Huawei, ByteDance, and Meta Compete on the Same Stage: AI Glasses Set to Remember 2026

02/27 2026

02/27 2026

639

639

Author | Chen Wen

Source | Insight New Research Society

As 2026 begins, the AI glasses sector kicks off the year's competition with a near-"saturation attack" approach.

In just over a month into the new year, manufacturers such as XGIMI, Thunderbird Innovation, Rokid, and Xuanjing have already launched a flurry of new products, while plans for the year from domestic and international giants like Meta, Google, Apple, Samsung, Huawei, and ByteDance have gradually come to light.

From "Year Zero" to "Total War," the 2026 smart glasses market is no longer just a plaything for geeks or a narrative for capital—it's a substantive clash over technology implementation, scenario positioning, and ecosystem construction.

01 All-Star Lineup Enters the Fray: From "Lightweight Experimentation" to "Standalone Terminal Breakthrough"

This year's AI glasses market has kicked off with a far more vibrant scene than ever before. It's no longer a solo act for startups but an "All-Star Game" featuring internet giants, major smartphone manufacturers, traditional eyewear channel operators, and AR newcomers.

The most noticeable trends this year are the significantly accelerated pace of new product launches and the clear divergence in technological paths, with CES 2026 in January serving as the ultimate stage for major players to showcase their strengths.

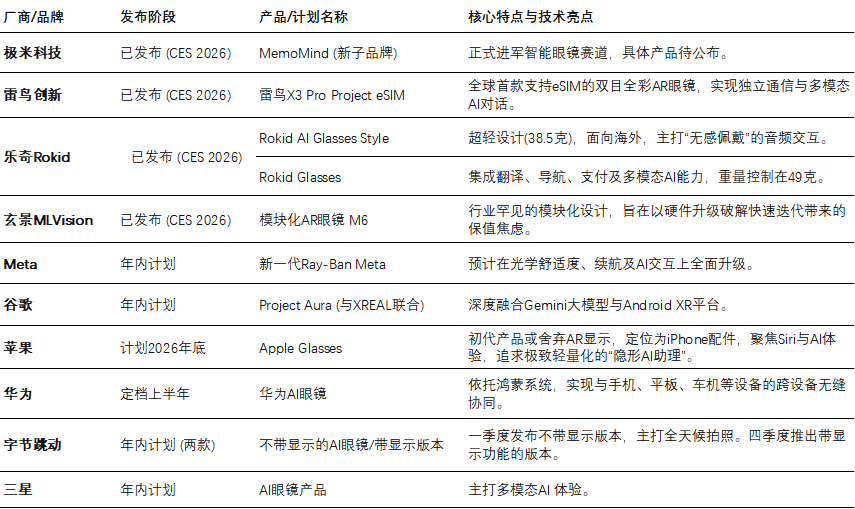

XGIMI Technology boldly introduced its new AI hardware sub-brand, "MemoMind," officially entering the smart glasses arena. Thunderbird Innovation unveiled the world's first binocular full-color AR glasses supporting eSIM standalone connectivity, the "Thunderbird X3 Pro Project eSIM," achieving true independent communication and multimodal AI dialogue without relying on smartphones—a key step in shedding the "accessory" label.

Rokid adopted a dual-track strategy: on one hand, it released the ultra-light 38.5-gram Rokid AI Glasses Style for overseas markets, focusing on "imperceptible wear" audio interaction; on the other, its core product, Rokid Glasses, integrates translation, navigation, payment, and multimodal AI large model capabilities, with weight controlled at 49 grams.

Additionally, Xuanjing MLVision introduced the industry's rare modular AR glasses, the M6, attempting to address consumer concerns about the rapid depreciation of electronics through a "hardware sustainable upgrade" model.

If the early-year product launches were the "appetizers," then the plans disclosed by the industry giants are the true "main course," pushing market competition to new depths.

Meta, the current "superpower" in the sector, captured 84% of the global AI glasses market share in 2025 with its Ray-Ban Meta (SAG data). Its 2026 moves are undoubtedly a bellwether for the industry. According to sources cited by Cailian Press, Meta plans to work with EssilorLuxottica to increase annual production capacity to over 20 million units, meeting explosive demand and seizing market opportunities. The next-generation Ray-Ban Meta is expected to see comprehensive upgrades in optical comfort, battery life, and AI interaction.

After a hiatus following Google Glass, Google is re-entering the fray with a "three-step" strategy: launching audio smart glasses with cameras and microphones in early 2026, focusing on voice translation and environmental understanding; releasing a monocular micro-display product by year-end; and partnering with XREAL to launch Project Aura, which deeply integrates the Gemini large model with the Android XR platform.

