Seizing the Trillion-Dollar Blue Ocean: A Comprehensive Breakthrough for China's Domestic Computing Power Chain!

04/17 2026

04/17 2026

631

631

If there were a vote for the most 'contradictory' field in 2026, AI for Science (AI4S) would likely win by a landslide.

On one hand, a trillion-dollar industrial blue ocean beckons: According to QYResearch, the global AI4S market is expected to reach USD 26.23 billion by 2032, with a compound annual growth rate (CAGR) of 28.9%. The combined market size across six major industries approaches USD 11 trillion, with current penetration rates still in single digits—leaving vast room for growth. Policies are ramping up nationwide, from the 15th Five-Year Plan's explicit call to 'lead scientific research paradigm shifts with AI' to dedicated AI4S policies in Beijing, Shanghai, and Shenzhen.

On the other hand, research institutions face a stark reality—a severe shortage of computing power. Demand is skyrocketing, yet large-scale clusters capable of meeting AI4S requirements remain scarce. More paradoxically, 'surplus' and 'shortage' coexist: National smart computing centers operate at just 32% utilization, leaving vast resources idle. Built computing power sits unused while high-quality resources remain inaccessible to critical research scenarios—a structural mismatch that defines AI4S's current dilemma.

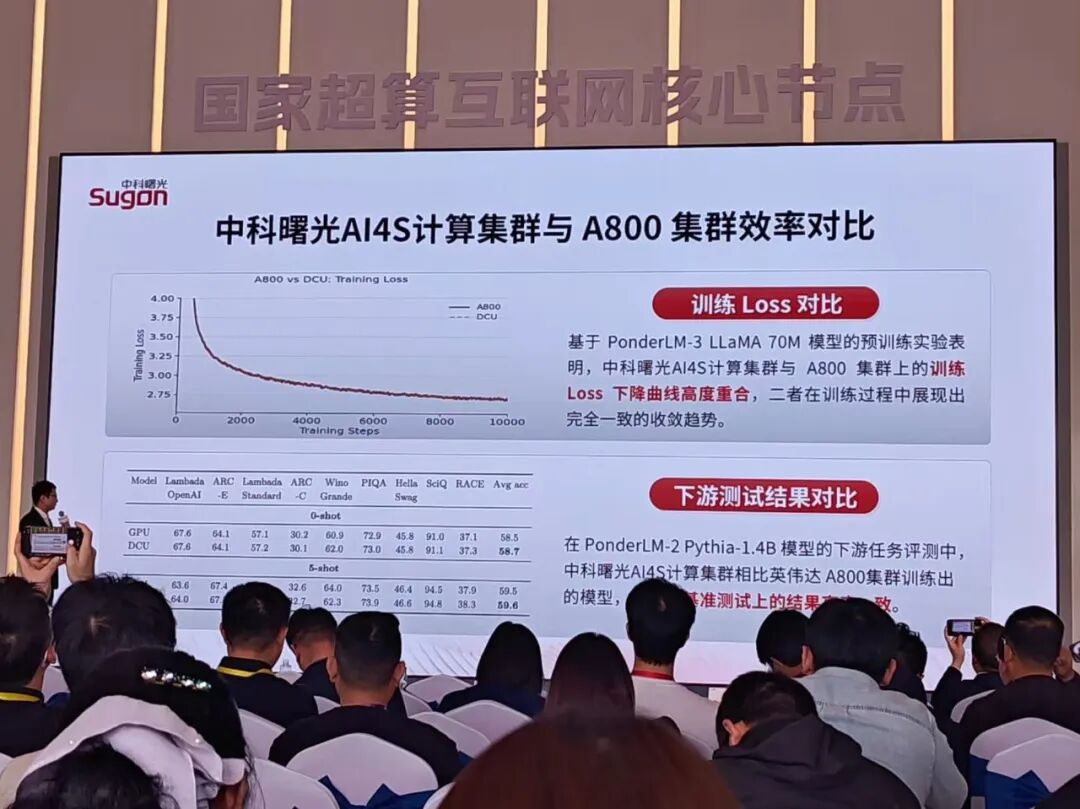

AI4S demands distinct computing capabilities compared to general-purpose large model training. While the latter focuses on content generation, AI4S tackles complex scientific problems at atomic and molecular levels—requiring high-precision floating-point operations, ultra-low-latency high-speed interconnects, and extreme stability for long-duration tasks. AI4S needs not generic computing power but deeply optimized specialized infrastructure.

