Performance Drops Sharply, Seres Alerts 280,000 Shareholders

07/14 2026

07/14 2026

506

506

Seres Finds Itself 'Back to Square One' Almost Overnight.

As of July 13, four listed automotive companies have unveiled their 2026 interim performance forecasts, all indicating losses.

Corporate announcements reveal that GAC Group (601238.SH) is expected to suffer losses ranging from 4.06 billion to 4.57 billion yuan in the first half of the year, compared to a net loss of 2.538 billion yuan in the same period last year, with losses widening further. JAC Motors (600418.SH) anticipates losses of approximately 740 million yuan in the first half, slightly narrower than the 773 million yuan loss recorded in the same period last year. BAIC BluePark (600733.SH) forecasts losses between 1.77 billion and 1.97 billion yuan, a reduction of roughly 340 million to 540 million yuan compared to the same period last year, marking its sixth and a half consecutive years of losses.

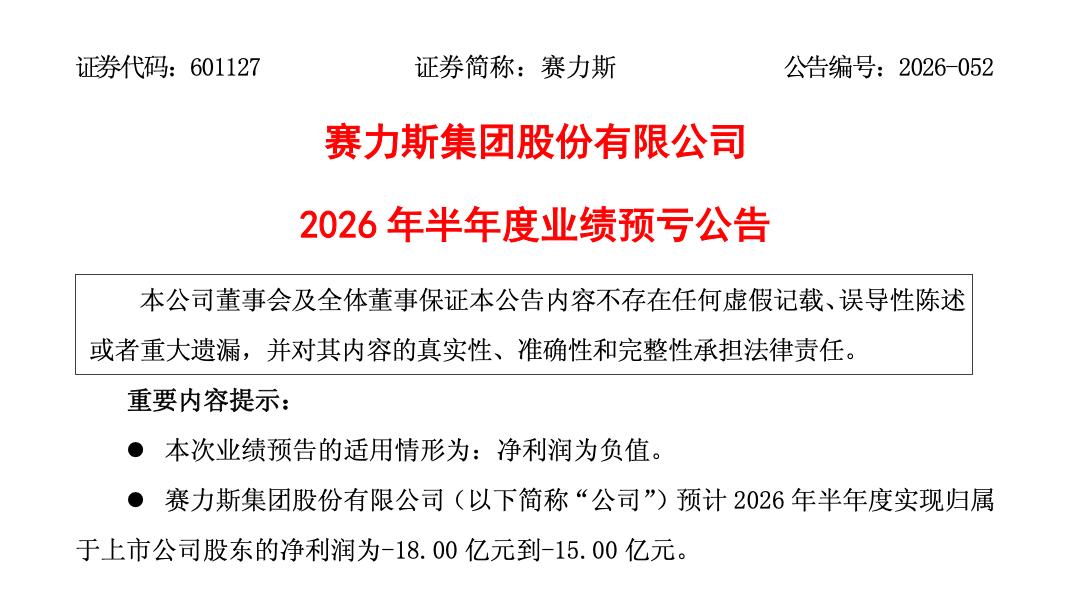

In contrast to these three companies experiencing sustained losses, the unexpected 'performance reversal' of Seres (601127.SH) is particularly notable: Seres is projected to incur losses ranging from 1.5 billion to 1.8 billion yuan in the first half of the year, a stark contrast to the profit of 2.941 billion yuan in the same period last year.

Image Source: Screenshot from Seres Announcement

The shift from profit to loss has transformed Seres from a 'high achiever' to a 'struggling student,' drawing widespread attention and even trending on social media, diverting some public scrutiny away from GAC, BAIC, and JAC. On July 13, the A-share automotive sector experienced a collective downturn, with Seres' stock price hitting the daily limit and closing at 53.91 yuan per share, giving the company a market capitalization of 93.91 billion yuan. On July 14, Seres' stock price continued to decline, having dropped nearly 70% from its peak of over 170 yuan per share in September last year, resulting in a loss of 200 billion yuan in market value.

The most unusual aspect of this performance forecast is that Seres' losses are not due to a collapse in sales; in the first half of 2026, Seres' cumulative sales of new energy vehicles reached 178,800 units, up 3.87% year-on-year. The stark contrast between growing sales and plummeting profits is striking.

