Car Companies Unite in 'Humanoid Creation': The Embodied AI Revolution Transforming the Automotive Industry

05/19 2026

05/19 2026

514

514

As the automotive industry, with its century-long legacy, embraces the wave of embodied AI, global car manufacturers are strategically pivoting from 'crafting wheels' to 'designing humanoids.' The embodied AI robotics sector is now harnessing the might of the most formidable industrial forces.

Leading automotive firms are capitalizing on their triple strengths—technology reuse, manufacturing synergy, and closed-loop scenarios—to overcome the three major hurdles of the embodied AI industry: 'implementation challenges, mass production difficulties, and commercialization barriers.' They are propelling humanoid robots from lab curiosities to essential deployments on a scale of tens of thousands, reshaping the global landscape of intelligent manufacturing and embodied AI.

Car Companies Unite: Diverse Strategies and Emerging Obstacles

The year 2026 marks a pivotal turning point for the embodied AI robotics industry, as global mainstream automotive companies collectively venture into this realm. From technology R&D and production line trials to large-scale mass production, they are becoming the driving force propelling the industry out of laboratories and into industrialization.

As of April 2026, from North America to Europe and China, nearly 20 major automotive companies, including Tesla, Mercedes-Benz, BMW, Volkswagen, Changan, SAIC, XPeng, GAC, and Chery, have entered the embodied AI sector through self-development, joint ventures, and incubations. This has created a dynamic tripartite situation where 'tech-driven automotive companies lead, traditional giants follow, and Chinese automotive firms break new ground.'

This crossover is not a fleeting trend but an inevitable evolution for the industry, profoundly reshaping the future of intelligent manufacturing and artificial intelligence.

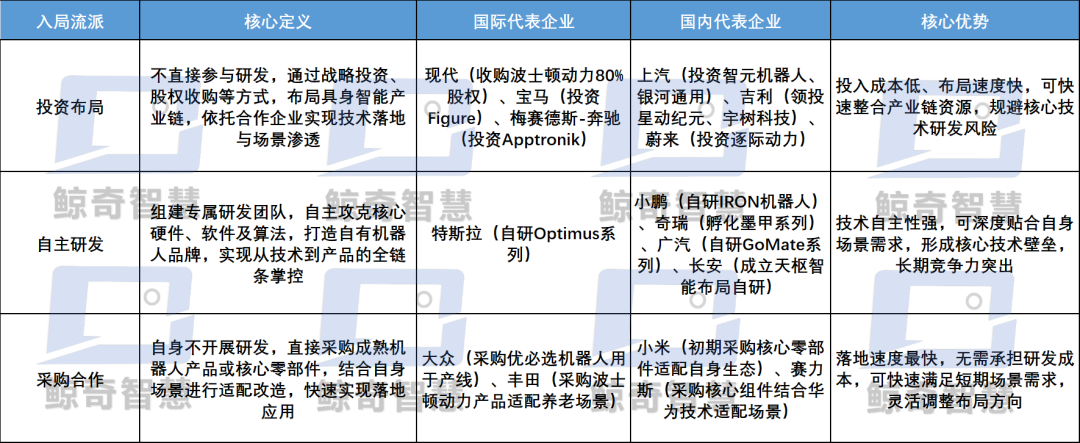

Notably, the entry strategies of domestic and foreign automotive companies can be categorized into three distinct schools of thought: investment and strategic positioning, independent R&D, and procurement collaboration. Each school leverages its unique strengths to form a differentiated competitive landscape, as illustrated below:

The parallel progress of these three schools is rapidly heating up the embodied AI robotics sector. However, beneath the industry's surface prosperity, four major pain points are becoming increasingly prominent, acting as key bottlenecks that hinder industrialization and making entry for automotive companies a necessity rather than an option:

Hardware Limitations: Core components (such as reducers, servo motors, and dexterous hands) account for over 70% of costs. Early reliance on imports and low localization rates keep overall machine prices high.

