OpenClaw has not only led to token sell-outs but also fueled the cloud computing boom!

04/17 2026

04/17 2026

578

578

OpenClaw (Clawbot) has gained significant popularity on GitHub, with this open-source AI agent framework sweeping through the developer community like wildfire.

This framework enables AI large models to evolve from traditional conversational generation to autonomous planning, tool invocation, and task execution, effectively becoming 'digital labor.' With simple configurations, enterprises can automate complex tasks such as code writing, data analysis, and system operations.

This signifies a restructuring of cloud computing business models: shifting from selling computing power and storage to selling intelligence and agents.

For all cloud computing companies, the choice is clear: ride the wave of AI agents or be left behind by the times.

Post-2025, it's not that traditional cloud services will become obsolete, but rather that the rules of the game have fundamentally changed—from resource-driven to intelligence-driven, and from infrastructure leasing to AI capability empowerment.

For cloud providers still clinging to IaaS and PaaS without innovation, the difficulty has increased exponentially.

In China, Alibaba Cloud dominates the cloud computing industry, with even Tencent and Huawei struggling to compete. The remaining small and medium-sized cloud providers are barely surviving below the break-even line.

Take UCloud, for instance, which has never been profitable since its listing but has finally encountered a once-in-a-lifetime opportunity.

01

UCloud: Significant Loss Reduction

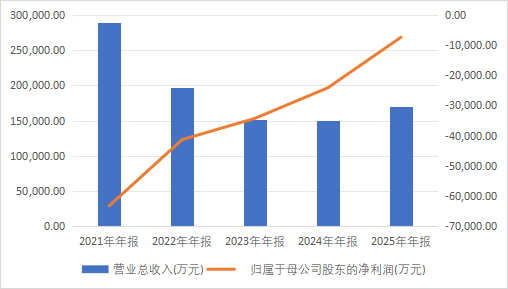

On April 10, 2026, UCloud released its 2025 annual report. Revenue reached RMB 1.699 billion, up 13.07% year-on-year; net loss attributable to shareholders was RMB 74 million, a significant reduction of 67.8% year-on-year; and net operating cash flow was RMB 243 million, up 98.64% year-on-year.

Data Source: iFind

Against the backdrop of AI large models sweeping across industries, this leading domestic neutral third-party cloud computing service provider is proving with solid performance that independent cloud providers can not only survive amidst competition from industry giants but also find new growth curves in the AI era.

This is a battle for survival and the future. Can UCloud transform amidst the wave of AI intelligent computing?

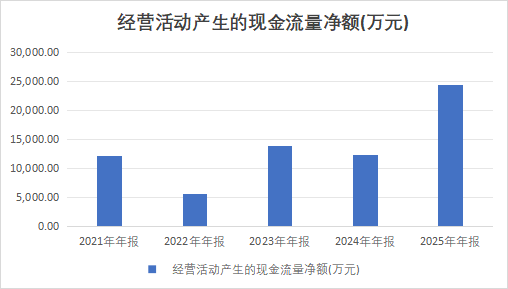

UCloud's net operating cash flow reached RMB 243 million in 2025, up 98.64% year-on-year, nearly doubling. This marks the second consecutive year of positive operating cash flow, setting a new historical high.

Data Source: iFind

Cash flow is the lifeblood of a business. For an asset-heavy, long-cycle industry like cloud computing, operating cash flow better reflects a company's true ability to generate cash than net profit. UCloud's ability to nearly double its operating cash flow while growing revenue indicates a significant improvement in business quality.

Another key signal is the substantial reduction in net losses.

From a loss of RMB 241 million in 2024 to a loss of RMB 74 million in 2025, UCloud narrowed its losses by 67.8% in just one year. If this trend continues, the company could potentially break even or even turn a profit in 2026.

How is the quality of revenue growth?

With revenue of RMB 1.699 billion, up 13.07% year-on-year, how does this growth rate compare in the cloud computing industry? Compared to industry giants, Alibaba Cloud grew by about 10% in 2025, while Tencent Cloud grew by about 8%. UCloud's 13% growth actually outpaces most cloud providers.

This demonstrates that, as an independent third-party cloud provider, UCloud is finding its niche through differentiated competition.

