No One Can Escape the Token Bill

07/06 2026

07/06 2026

524

524

Produced by | RoboIsland

In the second week of June, a Tencent employee logged into the internal management dashboard as usual, ready to use AI for work, only to find their monthly Token quota—previously $2,000—reduced to RMB 1,400. Within two days, the quota was exhausted.

According to incomplete statistics, after the adjustment, Tencent employees across different departments now have monthly Token quotas ranging from RMB 1,000 to RMB 7,000. In teams heavily reliant on AI, such as the Hunyuan large model team, employees receive around RMB 7,000 per month, while outsourced staff at Tencent Entertainment are allocated just RMB 1,000.

In the third week of June, Doubao officially launched its professional paid subscription service, offering three tiers: RMB 68, RMB 200, and RMB 500 for consecutive monthly subscriptions.

The announcement quickly sparked controversy across social media. Netizens revisited a poll from two months earlier, in which 88,000 out of 91,000 participants opposed charging fees, questioning Doubao's confidence. Many worried: Would the free version become "dumbed down"? Could they still ask questions freely?

Doubao officials repeatedly emphasized that basic features would remain permanently free, but few users believed them. History has shown that once a paid model is established, the "free cake" only gets smaller.

On the last day of June, SiliFlow submitted its IPO prospectus to the Hong Kong Stock Exchange.

Founded just 35 months ago, the company doesn't develop large models or applications. Instead, it focuses on unifying chips from NVIDIA, Huawei Ascend, Biren, and others through a proprietary engine, enabling models like DeepSeek and Qwen to run efficiently. It then sells access based on Token usage to developers and enterprises.

The prospectus revealed RMB 55.33 million in revenue for 2025, a 653% YoY increase. However, net losses reached RMB 345 million, over six times its revenue. Gross margin plummeted from 39.4% in 2024 to -24%, meaning the company lost RMB 0.24 for every RMB 1 earned.

The public cloud MaaS business fared even worse, with a gross margin of -119%, losing RMB 1.19 for every RMB 1 earned.

Some saw their quotas slashed, others started paying, and some raised funds through IPOs. From workers' desks to users' phones to IPO filings at the Hong Kong Stock Exchange, Tokens are reshaping three distinct scenes simultaneously.

Token, a term once confined to engineers' technical documents just two years ago, is now barging into everyone's bills unexpectedly.

In just half a year, the era of free Token usage has ended, ushering in a new age of full cost settlement.

I. The Token Factory: Selling More, Losing More

The explosive growth in Token usage has spawned a new breed of business: the Token factory.

These factories package complex engineering capabilities—chip adaptation, model deployment, inference engine optimization, and heterogeneous computing power scheduling—into standardized API interfaces. Developers can then access these resources on-demand and pay based on usage, much like utilities.

NVIDIA CEO Jensen Huang defines this as the "AI factory" concept, where higher Token throughput per watt at fixed power levels reduces production costs. SiliFlow is China's most prominent player in this space.

Founder Yuan Jinhui's journey reads like a startup novel. A Tsinghua PhD and student of Academician Zhang Bo, he founded OneFlow in 2016 to develop deep learning training frameworks. In 2023, OneFlow was acquired by Wang Huiwen's Light Year Beyond, which later merged into Meituan after Wang's medical leave.

Yuan declined Meituan's retention offer and relaunched his team in August 2023. By Spring Festival 2025, DeepSeek went viral globally, and SiliFlow quickly launched a full-powered DeepSeek model powered by Huawei Cloud Ascend computing, catapulting it to fame overnight.

But the financials tell a less glamorous story.

Partnered models. Source: SiliFlow official website

SiliFlow operates two business lines: one profitable, one not.

The first is public cloud MaaS, which rents GPUs, packages model APIs, and charges per Token. This generated RMB 29.26 million in 2025 revenue (52.9% of total), with paying clients surging from 2,454 to 716,000—a 289x increase.

Yet its gross margin was -119%. Why?

Computing power is a fixed cost. Whether clients use it or not, rental fees must be paid. In 2025, SiliFlow spent nearly RMB 60 million on computing rentals, accounting for 87% of sales costs.

To fill capacity, it distributed over RMB 54 million in vouchers to free users, all counted as sales expenses without generating revenue. Add RMB 209 million in R&D (378% of revenue), and losses mount.

The second line is on-premises solutions, where clients provide their own computing power, and SiliFlow deploys engines for software licensing fees. This generated RMB 26.07 million in 2025 revenue with an 82.5% gross margin. However, it's project-based with long delivery cycles and limited scalability.

While fluctuating numbers are tolerable, SiliFlow's strategic position is precarious.

Upstream, Alibaba and Huawei Halo are both shareholders and suppliers, directly competing in the public cloud MaaS market. Part of SiliFlow's rental costs flows to these competitors.

Downstream, without proprietary models, it relies on open-source alternatives, lacking pricing power. When DeepSeek officially cuts prices, SiliFlow must follow. Without a cloud ecosystem for cross-subsidies, every yuan burned is pure cost.

