2.27 Billion Shares Unlocked: Will Insta360 Face a Mass Sell-Off?

06/11 2026

06/11 2026

395

395

On June 11, 2025, Insta360 Innovations made its stock market debut, with its share price rocketing up by 274.44% on the very first day of trading.

Confronted with this sudden surge in enthusiasm, 33-year-old Liu Jingkang remarked, “This was something we hadn't anticipated.” “However, it's evident that the price-to-earnings (P/E) ratios of typical tech firms don't come close to ours.” He further explained that pricing dynamics differ between the secondary and primary markets, with the public and investors adopting vastly different valuation models and perspectives.

This statement acted as a preemptive measure to manage expectations.

A year down the line, Insta360's share price has experienced a wild ride, surging from over RMB 70 billion on its debut to a peak of RMB 140 billion (based on closing prices), only to now fall below the RMB 70 billion mark.

Tomorrow, Insta360 Innovations will celebrate its first anniversary as a publicly traded company, coinciding with the unlocking of a staggering 227 million restricted shares. This represents 56.5% of the total share capital, expanding the free float from 32.8 million shares to 259 million shares—nearly a sevenfold increase.

While the exact timing of when these 227 million shares will enter the market remains uncertain, the potential for a significant influx is undeniable.

Consequently, Insta360 Innovations must now undergo a rigorous valuation stress test, questioning whether its lofty valuation—higher than that of typical tech companies—can be sustained.

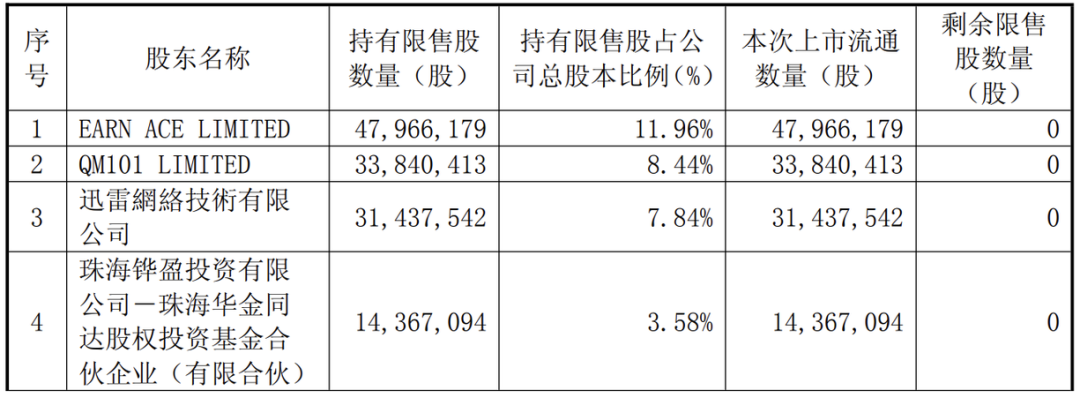

In terms of scale, this unlocking involves approximately 227 million restricted shares, accounting for 56.50% of the total share capital. Based on the closing price of RMB 163.45 on June 10, this equates to a market value of around RMB 37 billion.

The unlocked shares comprise original shareholder restricted shares and strategic placement shares from the IPO, with the majority being restricted shares from pre-IPO original shareholders, totaling around 220 million shares.

Structurally, the unlocking shareholders are predominantly financial investors, with no holdings by the founding team. The top three institutions collectively account for over 28% of the unlocking, including EARN ACE LIMITED from the IDG Group, QM101 LIMITED from Qiming Venture Partners, and Xunlei Network.

These institutions' investments date back to 2015, with extremely low average costs. Among them, IDG's investment stands out as particularly representative.

As early as 2013, Tong Chen, an IDG Capital analyst and now a director at Insta360 Innovations, met Liu Jingkang. By 2014, when Liu had “no revenue, no team, and no product,” IDG had already expressed its intention to invest.

During the Series A financing in 2015, IDG acquired 333,333 shares for USD 652,500. Later that year, in the Series B financing, IDG purchased an additional 84,388 shares for USD 1 million, bringing its total investment to USD 1.6525 million.

Following subsequent equity changes, including VIE structure dismantling, capital increases, share reforms, and the IPO, EARN ACE LIMITED from the IDG Group now holds 47.966 million shares in Insta360 Innovations. At a share price of RMB 163.45, this represents a market value of RMB 7.84 billion, approximately USD 1.156 billion, yielding a paper gain of around 700 times, excluding dividends.

Qiming Venture Partners entered the fray later, participating in the Series B and Series C financings, acquiring 368,100 shares for USD 5.25 million across two rounds. In 2019, they transferred shares worth RMB 37.4796 million, nearly recovering their initial investment. The current market value of their remaining 33.84 million shares is approximately RMB 5.5 billion, all representing profits.

Of course, unlocking does not necessarily equate to immediate selling.