Scalability Issues: Robot companies primarily engage in small-batch trials, with low yield rates and slow capacity expansions, making it difficult to achieve economies of scale.

Scenario Constraints: Robots lack strong generalization abilities and sufficient data accumulation (only meeting 1/10 of requirements), making them unable to adapt to complex industrial scenarios and keeping them in the 'trial' phase for extended periods.

Revenue Challenges: Most companies are still in the 'burning cash for R&D' phase, with unclear profit models. Small and medium-sized tech companies struggle to sustain R&D investments, urgently needing entities with financial, technological, and scenario advantages to break the deadlock.

These challenges cannot be overcome by a single company. Automotive companies, with their financial clout, 'automotive-grade' supply chain advantages, technological accumulation, and application scenario strengths, have become the core force in breaking through these bottlenecks in embodied AI.

The entry of automotive companies into the embodied AI robotics sector is both an inevitable choice for their own development and a responsibility to drive industrial industrialization.

Automotive Companies Embrace Robotics: A Strategic Move Driven by Capital, Technology, and Market

The crossover of automotive companies into robotics is not a random occurrence but a strategic necessity rooted in industrial cycles, technological DNA, and market potential.

The current automotive industry is facing intense 'involution,' with frequent price wars leading to declining profit margins, shrinking traditional fuel vehicle markets, and fierce competition in the new energy vehicle sector. Automotive companies urgently need new growth avenues and a second growth curve.

As the next core sector of future industries, embodied AI is predicted by authoritative institutions to reach a global humanoid robot market size of $10 trillion by 2030, far surpassing the current automotive industry space. This presents a key opportunity for automotive companies to break through growth bottlenecks.

From a capital market perspective, positioning in embodied AI has become crucial for automotive companies to enhance their valuations. Tesla's Optimus project directly boosted the company's valuation by over $200 billion; Chery, XPeng, and other companies have achieved significant valuation premiums through their robot ventures, opening new financing channels.

More importantly, embodied AI R&D requires massive investments, which small and medium-sized tech companies struggle to sustain. Automotive companies, with their years of accumulated financial strength, can continuously invest in R&D, breaking through barriers of technology, capital, and scenarios, and driving the sector from 'concept hype' to 'large-scale implementation,' resolving the dilemma of 'unsustainable R&D spending.'

Additionally, intelligent vehicles and robots share a common technological foundation, with technology reuse lowering R&D thresholds. Intelligent vehicles and embodied AI robots are essentially both 'embodied intelligent agents,' with over 70% overlap in underlying technologies. This technological homology gives automotive companies a natural crossover advantage, significantly lowering robot R&D thresholds and resolving the dilemmas of 'technological homogenization and insufficient generalization.'

At the hardware level, automotive motors, batteries, sensors, controllers, and chips can be fully shared. Automotive 'three-electric' technologies can be directly transferred to robot power systems—XPeng's IRON robot uses chips derived from autonomous driving technology, GAC's wheeled-foot structure reuses automotive suspension designs, and Changan extends automotive safety standards to robots.

At the software level, autonomous driving FSD algorithms, multimodal perception, path planning, and decision-making systems can be directly transferred to robot environmental understanding and motion control. Tesla's Optimus core algorithms fully reuse the FSD architecture, reducing end-to-end latency to 19ms.

At the manufacturing level, automotive companies possess the world's most mature precision manufacturing, supply chain management, and quality control systems, capable of increasing robot mass production yield rates from 60% to 90% and reducing core hardware costs by 40%, resolving the pain points of 'difficult mass production and high costs.'

Meanwhile, the rigid demand in automotive companies' manufacturing scenarios serves as an important 'testing ground' for robot deployment. Deploying robots on their production lines achieves 'research through usage,' with internal demand continuously generating vast amounts of real data, forming a positive cycle of 'technology R&D—production line verification—data feedback—technology upgrading.'