Apple is finally getting serious, with plans to release Apple Glasses by the end of 2026, according to Bloomberg. The initial product may forgo AR display capabilities, positioning itself as an iPhone accessory similar to the Apple Watch, focusing on Siri and AI smart experiences, and pursuing an "invisible AI assistant" experience through ultra-lightweight design for all-day wear.

Domestic manufacturers are also going all-in. Huawei's AI glasses are set for release in the first half of the year, leveraging the HarmonyOS system for seamless cross-device collaboration.

ByteDance has two products in the pipeline: an AI glasses model without a display launching in Q1, focusing on all-day photography, and a display-equipped version in Q4.

Samsung, Alibaba's Kuake, Baidu's Xiaodu, and Li Auto have also announced plans to deeply integrate AI large models into their glasses products.

Overview of Select 2026 AI Glasses Product Launches and Plans

Overview of Select 2026 AI Glasses Product Launches and Plans

Looking at these new products, two core trends emerge in the industry.

First, "lightweight" and "standalone" designs are advancing in tandem. Manufacturers are prioritizing wearer comfort over simply stacking display features, as seen in Rokid's 38.5-gram model and Apple's display-less strategy, while using eSIM and standalone chips to gradually reduce reliance on smartphones.

Second, "AI capabilities" have become the core selling point, evolving from simple voice assistants to AI Agents with multimodal perception, environmental understanding, and proactive services. Deep integration of large models with glasses hardware is now standard.

02 Behind the Explosion: The "Trident" Synergy of Cost, Technology, and Demand

Why are AI glasses experiencing a concentrated outbreak (breakout) in 2026? This is no coincidence but the inevitable result of mature supply chains, technological inflection points, and market demand resonance. A research report by China Merchants Securities points out that behind this "Hundred Glasses War" lie three key drivers: accelerated supply chain cost reductions, AI interaction transforming glasses from "toys" into productivity tools, and scenario adaptation providing killer applications.

First, rapid supply chain cost reductions and localization have provided a commercial foundation for the "Hundred Glasses War."

From a supply chain cost perspective, chips account for over one-third of costs in AI photography and audio glasses, while micro-displays and optical modules make up over half in display-equipped AI glasses.

Over the past two years, accelerated chip localization, breakthroughs in waveguide processes, and maturing Micro LED micro-display technologies have significantly reduced core component costs. Industry data shows that Chinese manufacturers, leveraging their complete supply chain advantages, now hold over 80% of the global AI glasses market share.

In the chip sector, companies like BES Technik and Allwinner Technology have developed AI-specific chips that elevate computing power and power efficiency to industry-leading levels. In optical displays, firms like Crystal-Optech and Lante Optics have cracked the mass production of resin waveguide lenses, reducing the weight of full-color AR glasses from 90 grams to 49 grams, approaching the wearability of ordinary glasses.

Cost reductions have directly translated to terminal pricing—mainstream AI glasses products now fall within the 2,000-3,000 yuan range acceptable to mass consumers, clearing a key hurdle for market expansion.

Second, the deployment of on-device AI and breakthroughs in interaction technologies have resolved product "usability" challenges.

Previously, smart glasses were constrained by the "impossible trinity" of weight, battery life, and computing power. Today, the launch of dedicated chips like Qualcomm's AR1 series enables complex AI algorithms to run at ultra-low power consumption. For example, at CES 2026, Goertek showcased its Rubis AR glasses, which use an MCU+ISP+NPU triple-chip heterogeneous system to streamline processing from cameras, ISPs, and NPUs to displays, allowing lightweight object detection models to run on the NPU at minimal power.

Meanwhile, optical solutions evolving from BirdBath to geometric/diffractive waveguides and display technologies iterating from LCoS to Micro OLED/Micro LED have enabled lightweight products with all-day usability. Features like the eSIM functionality in Thunderbird X3 Pro and multimodal AI recognition in Rokid Glasses are direct manifestations of these breakthroughs.

Notably, Rokid has deepened its collaboration with leading domestic large model companies to develop exclusive on-device multimodal models. Its next-gen AI glasses will be driven by generative AI and AI Agents, creating a new operating system and interaction interface.

Interaction innovations are also evident in multimodal perception breakthroughs—Rokid's automotive AI glasses, developed with GAC Group, allow remote vehicle control via voice commands, including locking/unlocking, climate control, and even automatic parking. Xuanjing Technology's "Hongyan AIOS" system automatically switches service modes based on user scenarios. These advancements signify glasses' evolution from "toys" to "productivity tools."