According to the STAR Market's share reduction rules, shareholders holding more than 5% of the shares cannot reduce their holdings by more than 1% of the total share capital via centralized bidding within any 90 consecutive calendar days, or by more than 2% via block trades. These rules effectively spread out selling over several months or even longer.

However, these rules only serve to slow down the pace of supply release. These shareholders, with extremely low holding costs and paper gains of tens to hundreds of times, and an investment horizon exceeding a decade, have a strong incentive to “cash in.”

Compared to early investors, strategic placement shareholders have seen much smaller gains.

Temasek (accounting for 0.44% of total share capital) and Luxshare Precision (0.12%) invested at the IPO price of RMB 47.27 per share, yielding a paper gain of over two times, excluding dividends.

Among the placement recipients in this unlocking, 202 core employees hold a combined 2.898 million shares through two employee asset management plans, representing 0.72% of the total share capital, with an average holding value of approximately RMB 2.3 million per person.

For the secondary market, the potential RMB 37 billion in selling pressure looms large over the free float. Regardless of when and at what pace shareholders choose to cash in, the mere possibility of massive supply releases prompts buyers to demand higher risk premiums.

Even without immediate selling, the sudden increase in the free float after unlocking shifts the distribution of shares from “concentrated” to “dispersed,” returning pricing power to a more fundamental-driven market.

The essence of the P/E ratio is the market's advance pricing of a company's future profitability.

On June 9, data from East Money showed that the trailing P/E ratio for the consumer electronics sector was 54 times, with the consumer electronics industry (Shenwan) at 41 times, and Insta360 Innovations at 76 times.

The market's pricing of Insta360 Innovations implies expectations of sustained high growth, with profits keeping pace with revenue.

(Source: East Money)

Let's examine revenue first. In 2025, full-year revenue reached RMB 9.741 billion, up 74.76% year-on-year; in the first quarter of 2026, revenue was RMB 2.481 billion, up 83.11% year-on-year. Revenue growth has indeed been outstanding.

Now, let's look at profit. Net profit attributable to the parent company was RMB 929 million in 2025, down 6.62% year-on-year. In the first quarter of 2026, net profit was only RMB 84.62 million, down 52.02% year-on-year. This marks the third consecutive quarter of year-on-year profit declines.

Changes in gross margin provide partial explanations. The overall gross margin was 45.74% in 2025, down 6.46 percentage points from the previous year. In the first quarter of 2026, the gross margin fell 7.73 percentage points year-on-year.

Multiple factors are at play here.

The first factor is the price war triggered by DJI's entry. In July 2025, DJI launched the Osmo 360 panoramic camera, priced lower than Insta360's comparable products. Insta360 quickly responded with price cuts, directly impacting its gross margin.

Over a longer period, Insta360's gross margin has been declining. In 2023, it was 56%; in the first half of 2025, it was 51.22%.

The second factor is the rising cost of upstream memory chips.

Global memory chips are experiencing significant price increases. According to a UBS report in February 2026, the DRAM type primarily used by Insta360 has seen sharp spot price increases since the fourth quarter of 2025 due to supply constraints. After a 30% increase in contract prices in 2025, prices are expected to rise another approximately 100% year-on-year in 2026.

UBS estimates that due to price increases in SoC, DSP, and DRAM chips, Insta360's bill of materials (BOM) costs will rise 9% year-on-year, dragging down the gross margin by about 4 percentage points. This means that, even without considering price wars and strategic investments, rising memory chip costs alone will significantly erode profit margins.

Recently, GoPro, the pioneer of action cameras, issued a bankruptcy risk warning. GoPro's decline resulted from multiple factors, including innovation, product positioning, and competition. However, the final straw was the soaring cost of storage, with prices of its core storage components surging by 80% to 115% year-on-year.

Beyond gross margin, Insta360 attributes its situation to strategic investments, stating that it is making unprecedented strategic investments to trade short-term profits for long-term technological barriers.

Data supports this claim. In 2025, R&D expenses surged by 96.95% year-on-year, nearly doubling. In the first quarter of 2026, R&D investment growth further accelerated to 100%. The company is simultaneously advancing new product categories such as drones, gimbal cameras, and wireless microphones, and has custom-developed three proprietary chips, with related investments reaching RMB 762 million in 2025.

Whether the logic of “trading short-term profits for long-term technological barriers” holds depends on whether these investments can translate into future revenue and profits, and further observation of the contribution of new businesses to revenue.

Looking ahead, DJI's competitive pressure is unlikely to subside in the short term, and the trend of rising memory chip costs driven by AI computing power demands is also unlikely to reverse quickly. If Insta360 cannot pass on cost pressures through price increases, its gross margin will face further pressure.

New product categories and rising storage costs have significantly strained cash flow.

Due to increased purchases of storage components, materials for innovative product categories, and overseas production lines, Insta360 Innovations' operating cash flow turned negative in the first quarter of 2026, with a net outflow of RMB 1.471 billion. Meanwhile, inventory levels at the end of the quarter increased by approximately RMB 880 million from the end of 2025.

