"Magic" Smartphones: Apple, Xiaomi, and Huawei's Mid-to-High-End Models Defy Market Trends with Price Cuts, While OPPO, Vivo, and Honor Raise Prices

05/20 2026

05/20 2026

695

695

Price Cuts on Multiple Flagship Models from Huawei, Apple, and Xiaomi Before 618: Which Offers the Best Deals?

Apple, Huawei, and Xiaomi's high-end models collectively see price reductions.

While storage chip prices are soaring on the back of AI demand, brands like OPPO, Vivo, and Honor were forced to collectively raise prices starting in March to protect their margins. However, the top three players suddenly went against the tide in mid-May.

On May 15, Apple's iPhone 17 Pro series saw a ¥1,000 price cut, with some e-commerce platforms offering additional subsidies for trade-ins, bringing the final price below ¥7,000. On the same day, Huawei's Mate X7 dropped by ¥1,000, and the Mate X6 saw a hefty ¥3,000 reduction.

Xiaomi took the lead by reducing the 15 Ultra by ¥1,500 on May 14, with promotions lasting until June 18.

At a time when storage costs are still climbing, leading manufacturers are choosing to cut prices against the trend. With the diminishing marginal effects of innovation in the smartphone industry, how much cushion can brand premium provide for this price war? Is this early-ignited "price war" a short-term inventory clearance or the beginning of a long-term market shift?

I

Platform Subsidies + National Subsidies + Trade-Ins: Which Smartphone Brand Offers the Best Value?

This round of price cuts is essentially an early move to generate pre-618 buzz, with e-commerce store discounts, platform subsidies, some national subsidies, and trade-in policies stacking to make the actual transaction prices far lower than the official website prices.

The New Insight Research Institute checked leading e-commerce platforms like Taobao/Tmall and JD.com and found that high-value subsidy coupons are available at the official flagship stores of Apple, Huawei, and Xiaomi, which have also updated their advertising graphics with "618" themes.

For example, on Taobao and Tmall, Apple's official Tmall flagship store is running a "618 Brings Joy" campaign, offering up to ¥1,000 off the iPhone 17 Pro, ¥2,000 off the iPhone Air plus a ¥500 national subsidy, ¥700 off the Apple Watch Series 11 plus a ¥500 national subsidy, and ¥220 off the AirPods Pro 3. The first three offers can be stacked with interest-free installment plans.

Meanwhile, the official flagship stores of Xiaomi and Huawei have also added 618 tags.

In terms of pricing, the iPhone 17 Pro, originally priced at ¥8,999, can be reduced to ¥7,999 with a ¥700 store discount and a ¥300 platform discount. Further savings can be achieved through trade-ins.

For instance, trading in an old iPhone 14 model in good condition yields a ¥742 recycling value plus a ¥100 trade-in subsidy, bringing the overall price to ¥7,157. The newer the model, the higher the recycling price, and higher recycling prices can lead to greater subsidies.

In other words, the advertised price drops of ¥2,000 may only be achievable by stacking trade-in subsidies, not through direct price cuts alone.

Notably, on the homepage of Apple's official Tmall flagship store, the iPhone 17 Pro or iPhone 17 Pro Max does not carry the national subsidy label, while the iPhone 17 and iPhone Air do.

After the price cut announcement, Apple officially informed the New Insight Research Institute that the price reduction campaign is indeed underway but is not available on Apple's official website. The discounts are only available at Apple's official Tmall flagship store and authorized dealers.

Apple stated that the price cuts are for the 618 campaign, which ends on June 21.

Regarding national subsidies, Apple mentioned that they generally apply to devices priced below ¥6,000.

Not only are Apple's high-end models seeing price reductions, but Huawei's high-end foldable model, the Mate X7, is also eligible for a ¥1,000 coupon, bringing its price down from ¥12,999 to ¥11,999. When combined with a trade-in of an old iPhone 14 model in good condition, the total discount reaches ¥1,022, reducing the overall price to ¥10,977. Under the same trade-in conditions, Huawei's subsidy is ¥180 higher than Apple's.

Besides the Mate X7, Huawei's Mate X6 has seen the steepest price cut, with a ¥1,000 store discount and a ¥2,000 platform discount, reducing its original price of ¥12,999 to ¥9,999. When combined with a trade-in, the price drops to as low as ¥8,977, a "small fracture " (minor price break) in comparison.

Xiaomi, on the other hand, is focusing on older models like the Xiaomi 15 Ultra, which can be reduced to as low as ¥4,799 with platform and store discounts, and below ¥3,700 with trade-ins. Newer models like the Xiaomi 17 Pro and Xiaomi 17 Pro Max only qualify for a ¥500 national subsidy.