02

Structural Recovery Driven by AI Intelligent Computing

In 2025, UCloud's revenue grew by 13.07%, from RMB 1.503 billion to RMB 1.699 billion, an increase of nearly RMB 200 million.

Where did the money come from?

The rapid growth of the AI intelligent computing business was the primary driver.

UCloud disclosed in its annual report that the company seized opportunities in AI development and focused on two main themes: 'AI Development and Global Expansion.' In 2025, revenue from AI intelligent computing-related businesses surged, becoming the core engine driving revenue growth.

Specifically, UCloud launched several major products in the AI field:

The 'Kongming' Intelligent Computing Platform is the company's core product for AI large model training and inference. It provides a full-stack technical solution from underlying computing power acquisition, training and inference capabilities, to AI application development, and has been deployed in multiple scenarios such as biopharmaceuticals, finance, and intelligent customer service.

The Large Model Training and Inference All-in-One Machine is an innovative product launched in 2025. This software-hardware integrated product allows government, financial, and healthcare clients to deploy exclusive large models within their enterprises with a single click, enabling out-of-the-box AI application experiences. The annual report disclosed that this product has been widely adopted by clients across multiple industries.

The AstraFlow AI Product Suite is the company's core platform for AI algorithm and application developers, providing full-link support from model loading to service output, effectively lowering the barrier to entry for AGI application development.

UPFS Parallel File Storage is a high-performance storage product designed for large model training scenarios, meeting the storage needs of massive training data.

Meanwhile, the traditional cloud computing business also saw steady recovery.

In the public cloud business, UCloud's GPU cloud hosts and GPU bare metal cloud hosts, among other computing products, deeply align with the massive data processing, model training, and inference needs in AIGC scenarios. The client base now widely covers innovative enterprises such as large model companies, AI application companies, and robotics companies engaged in AI technology research and development.

In the hybrid and private cloud businesses, the company continues to expand its client base in traditional industries such as finance, government, and healthcare, providing hybrid cloud solutions that combine 'public cloud + private deployment + dedicated network.'

Another easily overlooked factor is the recovery of the industry cycle.

In 2025, with the rapid popularize of large model applications, the cloud computing market showed signs of overall recovery. According to data from the China Academy of Information and Communications Technology, China's cloud computing market reached RMB 828.8 billion in 2024, up 34.4% year-on-year, and is expected to surpass RMB 3 trillion by 2030.

As an independent third-party cloud provider, UCloud has gained opportunities for differentiated competition in the AI era with its positioning of being 'neutral, secure, and trustworthy.'

03

AI Tailwind: The Intelligent Revolution in the Cloud Computing Industry

UCloud's revenue recovery and loss reduction are inseparable from the tailwind of AI large models.

AI intelligent computing is not simply 'AI + cloud computing' but an upgrade from resource delivery to intelligent delivery in cloud computing. Against the backdrop of the popularize of AI large models, enterprise clients' needs are fundamentally changing—from renting servers and storage space to procuring AI training and inference capabilities and agent services.

How deep is AI's impact on the cloud computing industry?

Since late 2025, open-source agent frameworks like OpenClaw (Clawbot) have rapidly gained popularity, with AI technology gradually evolving toward 'digital labor' capable of independent planning, tool invocation, and long-term memory.

The rapid development of AI agents has driven new demand for computing power—inference computing power demand is rising at an even faster pace and is expected to become the largest and most sustained demand segment in cloud computing.

How large is the cloud computing market?

According to the 'Cloud Computing Blue Book' released by the China Academy of Information and Communications Technology in July 2025, the global cloud computing market reached USD 692.9 billion in 2024, up 20.2% year-on-year, and is expected to approach USD 2 trillion by 2030.

China's cloud computing market reached RMB 828.8 billion in 2024, up 34.4% year-on-year, and is expected to surpass RMB 3 trillion by 2030.

Among them, demand in the AI-related intelligent computing cloud sector is booming, driving up demand for other cloud resources such as storage. The cloud computing market saw price increases in early 2026, with major domestic providers including UCloud, Alibaba Cloud, Tencent Cloud, and Baidu Intelligent Cloud, as well as overseas giants like Amazon AWS, Google Cloud, and Microsoft Azure, all announcing price hikes.