The vast blue ocean space in external markets also provides automotive companies with immense development potential. Extending from automotive production lines to 3C electronics, logistics, new energy, commercial services, elderly care, and other scenarios, automotive companies can leverage their scenario-based experience to rapidly replicate robot products to other industries, establishing a 'R&D—pilot—large-scale' commercialization path.

In essence, the crossover of automotive companies is a strategic move that leverages their strengths to create a 'automobile + robot' bidirectional empowerment industrial ecosystem.

Automotive Companies Reshape Industries and Drive 'Essential Deployments'

The year 2026 marks the first year of large-scale embodied AI implementation, with Zhiyuan Robotics rolling off its 10,000th general-purpose embodied robot, signaling the industry's definitive departure from the 'prototype era' into the 'product era.'

The collective entry of automotive companies into the humanoid robot sector is not merely a 'crossover product creation' but a strategic extension of the automotive industry's century-long evolution and a core force driving the industrialization of embodied AI and reshaping the global intelligent manufacturing landscape. Its deeper significance far exceeds the products themselves, propelling robots from 'trial usage' to 'essential deployments.'

Building robots is essentially a strategic transformation for automotive companies from 'vehicle manufacturers' to 'embodied AI solution providers,' completely breaking the boundaries of the automotive industry and constructing a 'automobile + robot' dual-drive industrial ecosystem.

This transformation not only enables automotive companies to diversify beyond reliance on single automotive products but also promotes deep integration between the automotive industry and artificial intelligence, intelligent manufacturing, and high-end equipment manufacturing, forming new industrial clusters.

More importantly, automotive companies are reshaping the rules of the robotics industry with their industrial logic—introducing automotive mass production standards, quality control systems, and supply chain management capabilities into the robotics industry, driving robots from 'laboratory prototypes' to 'industrialized products.' Humanoid robots are no longer conceptual exhibits but become essential equipment for manufacturing.

The entry of automotive companies through the three major schools of thought, integrating industrial chain resources and promoting collaborative development, is expected to resolve industrial 'chokepoint' issues through localized substitution of core components, enhancing China's global voice in the embodied AI field. A trillion-dollar embodied AI industrial ecosystem is accelerating its formation.

In the next three years, whoever can first achieve the transition of robots from 'pilot trials' to 'essential deployments' will secure the commanding heights in the new round of intelligent industrial revolution.

Whale ODD Comments

The collective entry of automotive companies into humanoid robotics is an inevitable choice for the century-long evolution of the automotive industry and a core turning point for the industrialization of embodied AI. From the differentiated positioning of the three major entry schools to the natural advantages in resolving the industry's four major pain points, and to the deeper significance of reshaping industries, iterating technologies, and serving industries, automotive companies are leveraging their heritage to drive embodied AI from 'concept' to 'reality.'

When automotive 'wheels' meet robotic 'legs,' the triple synergy of technological homology, capital collaboration, and market complementarity is breaking industrial boundaries. The next golden decade of the automotive industry will be redefined by embodied AI.

*Editor's Note: Original content creation is no easy feat; please respect the author's efforts. For reprints, please contact us for permission.

-

![]()

Why Did Tesla’s Profits Drop and Cash Flow Go Negative?

-

![]()

AI Titans Are All in the Red: Time for Intelligent Driving Car Buyers to Reassess?

-

![]()

In the Next Decade of Joint Ventures, Honda Should Move Away from 'Stubbornness'

-

![]()

Operating Profit Plummets by 57%! What Caused Tesla’s Profitability to Decline in Q2?

-

![]()

Starting at 12,999 Yuan! Samsung’s Pioneering Wide Foldable Phone Unveiled: Sleek, Lightweight, and Ushering in a New Era for Android Foldables

-

![]()

Seven Bankruptcies Fail to Topple It! Aston Martin Raises £550 Million to Keep Afloat

-

![]()

Weichai's 'Triple Leap': From Diesel Engine Manufacturer to a 400 Billion Yuan Powerhouse

-

![]()

Tesla’s Financial Acumen Outshines Even Huawei’s