In terms of platform price comparisons, under the same conditions, Apple's smartphone series is cheaper on JD.com than on Tmall due to JD.com's additional trade-in subsidies. The price differences for Huawei and Xiaomi models between platforms are not significant.

For consumers, this round of stacked discounts, such as platform billion-dollar subsidies and trade-in subsidies, creates a rare window of opportunity. Given the market's expectation that storage chip prices will continue to rise, manufacturers will face greater cost pressures in the second half of the year, making it highly unlikely that current promotional efforts will be sustained.

II

Mid-to-High-End Models as Apple and Huawei's Moat: Are OV, Xiaomi, and Honor Facing Tough Times?

Starting in the second half of 2025, the global storage chip market entered a strong upward cycle, with AI servers driving massive demand for DRAM and NAND, compounded by localized supply chain tensions that severely squeezed consumer electronics production capacity.

According to Sigmaintell Consulting, NAND flash memory prices for consumer electronics are expected to continue rising in the second quarter of 2026. Prices for NAND in smartphones are projected to increase by 40%-45% quarter-over-quarter, while consumer-grade SSDs are expected to rise by 35%-40%, though the pace of increase has slowed compared to the first quarter, when smartphone NAND prices surged by 65%-70% quarter-over-quarter. Mid-to-low-end models are bearing the brunt of the pressure.

Since March of this year, brands like OPPO, Vivo, and Honor have been adjusting the prices of their new models, with starting prices rising by ¥1,000 or more. This has been seen as the largest collective price hike in the past five years.

Some manufacturers have adopted a "volume reduction for profit protection" strategy, cutting shipments of low-end models and shifting toward higher-margin premium versions to mitigate cost risks. However, Apple and Huawei's choices stand in stark contrast to most other brands.

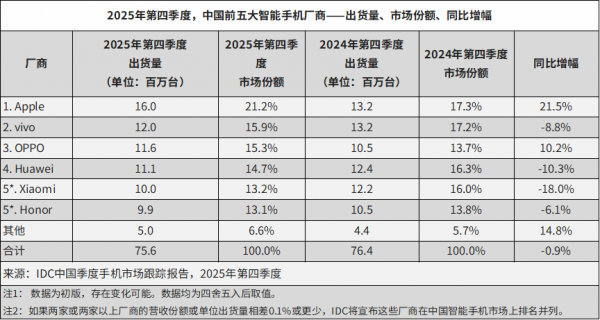

IDC data shows that in Q1 2026, smartphone shipments in China reached approximately 69 million units, down 3.3% year-over-year. Huawei led with a roughly 20% market share, while Apple rose to second place with about 19%. In contrast, cost-effective brands like OPPO, Vivo, Xiaomi, and Honor fared poorly.

OPPO's shipments in Q1 2026 fell 8.5% year-over-year, Honor's dropped by 2%, Vivo's increased slightly by 1.1%, and Xiaomi fell out of the top five, having ranked fourth in the previous quarter.

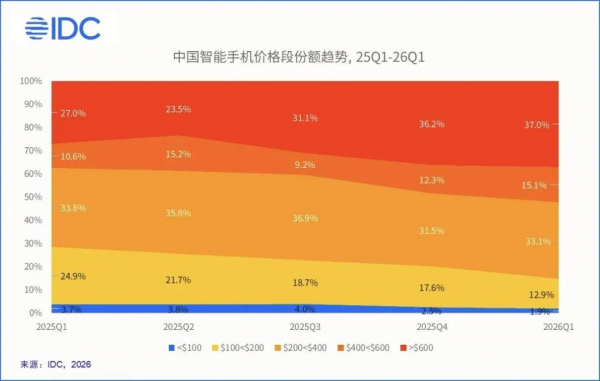

Despite the overall market downturn, the share of high-end models (priced above $600) continues to grow. In Q1 2025, the $200-$400 price segment performed the strongest, capturing 33.8% of the market, followed by the $100-$200 mid-range segment at 24.9%, becoming the mainstream consumer choices. High-end models above $600 accounted for just 27% of the market.

However, in Q1 2026, the market consumption structure shifted significantly. The share of $200-$400 models dropped to 33.1%, while the $100-$200 segment plummeted to 12.9%. In contrast, high-end smartphones above $600 surged to 37% of the market, showing remarkable growth.

Apple's confidence in price cuts stems from its iOS ecosystem's high user stickiness, industry-leading second-hand resale value, and strong bargaining power in the global supply chain.