Third, clear policy incentives and market expectations have injected strong momentum into the industry's outbreak (breakout).

In 2026, smart glasses were included in national consumer subsidy programs for the first time—the National Development and Reform Commission and Ministry of Finance jointly announced policies offering 15% subsidies on sales prices for four categories of digital products, including smart glasses, with a maximum subsidy of 500 yuan per unit. This policy is seen as a signal to establish smart glasses as "strategic mass-market terminals," driving their transition from "niche novelties" to "universal devices."

Policy incentives, coupled with technological maturity, have fueled unprecedented market optimism. IDC predicts that, driven by manufacturers' new product launches and national subsidy policies, China's smart glasses market shipments will reach 4.51 million units in 2026, up 78% year-on-year; global shipments could exceed 23 million units, with AI glasses surpassing 10 million units for the first time.

The enormous market growth expectations have, in turn, attracted more players—Thunderbird Innovation secured over 1 billion yuan in Series C+ funding led by China Mobile's Lead Fund and CITIC Goldstone; ShargeTek raised nearly 100 million yuan; and 17 AI glasses concept stocks saw net purchases exceeding 200 million yuan in a single quarter.

The synergy of policies and capital has created a virtuous cycle of "supply creating demand, demand pulling supply," providing the most compelling explanation for the 2026 concentrated outbreak (breakout).

03 The Future Battle: From "Hardware Involution" to "Ecosystem Definition"

With Meta planning 20 million-unit production capacity, Google rebuilding its OS ecosystem, and Apple testing the waters with lightweight devices, the 2026 competition focus has quietly shifted. The industry is moving from early hardware parameter races to deeper contests over user experience, technological integration, and ecosystem development.

First, user experience now trumps technological showmanship as the core of product competitiveness.

Faced with concerns over high return rates and accusations of "gimmicky" features, manufacturers must find reasons for users to wear their glasses daily. On social media, consumers care less about specs and more about "whether they'll get tired after wearing them for long periods."

Rokid's data supports this: its Rokid Glasses average 8 hours of daily wear, with users truly integrating them into daily life rather than relegating them to "toys."

In 2026, manufacturers are shifting from feature stacking to scenario deep-diving. Rokid partnered with GAC Group to integrate AI glasses into in-car full-scenario interactions, enabling remote vehicle control and navigation projection. Nanobox launched the world's first AI learning glasses, equipped with an education-specific large model that generates real-time class notes and intelligently plans vocabulary reviews, making learning efficiency and focus core values.

IDC China analyst Ye Qingqing believes 2026 is a pivotal year for vertical scenario implementation in smart glasses. Only by deeply integrating AI capabilities into high-frequency, essential fields can products transition from "novelties" to "everyday tools."

Second, technological integration now outperforms single breakthroughs, with system-level innovations determining product excellence.

Previously, smart glasses were constrained by the "impossible trinity" of weight, battery life, and computing power. Today, single-component upgrades are no longer sufficient—true breakthroughs come from system-level synergistic optimization.

Goertek's Rubis AR glasses, showcased at CES 2026, use an MCU+ISP+NPU triple-chip heterogeneous architecture to efficiently coordinate processing from cameras, NPUs, and displays, enabling lightweight object detection models to run at ultra-low power. This "heterogeneous computing" approach allows glasses to evolve from passive response to proactive perception.

Meanwhile, interaction integration is accelerating—Rokid partnered with Wearable Devices to incorporate the neural wristband Mudra Link into AI glasses, enabling precise control through subtle finger movements and making interaction "second nature."

This evolution from "single-point breakthroughs" to "system integration" marks the industry's true maturity.

Finally, ecosystem development determines long-term value, as standalone hardware cannot win the war.

Analysts at Huafu Securities point out that manufacturing glasses hardware has relatively low barriers in China and is highly commoditized. When supply chains converge and product designs become stereotyped, the true barriers lie in software ecosystems and AI capabilities.

Google's Project Aura, developed with XREAL, aims not just to sell glasses but to promote the Android XR system, replicating its "ecosystem platform" strategy from the smartphone era.

Domestic manufacturers are also ramping up ecosystem efforts: Huawei leverages HarmonyOS for seamless collaboration across phones, tablets, vehicles, and glasses. Rokid, active in 115 countries with over 100,000 active users, has integrated ecosystem partners like AutoNavi Maps, Alipay, and JD Technology.

The future competition won't be between glasses alone but between ecosystems—whoever can best integrate large model capabilities, application services, and user data into glasses will dominate the next era of human-machine interaction.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan