AI Enters Second Half: Buy the 'Cloud,' Not the 'Chip'?

07/14 2026

07/14 2026

475

475

Source | Bohu Finance (bohuFN)

In early July, a piece of news sent ripples across global capital markets.

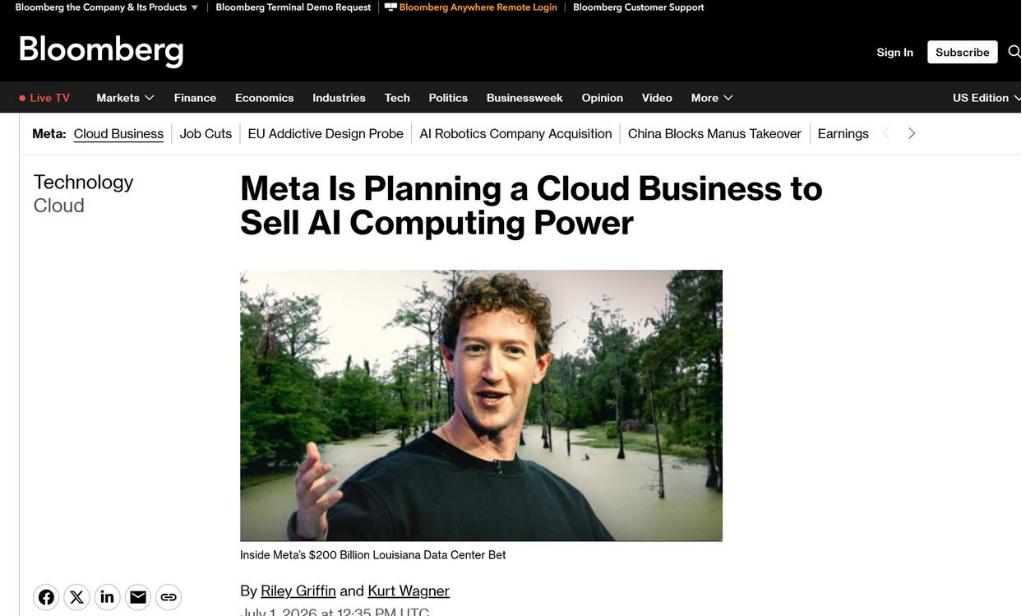

According to Bloomberg, Meta is planning to launch a new cloud infrastructure business, selling its surplus AI computing power to external customers. The news sent Meta's stock price soaring by 8.8% in a single day, with its market value increasing by approximately $127 billion in one day.

At the same time, the computing power supply chain, seen as a beneficiary of AI infrastructure, came under collective pressure—CoreWeave and Nebius AI cloud vendors plummeted by 13.92% and 17.01%, respectively; storage chip stocks like SanDisk and Micron Technology fell by over 10%.

One news story sent the market value of leading computing power companies on a rollercoaster ride.

Meta renting out its unused GPUs to make money seems like a simple business. However, the market is concerned: if even one of the world's largest GPU buyers starts selling computing power, does the assumption that computing power will always be scarce still hold?

Once the narrative of computing power scarcity cracks, it will not only affect the performance and stock prices of AI cloud vendors but also shake the logic that has driven the entire AI supply chain forward over the past two years.

Is the AI industry about to burst its bubble?

The answer may not be so simple. The real watershed will emerge when the AI industry stops competing solely on computing power scale and model parameters—it's not about who has more GPUs but who can make each GPU create more value.

01 Is the AI Infrastructure at a Turning Point?

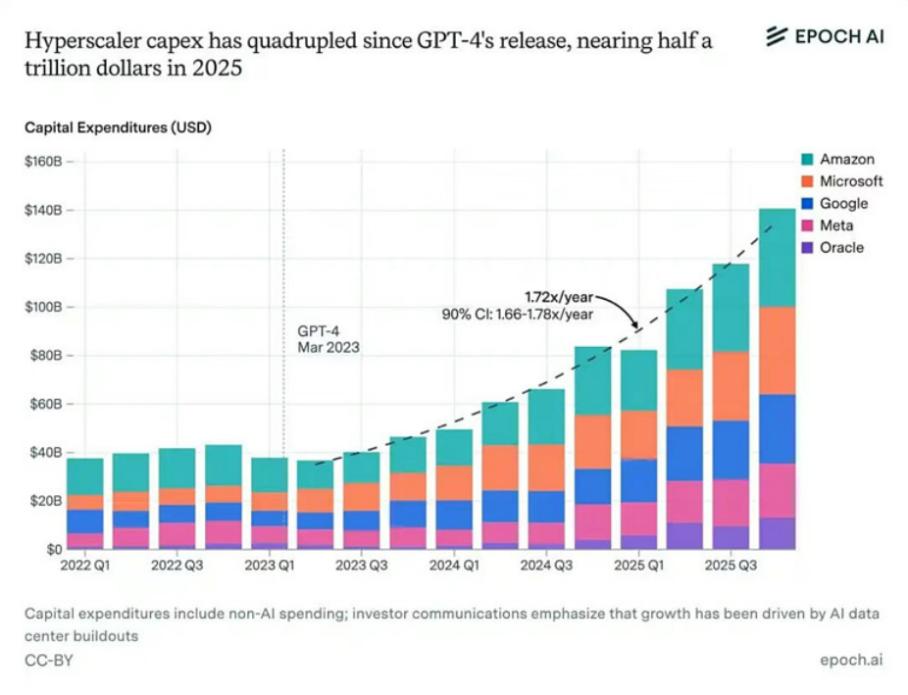

Over the past two years, global tech giants have embarked on an unprecedented capital expenditure race, all sharing the same belief: AI computing power will always be scarce.

To understand this logic, one must grasp the story the AI supply chain is telling.

Whether it's generative dialogue, coding, agents, or other AI applications, they all ultimately consume computing power. The difference lies in whether they consume training computing power ( phased , phased ), inference computing power ( sustainability , sustainability ), or both.

However, computing power demand does not experience diminishing marginal returns as scale expands; instead, each invocation requires a fresh consumption of computing power. This is why major companies are actively investing in capital expenditures—the more GPUs they stockpile, the higher their computing power barrier becomes.

Behind each GPU lies a complete supply chain comprising HBM, PCBs, optical modules, electricity, and data center clusters. As long as there is demand for AI applications, GPU shipments will be supported, and the supply chain's prosperity will continue.

Therefore, the market also assumes that as long as AI demand sustained growth (continues to grow), computing power will remain scarce. Over the past two years, NVIDIA's market value briefly topped the global rankings; SK Hynix and Samsung boosted the South Korean stock market, all driven by the same logic.

But the problem is, this logic is being shaken by Meta's plan.

First, Meta's move to 'sell computing power' exposes the anxiety tech giants face amid soaring capital expenditures.

As one of the world's largest GPU buyers, Meta's AI-related capital expenditures for 2026 are as high as $125-145 billion, with total leasing commitments reaching $182.9 billion.

In addition, in 2025 alone, the capital expenditures of five major overseas companies—Amazon, Microsoft, Google, and others—are approaching $500 billion, with no sign of peaking yet.

Yet Meta wants to rent out the computing power it purchased at great expense, indicating that even tech giants are beginning to feel burdened by sustained capital investments.

Second, tech giants are reevaluating whether to continue their unlimited investments in AI competition.

Meta's move to rent out computing power hints at a possibility: if the revenue expectations from AI applications consistently lag behind the Expansion rate (expansion speed) of capital expenditures, only a few companies may ultimately continue participating in this 'money-burning race.'

Clearly, Meta is planning to leave itself an escape route—besides becoming another 'OpenAI,' it could also become another 'AWS'—leasing out potentially surplus computing power after the computing power arms race.

This story is not unfamiliar. Amazon's early days with AWS involved renting out excess servers purchased annually to handle 'Black Friday' demand during off-peak times, only for AWS to become Amazon's most profitable division.