More noteworthy than the performance forecast itself is the question it raises for the entire new energy vehicle industry: In the current competitive landscape, can automakers reliably convert sales into profits, even with popular models, premium brands, and consistently growing sales volumes?

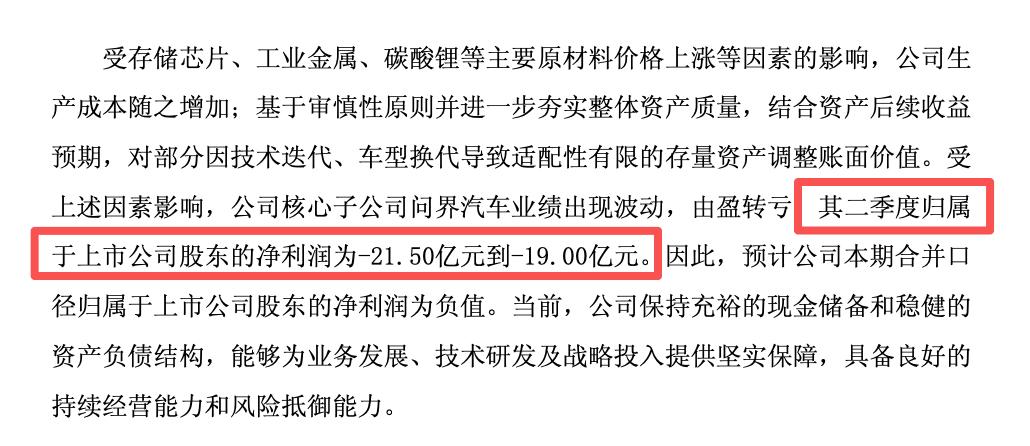

According to the data disclosed in the announcement, Seres' losses almost entirely occurred in the second quarter.

In the first quarter of this year, the company's net profit attributable to shareholders of the listed company was 754 million yuan. However, in the second quarter, AITO is expected to incur losses ranging from 1.9 billion to 2.15 billion yuan for the quarter, not only wiping out the first-quarter profits but also dragging the entire first half into the red.

Image Source: Screenshot from Seres Announcement

The 'performance bombshell' has sparked dissatisfaction and skepticism among many investors. Regarding this performance fluctuation, Seres primarily attributes it to rising raw material prices and adjustments to the book value of certain existing assets. Specifically, firstly, the increase in prices of major raw materials such as memory chips, industrial metals, and lithium carbonate has significantly raised vehicle manufacturing costs. Secondly, based on prudence, the company has adjusted the book value of certain existing assets whose adaptability has declined due to technological iterations and model updates, further depressing current profits.

These explanations are certainly valid, but when viewed in the context of the entire industry, rising raw material prices are not a challenge unique to Seres.

Since the beginning of this year, nearly all new energy vehicle manufacturers have been under pressure from rising supply chain costs, ranging from battery materials to automotive-grade chips and various metal materials. Meanwhile, the 'price war' continues, with automakers offering various incentives such as cash discounts, financial policies, trade-in subsidies, and free configuration upgrades to compete for market share.

In this market environment, automakers are generally facing the dual squeeze of 'rising upstream costs and downward pressure on downstream selling prices.' However, what truly differentiates companies is not the so-called cost pressure but their ability to better manage costs, allocate resources, and convert growth into actual profits.

Therefore, the more worthy discussion regarding Seres' shift from profit to loss is not the cost increase itself but why these pressures were so concentratedly reflected in the income statement in the second quarter of this year.

Image Source: CanTu Picture Library

Over the past few years, the success of AITO has propelled Seres onto the 'fast track.' To seize market opportunities, the company has continuously increased investments in R&D, new models, channel construction, and brand marketing.

This approach is not inherently flawed, but any rapid expansion presupposes that sales growth can continuously cover the escalating investments.

The issue arises when the industry enters a phase of stock competition (market saturation), and sales growth slows down. Can this growth logic still hold? The asset impairments mentioned in this financial report, to some extent, reflect this dilemma.