Thus, at this stage, the larger the Token factory's scale, the greater its potential losses. Selling Tokens isn't a guaranteed profit. When computing power is fixed but revenue variable, every order is a gamble on whether clients will fully utilize their quotas.

II. The Token Resellers: Profiting in the Gray Zone

If Token factories are the regular forces (legitimate forces), then Token relays operate as guerrilla units in the gray area.

Their business logic is simple: users send requests to relays, which route them through their own channels to large models, then return results. Think of it as an underground power grid for AI, where official circuits are expensive and restricted, prompting some to illegally tap, distribute, and sell electricity.

The profit margins are staggering. RoboIsland interviewed veteran investors who revealed that leading relay projects can generate RMB 5 million in monthly revenue with gross margins near 50%.

The most common tactic is wholesale-retail: bulk-purchasing developers' Coding Plan packages, combining quotas, and reselling them. Others encapsulate web or client interfaces into APIs, while more extreme methods include mass-registering startup accounts to claim free quotas from platforms like OpenAI for zero-cost resale. Some even split membership accounts among 20 users to share costs.

If these tactics merely skirt the law, model substitution borders on fraud. Users pay premium prices for top-tier models like Claude but receive responses from low-end alternatives.

Illegal AI relays face constant account bans, and user data—conversations and uploads—may be intercepted and sold for profit.

These layered gray operations yield profits far exceeding traditional financial gray markets. However, this business model is inherently short-lived, filling a market gap where "demand outpaces regulations." It's a transient product of the AI boom.

Once upstream vendors crack down on violations, profit margins built on reverse-engineering and stolen credentials will shrink.

III. The Collective Pivot Amid Cost Cliffs

Token demand isn't just outpacing regulations—it's surpassing cost controls. Despite majority opposition in trial polls, Doubao proceeded with formal charging, driven primarily by computing costs.

By June 2026, Doubao's large model averaged over 180 trillion daily Token calls. At an estimated RMB 4 per million Tokens, daily costs reached RMB 720 million. Even conservative estimates put daily costs between RMB 130–240 million.

ByteDance's profits are being devoured by AI investments. In 2025, its capex reached RMB 150 billion, mostly for AI. In 2026, this rose to RMB 200 billion. With profits eroding and spending escalating, commercialization became inevitable.

Paid users, however, are unimpressed. Some report bugs in Doubao's "Office Task Mode" and unpredictable quota consumption, likening it to a "blind box" where task completion costs remain unknown.

Doubao product introduction. Source: Doubao official website

ByteDance isn't alone in facing computing crunches. Global tech giants are tightening employee Token quotas:

Uber exhausted its 2026 AI budget by April, capping monthly employee usage at $1,500. Meta imposed spending limits or mandated cheaper model usage. Amazon discontinued its internal AI leaderboard, KiroRank, urging employees to "avoid using AI for its own sake."

In June, Tencent adjusted Token quotas, replacing flat allocations with dynamic task-based distributions and eliminating rankings.