Meta's step forward is a sound out (probe).

But if this were the only action, it wouldn't be enough to make the market worry that computing power will shift from scarcity to surplus. What truly matters is the deeper signal it releases: the AI supply chain may form new divisions of labor.

Meta not only has computing power but also infrastructure such as training frameworks, model services, and developer tools, all of which can be offered for sale. Tech giants are not just computing power buyers; they can also be infrastructure integrators or even rule setters.

If this logic holds, AI computing power competition will shift from hardware competition to a contest combining software and hardware capabilities—giving you the 'shovel' and teaching you how to dig faster and better. This is the reconstruction happening in the AI cloud market.

02 Is 'Selling Computing Power' a Good Business?

Driven by AI, Token demand has surged, and the cloud services market has experienced a boom.

According to Synergy Research Group, global enterprise spending on cloud infrastructure services reached $129 billion in the first quarter of 2026, up 35% year-over-year, marking the highest growth rate since the fourth quarter of 2021.

The Chinese market is also accelerating. Data from the China Academy of Information and Communications Technology shows that the domestic AI computing power rental market reached 68 billion yuan in the first quarter of this year, up 62% year-over-year, with full-year projections expected to exceed 260 billion yuan.

However, while the pie is growing, the fates of players differ. Currently, cloud vendors' business models mainly fall into three categories:

The first is computing power infrastructure providers, with CoreWeave in the U.S. being the most typical example. Its business model is straightforward: the company buys GPUs, builds data centers, and rents them out to AI companies by the hour, earning money from resource integration.

However, this business model, while seemingly riding the wave, is not as profitable as imagined.

In the first quarter of this year, CoreWeave reported revenue of $2.078 billion, up 112% year-over-year, but struggled with profitability, with its adjusted net loss widening to $589 million in the first quarter.

The business model of computing power intermediaries is far more fragile than imagined, with rentals, depreciation, and expansions all eating into profits. This is why CoreWeave was the first to plummet following Meta's announcement of renting out computing power.

The second category is computing power as a platform, represented by AWS and Alibaba Cloud. They not only sell computing power but also model services, development toolchains, databases, and more, with computing power being just one piece of the puzzle.

Clearly, selling in bundles is more profitable. Alibaba's fiscal year 2026 second-quarter earnings preview shows that Alibaba Cloud's revenue growth accelerated to around 45%, with its EBITA margin improving from around 9.1% in previous quarters to the low double digits, indicating that its AI monetization is entering a return phase.

The third category is computing power creating applications, such as consumer-facing products like Doubao and Qianwen. While they don't explicitly sell computing power, every user query consumes computing power.

According to Volcano Engine, as of June this year, Doubao's large model had surpassed 180 trillion daily Token invocations, growing more than tenfold over the past year.

However, according to LatePost, Doubao's current daily revenue is less than 1 million yuan, relying almost entirely on e-commerce commissions embedded in Douyin Mall. The computing power consumed by consumer users has yet to contribute corresponding revenue and profits.

It's clear that this round of AI-driven cloud service expansion differs significantly from previous cycles.

The era of cloud services competing on resources and price is over. Today, cloud vendors compete on full-stack integration of computing power, models, toolchains, and application ecosystems. Who eats the meat and who drinks the soup depends on where you stand in the supply chain.

03 'Competing on Cards' Is Inferior to Competing on Capabilities

The business of 'selling computing power' has entered a new narrative, with capital market winds blowing toward domestic giants.

Over the past year, the AI industry has focused on 'computing power scale,' with major companies being pressured to continuously increase capital expenditures, yet returns remain elusive.

Therefore, market funds have preferred to bet on the computing power hardware supply chain, as the hardware-side business model is clear, orders are visible, and financial results are straightforward.

But now, the market has changed. It no longer just looks at who invests more aggressively or whose models run faster but asks how all these GPUs will be monetized and who can turn AI into profits first—how to use AI to drive business growth or even create entirely new revenue streams will become the anchor for enterprise valuations in the next phase.

In this competition, Alibaba Cloud has taken the lead.

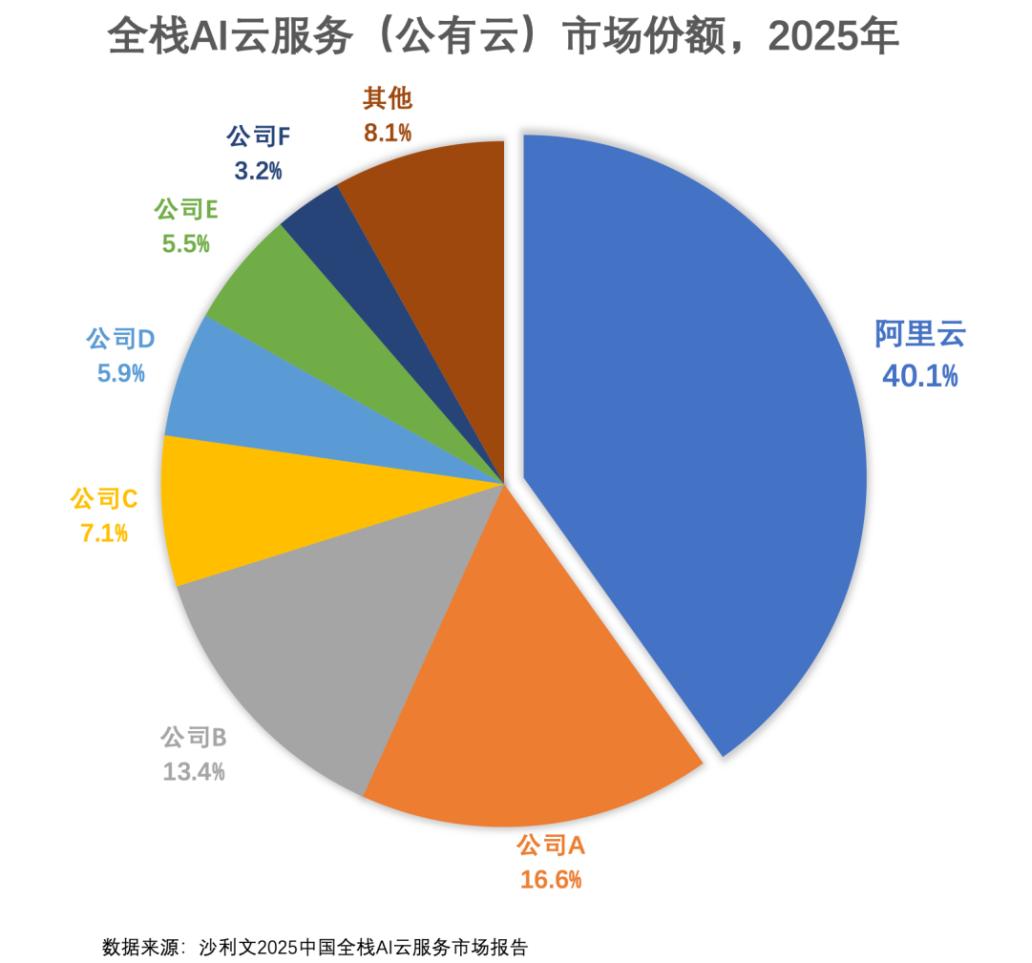

According to a report by Frost & Sullivan, the total market size of China's IaaS, PaaS, and MaaS reached 59.59 billion yuan in 2025, with Alibaba Cloud ranking first with 23.9 billion yuan in revenue and a 40.1% market share, exceeding the combined total of the second to fourth place vendors.

Alibaba Cloud's confidence comes from its full-stack self-research in 'chips-cloud-models-inference.' At the chip layer, over 60% of Alibaba's T-Head computing power serves external commercial customers; at the model layer, Qianwen has achieved near-leading closed-source model performance on multiple authoritative benchmarks; at the platform layer, the BaiLian MaaS platform has seen an 8x increase in customer numbers year-over-year.