As models rapidly iterate, the production lines, molds, equipment, and inventory parts corresponding to older models quickly depreciate, meaning that past investments have not fully translated into future returns but have instead been reflected in current profits and losses. This is not only a normal phenomenon brought about by technological iterations but also places higher demands on companies' ability to switch between old and new products, manage inventory, and utilize assets efficiently.

In other words, while profit declines are undoubtedly influenced by external environmental factors, the deeper issue may lie in whether the company has established a profit management system commensurate with its current scale. Are R&D investments efficient enough? Is the product rhythm more reasonable? Are resource allocations truly centered around profitability? These issues often do not surface during periods of rapid growth but become apparent when growth slows down.

For Seres today, this interim report serves more as a stress test at the operational level. It does not imply that AITO has lost its competitiveness or that the company has fundamental operational issues. However, it does suggest that competition in the new energy vehicle sector is shifting from a race of who can expand faster to a race of who can manage better.

In the future, the real challenge for Seres' management will be to re-establish a balance between scale expansion, profit growth, and resource allocation, truly converting sales volumes into profits.

If this interim report exposes new challenges to Seres' profitability, then a more pressing question for the company is: Besides AITO, who can shoulder the growth tasks in the next phase?

Over the past few years, AITO has achieved remarkable milestones for Seres that were once unimaginable. From a traditional automaker long entrenched in the low- to mid-end market to entering the premium new energy vehicle market priced above 300,000 yuan, and then to continuously creating popular models like the AITO M9, Seres has achieved a comprehensive upgrade in brand recognition, sales volumes, and capital market approval with the help of Huawei.

However, any company that relies heavily on a single brand for an extended period faces increasing operational risks. The more successful AITO becomes, the greater its impact on Seres' performance—once profit fluctuations occur due to cost increases, product updates, or market competition, the entire group will be significantly affected.

According to previous disclosures, since collaborating on vehicle manufacturing in 2021, Seres has paid Huawei cumulative procurement fees exceeding 75 billion yuan, with 20 billion yuan in the first half of 2025 alone. Some analysts point out that Huawei charges approximately 10% in fees for AITO models, including 8% for marketing channel fees and 2% for technology licensing fees. This means that for an AITO model priced at an average of 400,000 yuan, 40,000 yuan is paid just for these two items.

Furthermore, as Huawei's 'Five Brands' matrix under Harmony Intelligent Mobility continues to expand, AITO's resource position within the Huawei ecosystem is also changing. Some investors question that while AITO accounts for nearly 70% of Harmony Intelligent Mobility's sales volume, its profits remain under pressure, and channel commissions continue to erode per-unit revenue, while marketing and store resources are being diverted to more 'brands'.

This interim report reflects the relatively concentrated growth structure. Against this backdrop, the launch of the new AI automotive brand AIVA by Saido Technology, in which Seres holds a stake, in June this year, is particularly noteworthy.

Image Source: Saido Technology

On June 9, when Saido Auto made its official debut, Zhang Zhengyuan, nephew of Seres Group founder Zhang Xinghai and chairman of Saido Technology, led the launch of the new brand AIVA.

Unlike AITO, which relies heavily on the Huawei ecosystem, AIVA adopts a different industrial collaboration model: Seres is responsible for vehicle R&D and manufacturing, ByteDance's Volcano Engine provides AI capabilities, Yuanrong Qixing handles assisted driving, and CATL supplies power batteries. It hopes to create a new growth curve in the mainstream market priced between 100,000 and 200,000 yuan by integrating industrial chain advantages.

To some extent, AIVA's mission goes beyond launching a new model or creating a new brand; it aims to answer a more crucial question: Can Seres still define products, integrate resources, and continuously create popular models after leaving AITO?

Of course, this challenge will not be easy. Compared to the competitive environment AITO faced when entering the premium new energy vehicle market, AIVA is entering the most fiercely competitive mass market, where established brands like BYD, Geely Galaxy, and Leapmotor coexist with a growing number of new players competing around intelligence and AI.

For consumers, brand recognition, product experience, pricing systems, and channel capabilities are more important than ever. Meanwhile, AIVA also carries Seres' expectations for optimizing its growth structure.