Even with the iPhone 17 Pro series voluntarily entering the $600-$800 price range, its average selling price (ASP) remains high, generating significant revenue and profit from relatively restrained shipment volumes.

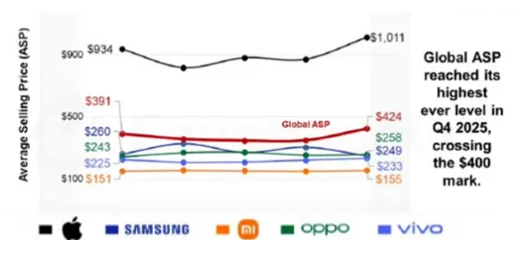

Counterpoint Research data shows that Apple's iPhone ASP surpassed $1,000 for the first time in Q4 2025, driven by strong sales of the iPhone 17 series' Pro and Pro Max versions, which pulled up the average price.

This has significantly widened the ASP gap with Android manufacturers, a clear manifestation of brand premium. Consumers are willing to pay extra for the ecosystem, stability, and residual value.

Huawei, meanwhile, has reduced its sensitivity to external storage price hikes by improving the self-sufficiency rate of its Kirin chips and optimizing its domestic supply chain. The steep price cuts on the Mate X6/X7 are not only a result of cost space release but also a deliberate effort to accelerate the mainstream adoption of foldable screens while firmly maintaining its brand image of technological innovation and high-end positioning.

Under high storage cost pressure, Huawei demonstrates stronger pricing flexibility than most Android manufacturers. In contrast, brands like OPPO, Vivo, Xiaomi, and Honor, which emphasize cost-effectiveness, face a more delicate situation. Reducing the 15 Ultra to the ¥4,300 range is a standard "price-for-volume" tactic aimed at capturing mid-to-high-end users and stabilizing market share before 618.

However, with core component costs like storage remaining high, this strategy risks further compressing already tight profit margins, potentially leading to a situation where shipments increase but profits do not. The differences in price premium coefficients are starkly revealed here.

Apple and Huawei's premium space stems from their long-accumulated brand strength, ecosystem barriers, technology, and supply chain autonomy, while other brands rely more on hardware configurations and immediate price levers.

When external cost shocks hit, the former have more room to maneuver, while the latter are easily pushed into a corner.

Samsung's experience in the Chinese market serves as a cautionary tale. Its once-high premium positioning gradually collapsed amid fierce competition and pressure from local brands, leading to sustained market share declines and forcing it to drastically adjust its strategy.

This serves as a reminder to current manufacturers that once premium positioning crumbles, rebuilding it is difficult. This round of price cuts is accelerating this differentiation process and testing the true depth of different brands' moats.

Consider this: storage chip prices are still rising, yet Apple and Huawei can still afford to cut prices on their high-end smartphones. Doesn't this demonstrate that cost is merely the backdrop, while brand premium power and the competition for existing users are the real core variables?

III

Have the "Wait-and-See" Crowd Really "Won"?

The most direct beneficiaries of this round of price cuts are consumers, and their behavioral changes are the most intriguing.

The shift from "wait-and-see" to "buy now" can happen in just a few hours, as many users are spurred into quick decisions by the lure of stacked subsidies.

These "discounts" transform hesitant upgrade plans into immediate actions. Subsidies are no longer simple discounts but precisely target the "get-a-bargain" switch in consumers' psychological accounts, turning large expenditures into a sense of smart consumption satisfaction.

However, the frenzy of price cuts also sows seeds of future problems. Frequent, substantial, and highly stacked promotions may foster more extreme wait-and-see habits in the long run.

Users might strategically wait for the maximum subsidy before making a purchase, posing a potential challenge to manufacturers' natural sales rhythms.

Moreover, while steep price cuts can quickly expand the user base, they may also leave early adopters feeling "ripped off" for buying too soon.

A netizen from Shanxi posted on social media: "The sky is falling. I just bought the 17 Pro at an offline store on May 7 for ¥8,999. I'm so upset I could cry." Others lamented the lack of price protection for early purchases.

Changes in consumer behavior will profoundly influence industry trends. With price sensitivity fully awakened, manufacturers will have to contend with a more discerning and pragmatic user base.

Relying solely on hardware specifications and periodic discounts will increasingly fail to impress them. The real competition will shift toward continuous optimization of user experience, deep binding of ecosystem services, and long-term value delivery.

In the mature market, consumers have won lower prices, but could the industry lose its momentum for further growth? After 618, will there be a brief lull following the promotional frenzy, or will it spark an even fiercer round of competition?

The answer may lie not with manufacturers but in the choices of increasingly mature and discerning consumers.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle