turnaround.’

In 2025, the company reported RMB 57.1 million in adjusted net profit, versus adjusted losses of RMB 242 million in 2023 and RMB 70.1 million in 2024.

This marks Qunhe’s transition from SaaS’s cash-burn phase to profitability, driven by revenue growth and expense reductions.

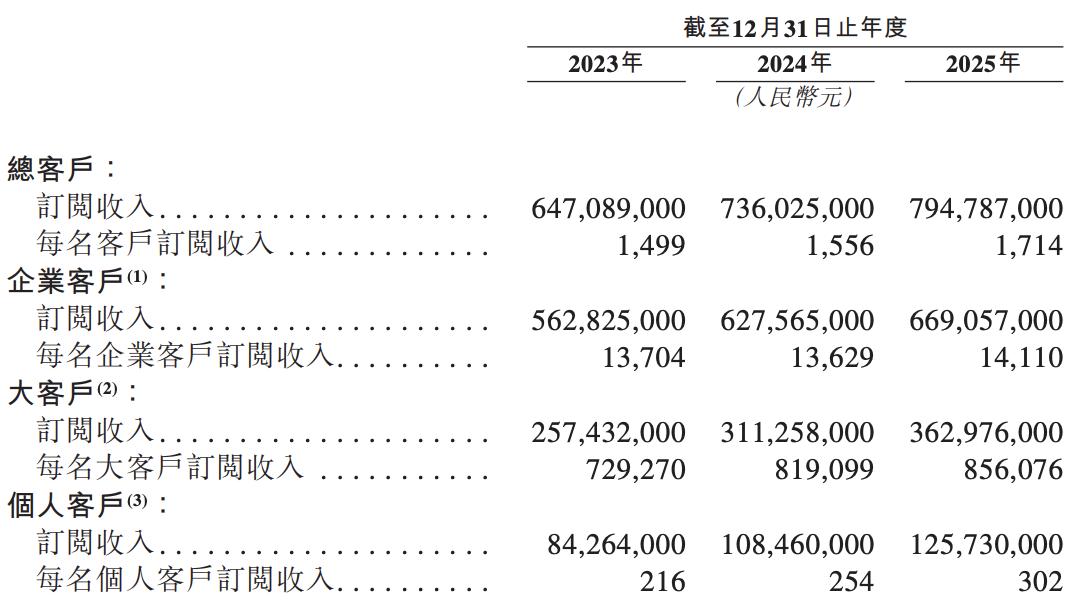

Revenue climbed steadily from RMB 664 million in 2023 to RMB 820 million in 2025, while gross margins rose from 76.8% to 82.2%, indicating strong pricing power and scale effects for core products.

Simultaneously, R&D and sales expense ratios plunged.

R&D expenses fell from 58.9% of revenue in 2023 to 35.5% in 2025; sales expenses dropped from 53.7% to 33.4%. The sales team shrank from 615 to 484.

Specifically, 2025 R&D spending was RMB 291 million, down approximately RMB 100 million from 2023; sales expenses were RMB 274 million, down approximately RMB 82 million. Combined, these cuts saved approximately RMB 182 million.

More critically, Qunhe’s customer quality metrics are declining.

From 2023–2025, overall net revenue retention fell from 106.1% to 98.6%; overall customer retention dropped from 61.2% to 58.4%. Enterprise retention slid from 87.4% to 79.8%, while individual retention fell from 58.4% to 56.0%. Only large clients (spending >RMB 200,000 annually) maintained 96.5–98.7% retention.

This divergence stems from Qunhe’s recent strategy to lower pricing thresholds for SMEs. However, SMEs’ limited budgets, short lifespans, and price sensitivity naturally lead to higher churn.

While large clients (retaining >98%) contribute half of enterprise revenue, their growth ceiling looms amid China’s property downturn—a cyclical industry where leading firms have limited budget expansion room.

Currently, large clients’ ARPU (average revenue per user) rose from RMB 729,000 to RMB 856,000. If large client growth stalls and SME churn persists, Qunhe’s profitability faces severe risks.

Considering revenue growth, cost structure, and customer retention, Qunhe has proven profitability but through efficiency optimization.

Future sustainability hinges on two factors: (1) whether large clients’ ARPU can keep rising, and (2) whether SME churn can be curbed through product improvements or pricing strategies.

Qunhe is a SaaS company with a validated model but unproven high-growth potential.

III. The ‘Spatial Intelligence First’ Gambit?

This isn’t Qunhe’s first IPO attempt.

In its 2021 U.S. listing bid, it pitched as the ‘first 3D cloud design stock’—essentially a design SaaS firm centered on Kujiale. But tighter Chinese concept stock regulations and SaaS valuation corrections derailed the IPO.

Now, its Hong Kong positioning shifts to ‘global spatial intelligence leader.’

This reflects changing capital market valuation logic.

Pure SaaS firms face valuation compression in secondary markets. In contrast, AI and embodied intelligence narratives offer higher valuation elasticity and imagination.

The new narrative centers on SpatialVerse, a 2024-launched business labeled a ‘spatial intelligence solution.’

Simply put, it transforms Kujiale’s 14-year accumulation of 360+ million 3D models and billions of indoor scenes into datasets for AI model training, simulating real-world physics and spatial relationships.

Why does this matter? Since 2024, embodied intelligence and robot training have become global tech’s hottest tracks. For robots to perform complex tasks like serving tea or cleaning in homes, they need not just algorithms but high-quality training data.

Unlike text or image data, spatial and physical interaction data are costlier and slower to acquire. SpatialVerse provides virtual training environments where robots can perform thousands of grasping, navigation, and obstacle-avoidance trials before real-world deployment.

Qunhe’s SaaS subscription business faces a ~RMB 10 billion revenue ceiling—China’s spatial design software market will reach just RMB 6.6 billion by 2029.

Positioning as spatial intelligence changes the valuation logic. SaaS tools are judged on revenue growth and margins; spatial intelligence is valued on data barriers and future applications.

However, this story remains unproven. Prospectus data shows SpatialVerse acquired approximately 8 clients in 2024 (RMB 3.4 million revenue) and 16 in 2025 (RMB 5.2 million), accounting for <1% of total revenue.

More pressing is competition. In spatial intelligence, Qunhe isn’t alone. Baidu’s ERNIE models and SenseTime’s SenseCore are developing 3D spatial understanding with stronger computing resources and algorithm teams.

Qunhe’s edge lies in vertical-scene data accumulation, particularly granular indoor home data. But whether this can translate into cross-scenario, scalable technical barriers remains untested.

The shift from ‘cloud design software’ to ‘spatial intelligence first’ is essentially a valuation re-anchoring. It tells markets: ‘Don’t measure me as a SaaS company—I don’t sell software subscriptions but tickets to digitize the physical world.’

For investors, Qunhe is a stable but slow-growing SaaS base with a sexy but uncertain spatial intelligence long-term option.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action