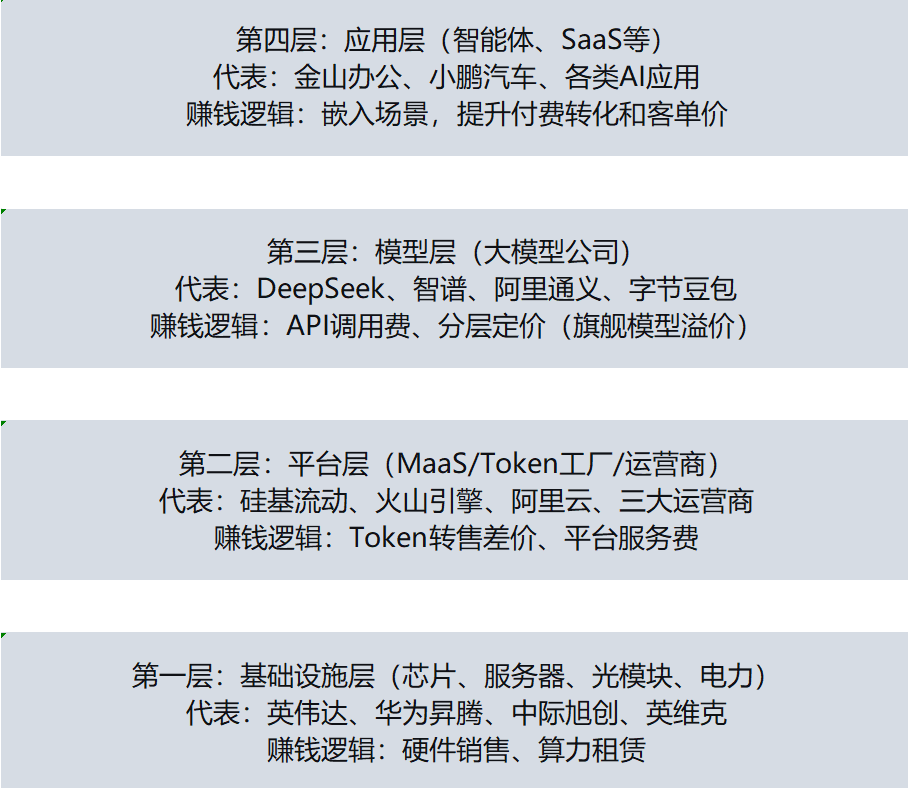

IV. Who's Really Profiting from Tokens?

The Token economy now features a clear industrial hierarchy with distinct profit logics at each level. Some profit from scarcity, others from ecosystems, while some burn money for future gains.

Four-tier Token industry chain. Created by RoboIsland

At the top, chip manufacturers profit from selling "shovels." Their logic is simple: harder technical barriers and scarcer production capacity yield higher profits.

NVIDIA claims every Token is a profit unit, but the real money lies in the "machines" producing Tokens. MoXi Technologies' 30x revenue growth in three years stems from its unique manufacturing capabilities.

The midstream is more complex, divided into three layers:

1. Cloud Providers: Locking in Ecosystems

Their profit logic revolves around migration costs—losing money at the entry point but profiting downstream. General-purpose models may operate at a loss, but once enterprises bind their Agents to a cloud ecosystem, platforms shift from charging for "computing power" to "production flow tolls." Moving data, workflows, and Agents off the platform becomes nearly impossible.

Volcano Engine and Alibaba Cloud use low-cost models to capture market share, monetizing through cloud storage, databases, and security services. In 2025, Volcano Engine held nearly half the public cloud MaaS market but generated just RMB 1.5 billion in revenue. Its 2026 target of RMB 15 billion reveals the market's current burn-for-scale phase.

2. Model Developers: Profiting from Capability Tiers

These firms earn by stratifying capabilities. Lightweight models chase volume and general traffic, while flagship models defend prices in high-value scenes like coding and long-context processing. This path demands extreme technical barriers—only model developers with irreplaceable capabilities in coding, Agents, and other scenes can sustain premium pricing.

3. Operators: Exploring "Traffic-to-Token" Conversion

In 2025, China's three major telecom operators saw a 2.3% YoY decline in net profits, ending 12 years of growth. With traditional communications saturated, Tokens represent a new growth bet. In May 2025, China Telecom launched a RMB 9.9/10 million Token package, with China Mobile following suit. On June 29, China Mobile established a Token office.

Yet operators face clear dilemmas. Liu Liehong, director of the National Data Administration, warned that Tokens, as a new pricing unit, cannot rely on the The era of traffic (traffic-era) playbook of Grab the market at low prices (low-price market capture) and Subsidy for scale (subsidies for scale). Operators sell extensions of their "pipelines," packaging AI computing power into data plans. But pipelines themselves generate no value—without proprietary model capabilities, they lack pricing power.

At the bottom, application scenarios profit from barriers.

AI office tools, coding platforms, and legal contract reviewers with strong scene barriers and user stickiness have reaped real rewards. For example, Kingsoft Office boasts an 85.95% gross margin, but this stems from its document scene, not models. AI applications without scene barriers see every yuan of revenue siphoned off by chip makers, cloud providers, and model developers first.

Across the chain, profits haven't evenly distributed with Token usage growth. Only a few application-layer players with scene barriers truly profit. Independent third-party MaaS platforms like SiliFlow are squeezed in the middle—lacking chip scarcity, cloud ecosystem locks, or proprietary model pricing power, they can only burn money for scale, betting on a temporary window.

V. Conclusion

A Tencent employee complained on Maimai: "I use my salary to buy Tokens, boosting efficiency for the company. Model developers profit, but I'm paying to work, and my workload hasn't decreased."

This dilemma is widespread. Amid grand Token narratives—whether NVIDIA redefining data centers as Token factories or Lenovo launching Token factory solutions—the average worker cares more about whether to revert to manual coding or pay out of pocket for quotas.

AI has become a paid resource. Everyone caught in this revolution must recalculate their costs. Someone, somewhere, will always foot the bill for the Tokens burned.

Cover source: *The Litchi of Chang'an*

Featured image source: AI-generated

Copyright of Robo Island. All rights reserved. Reproduction without authorization is prohibited.

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models

-

Former Employer Sponsors IPO, Ex-Employee Leads Finance: Yunbao Intelligent's IPO Embroiled in a 'Web of Connections'

-

![]()

Volkswagen's Market Share in China Drops to 9.7% in a Decade, U.S. Brands Down to 5%: Chinese Automakers Take the Offensive to Competitors' Doorsteps

-

![]()

In the AI-Driven Office Era, Is WPS Becoming a Hidden Threat to Hard Drives?

-

![]()

When AI Begins to Reshape Infrastructure: A Reshuffle in the U.S. Cloud Market