However, it should be noted that since Seres contributed existing assets and shifted from a controlling shareholder to a minority stakeholder, Saido Technology's operating performance and balance sheet will no longer be consolidated into Seres' listed company reports. At the same time, Seres Group can divest itself of 'Lixiang,' which has long been under operational pressure, and with external capital infusion, Seres does not have to bear the enormous investment costs alone for the future development of the new brand.

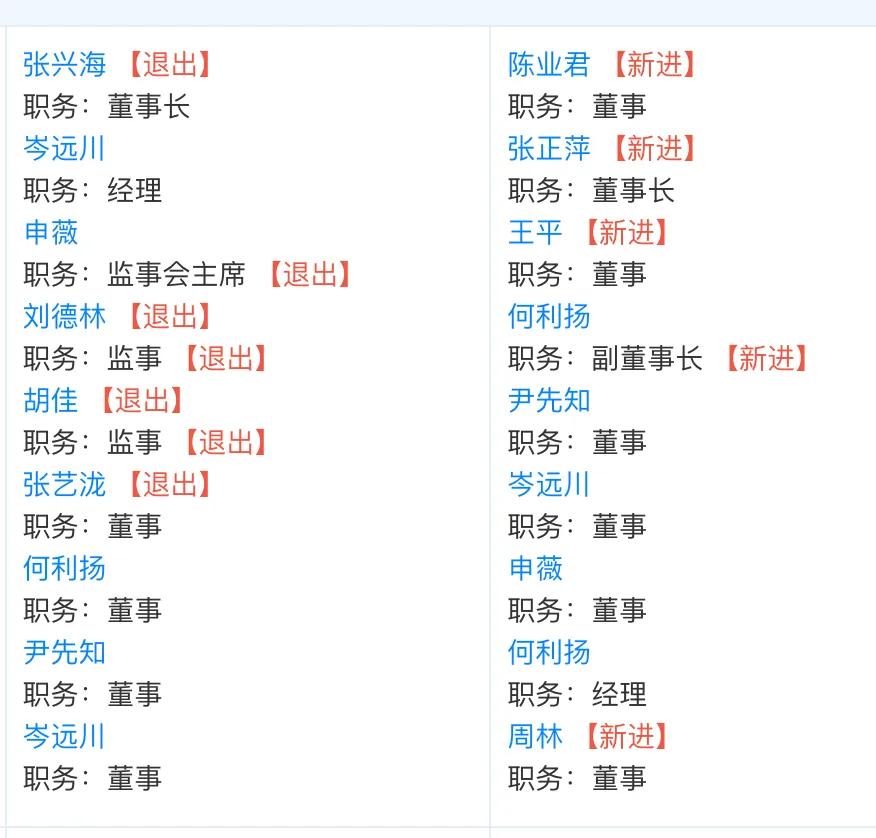

Image Source: Screenshot from Tianyancha

In the first half of this year, Seres completed a series of important personnel changes, further streamlining the management structure between the group and its business subsidiaries. Among them, Zhang Zhengping, son of Zhang Xinghai, succeeded as chairman of Seres Automobile Co., Ltd., meaning he has taken full charge of the group's core vehicle business, focusing on the refined operation, market expansion, and technological iteration of the new energy vehicle business centered around AITO.

For Seres and Zhang Zhengping's team, this interim report may serve more as a reminder. For a mature automaker, creating a popular brand is undoubtedly important, but what truly determines long-term competitiveness is always the ability to consistently generate profits.

-

![]()

AI-Generated Code Reveals Surprise That Thrills China

-

The answer lies in the performance of the production line by the end of 2026

-

![]()

The Voice in AI Hardware Industry is Quietly Shifting Amid Brain Drain

-

![]()

AI Enters Second Half: Buy the 'Cloud,' Not the 'Chip'?

-

![]()

Breaking the Monopoly! Trillion-Parameter Large Model Adopts Domestic Chips, Marking a Key Step Towards 'De-NVIDIA-ization' in AI Computing Power

-

![]()

Performance Drops Sharply, Seres Alerts 280,000 Shareholders

-

Behind the AI Boom: US Rakes in $314 Billion, South Korea $223 Billion, While China Lags at $26 Billion?

-

![]()

Volkswagen's 'Drastic Measures' to Cut Half of Its Models: Will China's Three Joint Ventures Be Affected?