This explains why the 60,000-card AI4S computing cluster was instantly hailed as a 'computing power powerhouse' upon its release. Judging by its recent pace, the company appears to be answering with speed: Launching the scaleX 10,000-card supercluster in December 2025, deploying 30,000 cards at the National Supercomputing Internet's core node in February 2026, and expanding to 60,000 cards by April—each step spaced just two to three months apart.

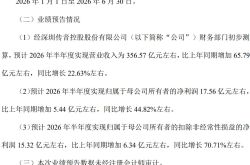

Financial results reinforce this momentum: 2025 revenue hit RMB 14.964 billion (+13.81% YoY), with non-GAAP net profit surging 33.97% YoY. Q1 2026 revenue reached RMB 3.072 billion (+18.80% YoY), while non-GAAP net profit soared 57.77% YoY. Gross margins are poised to rise from ~24% to over 40%.

Beyond the headlines, its deeper impact on the computing ecosystem warrants attention.

First, AI4S is forging a value chain from computing investment to industrial output. Previously, six key industries faced lengthy R&D cycles and high validation barriers, leading to 'hesitation in using computing power.' Now, they 'leverage computing to accelerate cycles.' The 60,000-card cluster's OneScience platform integrates 'data-computing-modeling-application,' enabling researchers to develop scientific large models within hours and compress task cycles from days to hours.

Second, China's domestic computing ecosystem is evolving from 'usable' to 'user-friendly,' driving full-stack industrial maturity. The 60,000-card cluster employs domestic chips and a self-developed 400G lossless high-speed network, with features like efficient coupled deployment and three-tier storage-computing-transmission coordination. This provides a large-scale testing ground for domestic AI chips, high-speed switches, distributed storage, and liquid cooling solutions. Improved developer tools and model compatibility are attracting research institutions and commercial firms to migrate to domestic platforms.

Third, the structural contradiction of 'computing surplus' is being resolved through high-quality supply. Data shows 42 national 10,000-card smart computing clusters operate at ~30% utilization, due to mismatches between general-purpose computing and specialized needs. The 60,000-card cluster, optimized for AI4S from networking to storage and scheduling, is key to activating idle resources. Its achievement of simulating 4.5 trillion atoms/molecules (a world record) proves that when computing power 'targets the right problems,' downstream demand far exceeds expectations. This 'application-driven computing' model could shift smart computing centers from blind expansion (blind expansion) to precision construction, refining industrial chain (industrial chain) links like computing scheduling, cross-domain collaboration, and operational optimization.

As research shifts from 'decade-long endeavors' to 'computing-driven innovation,' the competition for AI4S computing infrastructure has just begun. The future hinges on: Who can iterate sustainably? Who can truly convert computing power into industrial value? Who can pioneer the path from 'computing powerhouses' to 'robust ecosystems'? The computing chain surrounding this evolution is poised for a holistic upgrade—spanning hardware to software, single points to systems.

-

![]()

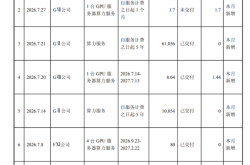

Computing Power Supplier Bags Orders Worth Over 600 Million Yuan, Yet Receives Only 4.5 Million Yuan in Actual Payments!

-

Alibaba Is Just Five Months Away from Securing Two Consecutive AI Coding Titles

-

![]()

Less Investment Isn't Apple's Get-Out-of-Jail-Free Card

-

![]()

The 'King of Africa' Tecno Mobile: What Is the Market Hesitating About After Its 'V-shaped' Rebound?

-

![]()

ByteDance Restructures Feishu, What Signals Does It Send?

-

![]()

ByteDance Overhauls Feishu: What Strategic Signals Are Being Sent?

-

![]()

Pay $39 a Month with Apple Upgrade: Apple's New Business, Your Old Wallet

-

![]()

The Open-Source Debate Dividing Silicon Valley