Alibaba revealed that in the first quarter of fiscal year 2026, AI-related product revenue accounted for over 30% of Alibaba Cloud's external commercial revenue for the first time, with expectations to exceed 50% in the coming year, becoming the primary driver of Alibaba Cloud's revenue growth.

Volcano Engine, meanwhile, is the new king of the MaaS track (MaaS track).

IDC data shows that in 2025, Volcano Engine held a 49.5% market share in China's public cloud MaaS services, ranking first. According to 36Kr, Volcano Engine has raised its 2026 MaaS business revenue target to 15 billion yuan, up from around 1.5 billion yuan in 2025.

Volcano Engine's core logic is to define the cloud through models, converting computing power into Token intelligence via MaaS, then assembling Tokens into Agents, supplemented by complete development and operations tools to enable Agents to serve clients in core enterprise domains.

Volcano Engine CTO Wu Di believes that while traditional IaaS, PaaS, and SaaS layering represents a consensus on technical stratification, what matters more in cloud computing's future is focusing on products and businesses themselves rather than how the layers are divided.

Baidu Cloud shares a similar viewpoint with Volcano Engine, believing that the cloud services market will embrace new rules.

Baidu Chairman Robin Li has proposed a new judgment: Tokens may not represent the final outcome, with DAA (Daily Active Agents) being the new metric for the AI era. Computing power consumption is merely a cost, while the value created by Agents is the output.

In the first quarter of 2026, Baidu's AI cloud revenue reached 8.8 billion yuan, up 79% year-over-year; AI business revenue hit 13.6 billion yuan, accounting for 52% of Baidu's general business revenue. Driven by AI, Baidu's revenue structure is undergoing a fundamental transformation.

Tencent Cloud, meanwhile, has taken a distinct path, combining 'AI + SaaS.'

Tencent Cloud's logic is to embed AI capabilities into specific business scenarios, such as incorporating AI value-added functions into SaaS products like Agent development platforms and low-code development platforms, focusing not just on Token transactions but also on innovating AI application scenarios.

In 2025, Tencent Cloud achieved Large scale profitability (scaled profitability) for the first time; in the first quarter of this year, all three of Tencent's business segments saw significant AI-driven growth, with marketing services revenue up 20% year-over-year thanks to AI-driven ad recommendation models.

Alibaba bets on full-stack integration, Volcano Engine on models, Baidu on Agents, and Tencent on scenarios. While the tech paths of these giants differ, they all point to the same direction: the competition in cloud services ultimately hinges on who can turn AI into real cash flow.

Now, the question Meta probed has an answer.

Tech giants are entering the cloud services market with different trump cards, but the only chip that matters is getting customers to use their services and making their businesses truly viable.

In the second half of the AI industry, computing power is the ticket, but services are the real business.

The cover image and illustrations in this article are owned by their respective copyright holders. If the copyright holders believe their works are unsuitable for public browsing or should not be used free of charge, please contact us promptly, and our platform will make corrections immediately.

-

![]()

Why Does Yin Qi, Who 'Doesn't Listen to Advice,' Insist on Making AI Agent Smartphones? | Interview with Jieyue Xingchen

-

![]()

AI-Generated Code Reveals Surprise That Thrills China

-

More Than Selling GPUs: NVIDIA Launches Computing Power Loan, Creating a New Model of Revenue-Sharing Computing Power Cooperation

-

The answer lies in the performance of the production line by the end of 2026

-

![]()

The Voice in AI Hardware Industry is Quietly Shifting Amid Brain Drain

-

![]()

AI Enters Second Half: Buy the 'Cloud,' Not the 'Chip'?

-

![]()

Breaking the Monopoly! Trillion-Parameter Large Model Adopts Domestic Chips, Marking a Key Step Towards 'De-NVIDIA-ization' in AI Computing Power

-

![]()

Performance Drops Sharply, Seres Alerts 280,000 Shareholders