Rising inventory is a neutral signal in itself. If new products sell well, increased inventory is a proactive measure; if sales fall short of expectations, strategic inventory will become excess stock.

This means that Insta360 is betting heavily on the market performance of its new products. The success or failure of these products will determine how the market redefines the company: as a platform company breaking out, or as a hardware manufacturer confined to a niche category.

After going public, Insta360's market value once exceeded RMB 140 billion, with a PE (TTM) ratio reaching 140 times. Besides its small free float, this was also due to a widely accepted narrative: its monopoly in the panoramic camera sector and the resulting vision of a platform company.

Monopoly implies pricing power, while a platform implies a much higher ceiling than a single hardware product.

Are these two pillars still stable?

History repeatedly shows a common script: a champion in a niche hardware sector wins a high valuation before going public with a breakthrough single product, but after going public, faces issues such as a market ceiling within reach, giant competitors squeezing profits, and a gap between new product development and market needs.

GoPro's fall from grace in the action camera sector, and the prolonged valuation corrections of Roborock and XGIMI after industry growth slowed, are similar cases.

Insta360 is also part of this story.

Panoramic cameras are a market defined by Insta360. The company has ranked first in global shipments for six consecutive years, with a market share once exceeding 60%.

Once such a niche category fails to become a mass-market product, dominant companies are more likely to hit a ceiling, as seen with XGIMI. When it comes to projectors, XGIMI remains a competitively advantageous brand, and projectors have partially replaced televisions. However, they have never become as ubiquitous as washing machines or air conditioners.

Insta360 has done its utmost to lower usage barriers, turning image creation into a tool “for everyone.” For example, the Insta360 Nano can be used independently or directly plugged into an iPhone, reducing panoramic video processing time from hours to minutes; AI-powered one-click video editing; and the Antigravity A1 panoramic drone eliminates the need for complex post-production editing or high-skill FPV flying techniques.

By lowering usage barriers and optimizing product experiences, Insta360 has captured innovators and early adopters who, like the company, are enthusiastic about exploring new technologies. They have been the primary drivers of growth in recent years.

However, for the broader mass market, “ease of use” is only a necessary condition, not a sufficient one.

A larger variable comes from DJI. DJI is no ordinary product company; it boasts top-tier supply chain integration capabilities, a global distribution network, and imaging technology and brand recognition accumulated in the drone sector.

Its entry has transformed Insta360 from a sector definer into one of two dominant players in a duopoly. This change in the competitive landscape brings not occasional fluctuations but sustained price wars, supply chain battles, and more.

Meanwhile, Insta360 is attempting to build a richer product matrix, including drones and microphones mentioned earlier. This is almost a standard move for “single-category breakthrough” companies after going public: using capital raised from the markets to fuel a second growth curve.

The “Antigravity A1,” co-incubated by Insta360 Innovations and a third party, carries a mission that transcends the product itself, relating to the company's fate. However, its sales performance has not lived up to such high expectations, and its price was reduced after DJI launched its first panoramic drone, the Avata 360.

If new product breakthroughs can unlock a second growth curve and proprietary chip development establishes genuine technological barriers, transforming the company from a panoramic camera company into an intelligent imaging platform, then today's strategic investments will become tomorrow's moat, justifying its above-industry valuation.

If new products fail to gain traction, competition and costs continue to compress profit margins, and cash flow is rapidly depleted in a two-front war, then Insta360 will inevitably regress from a sector leader to an ordinary hardware company, with its high valuation dissipating alongside its scarcity and imagination space.

These questions have persistently haunted Insta360, and as progress is made in unlocking [potential/solutions, depending on context], the urgency to address and resolve them becomes even more pronounced.

With pricing power now distributed among a wider range of investors, the company's valuation may no longer be solely dependent on a single standout product, a compelling narrative, or a fleeting market position. Instead, its true worth will increasingly hinge on its capacity to consistently demonstrate resilience and innovation in the face of fierce competition.

-

![]()

Why Do All Cars Look Alike These Days?

-

Don't Just Focus on Financing Amounts—Look at the 'Order Truth' Behind the Commercialization of Embodied AI

-

![]()

Are Traditional Fuel Cars Really Losing Their Market?

-

![]()

Comprehensive PPT Guide to Understanding CAAM Production and Sales Data: Auto Production and Sales Declines Narrow Again in May; New Energy Vehicle Market Share and Auto Exports Reach New Monthly High

-

![]()

Chinese Cars Seize Overseas Markets: The Advent of a Winner-Takes-All Era

-

![]()

Will WeChat Start Charging Fees?

-

![]()

Cross-border 'Golden Window' in 2026: Chinese Products Sweep Across Southeast Asia

-

![]()

BIWIN Storage, Betting 20 Billion on the Future with Hundreds of Billions in Market Cap