What is UCloud's competitive advantage in AI intelligent computing?

Neutrality.

Compared to giants like Alibaba Cloud and Tencent Cloud, UCloud, as an independent third-party cloud provider, does not compete with clients in their core businesses. This 'neutrality' is even more valuable in the AI era, as large model companies and AI application companies prefer to deploy their core businesses on neutral platforms like UCloud rather than on competitors' clouds.

Full-stack service capabilities serve as a moat.

UCloud provides services through public, private, and hybrid cloud models, covering business needs across different scenarios in industries ranging from internet, media, and finance to manufacturing.

Differentiated positioning is the breakthrough.

In the AI era, UCloud focuses on two main themes: 'AI Development and Global Expansion,' avoiding direct competition with giants in the general IaaS field and establishing differentiated advantages in the AI intelligent computing niche.

However, the AI intelligent computing business also faces fierce competition.

Huawei Cloud, Alibaba Cloud, and Tencent Cloud are all ramping up their AI computing power investments. As an independent cloud provider, UCloud still lags behind in terms of financial strength and brand influence. Whether it can hold its ground amidst competition from the giants is the company's biggest challenge.

04

Survival Strategies Amidst Price Wars from Industry Giants

Although UCloud has achieved revenue growth and significant loss reduction, it still faces substantial competitive pressure.

Alibaba Cloud was the earliest to layout in the AI large model field, with its Tongyi Qianwen large model already widely applied across multiple industries. More importantly, Alibaba Cloud possesses the most complete AI infrastructure stack, forming a closed loop from chips and servers to cloud platforms and large models.

Alibaba Cloud has rapidly seized market share through price cuts, lowering cloud product prices multiple times since 2024, putting immense pressure on small and medium-sized cloud providers.

Tencent Cloud leverages super apps like WeChat and QQ to enjoy natural advantages in internet, gaming, and social sectors. In the AI era, Tencent Cloud has deeply integrated AI capabilities with social and gaming scenarios, forming unique competitiveness.

Huawei Cloud boasts a strong sales network and brand influence in the government and enterprise market, with its 'cloud-network-security' integrated solutions highly favored by government and state-owned enterprise clients. In the AI computing power field, Huawei's Ascend chips + Huawei Cloud's software-hardware integrated solutions are highly competitive.

Operator clouds like China Telecom Cloud, China Mobile Cloud, and China Unicom Cloud, backed by state-owned capital and government and enterprise client resources, hold significant market share in government and state-owned enterprise clouds.

What is UCloud's response strategy?

Focus on differentiated segments.

UCloud avoids direct competition with giants in the general IaaS field and focuses on differentiated segments such as AI intelligent computing, hybrid cloud, and private cloud. The company explicitly stated in its annual report that it will 'deepen the integration, application, and innovation of AI technologies in the cloud computing field.'

05

Risks: Three Major Challenges During the Transition Period

Risk of persistent losses.

Despite significant loss reduction in 2025, UCloud has yet to achieve profitability. If it fails to turn a profit in 2026, the company's capital reserves and financing capabilities will face tests. As of the end of 2025, the company's cumulative undistributed losses still stood at RMB 2.064 billion.

Alibaba Cloud, Tencent Cloud, Huawei Cloud, and other giants are making astonishing investments in the AI intelligent computing field. As an independent cloud provider, UCloud still lags behind in terms of financial strength and brand influence. Whether it can defend its market share amidst competition from the giants remains uncertain.

Risks in AI commercialization.

Although the AI intelligent computing business has promising prospects, large-scale commercialization still faces challenges. Factors such as clients' value perception, willingness to pay, and deployment complexity for AI intelligent computing products may all affect the pace of business expansion.

-END-

Disclaimer: This article is based on the public company attributes of listed companies and relies primarily on information disclosed by the companies in accordance with their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms) as the core basis for analysis and research. Shiyu Xingkong strives to ensure the fairness of the content and views presented in the article but does not guarantee their accuracy, completeness, or timeliness. The information or opinions expressed in this article do not constitute any investment advice, and Shiyu Xingkong assumes no responsibility for any actions taken based on this article. Copyright Notice: The content of this article is original to Shiyu Xingkong and may not be reproduced without authorization.

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action